Ouster (OUST) is back in focus after the company announced a collaboration with FUJIFILM to build native color lidar sensors, combining high resolution 3D depth and color data in a single hardware platform.

See our latest analysis for Ouster.

The FUJIFILM partnership lands at a time when the stock has a 1 day share price return of 3.87% and a 90 day share price return of 61.79%, while the 1 year total shareholder return is very large, signaling strong momentum despite a 7 day share price pullback of 9.66%.

If this color lidar story has your attention, it may be worth seeing what else is moving in related areas by scanning 34 robotics and automation stocks

With Ouster trading at US$30.87 and sitting at roughly a 30% discount to the current analyst price target and about a 34% discount to one intrinsic value estimate, you have to ask: is there still a buying opportunity here, or is the recent enthusiasm already pricing in future growth?

Most Popular Narrative: 22.2% Undervalued

On the most followed narrative, Ouster's fair value of $39.67 sits well above the last close at $30.87, putting the focus squarely on what has to go right to close that gap.

Ouster's focus on software-attached bookings, which increased by over 60% in 2024, indicates future growth in high-margin software solutions, likely resulting in improved net margins compared to hardware-only sales.

Want to see what kind of revenue ramp, margin lift, and future earnings profile need to line up to support that price gap? The narrative leans on ambitious growth, a sharp profitability shift, and a premium earnings multiple more often associated with mature leaders than an unprofitable lidar stock.

Result: Fair Value of $39.67 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, there are clear pressure points to watch, including intense competition from Chinese lidar suppliers and potential earnings volatility from shifting product mix and ongoing litigation costs.

Find out about the key risks to this Ouster narrative.

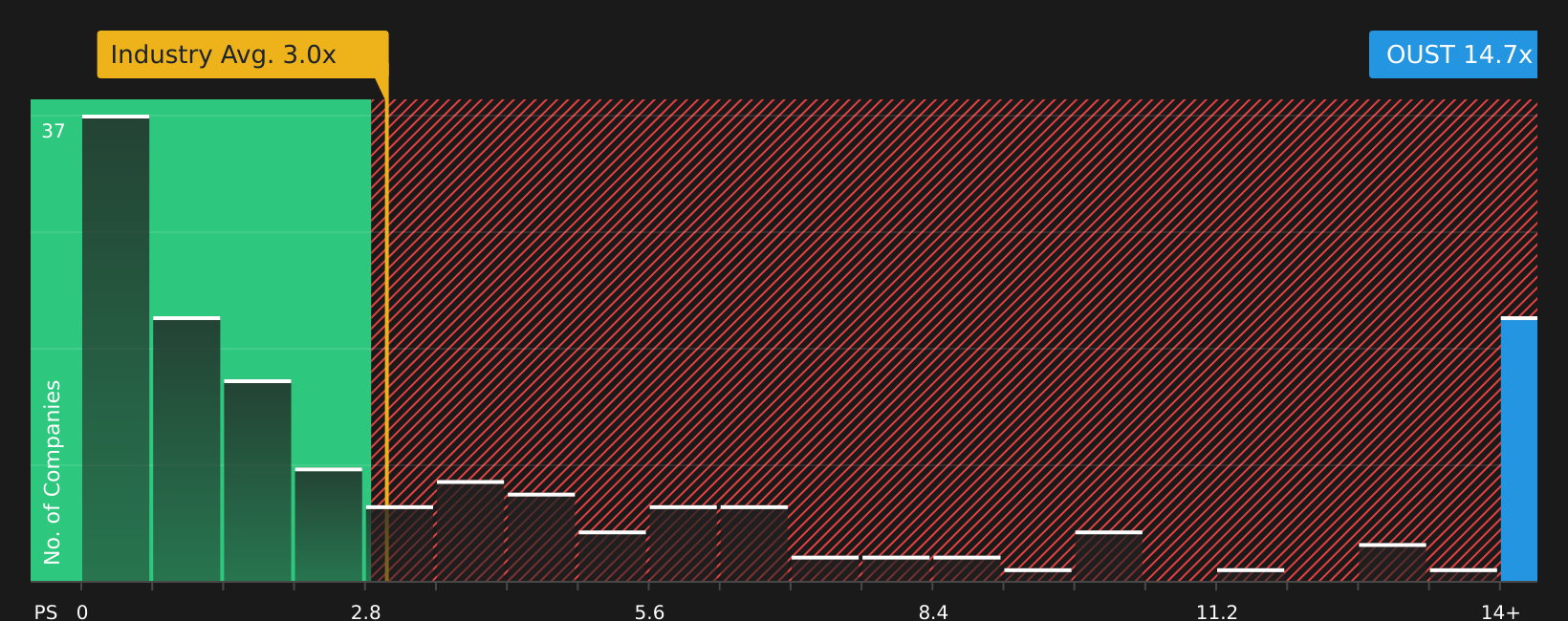

Another View: Price To Sales Paints A Tougher Picture

While the SWS DCF model and analyst targets suggest upside, the current P/S of 10.6x is far above the US Electronic industry at 2.6x, the peer average at 3.4x, and even the fair ratio of 7.4x. This raises the question of how much execution risk is already baked into the price.

See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

Mixed messages in the data so far? Take a closer look at the full picture, consider the trade off between potential upside and clear watchpoints, and review the 4 key rewards and 2 important warning signs

Looking for more investment ideas?

If Ouster is on your radar, do not stop here. Broaden your watchlist with a few targeted ideas that could sharpen your overall investing edge.

- Kickstart a hunt for potential bargains by checking stocks screened as high quality and potentially mispriced through the 51 high quality undervalued stocks.

- Strengthen the defensive side of your portfolio by reviewing companies highlighted in the 67 resilient stocks with low risk scores.

- Spot lesser known opportunities with solid fundamentals before others catch on by scanning the screener containing 21 high quality undiscovered gems.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com