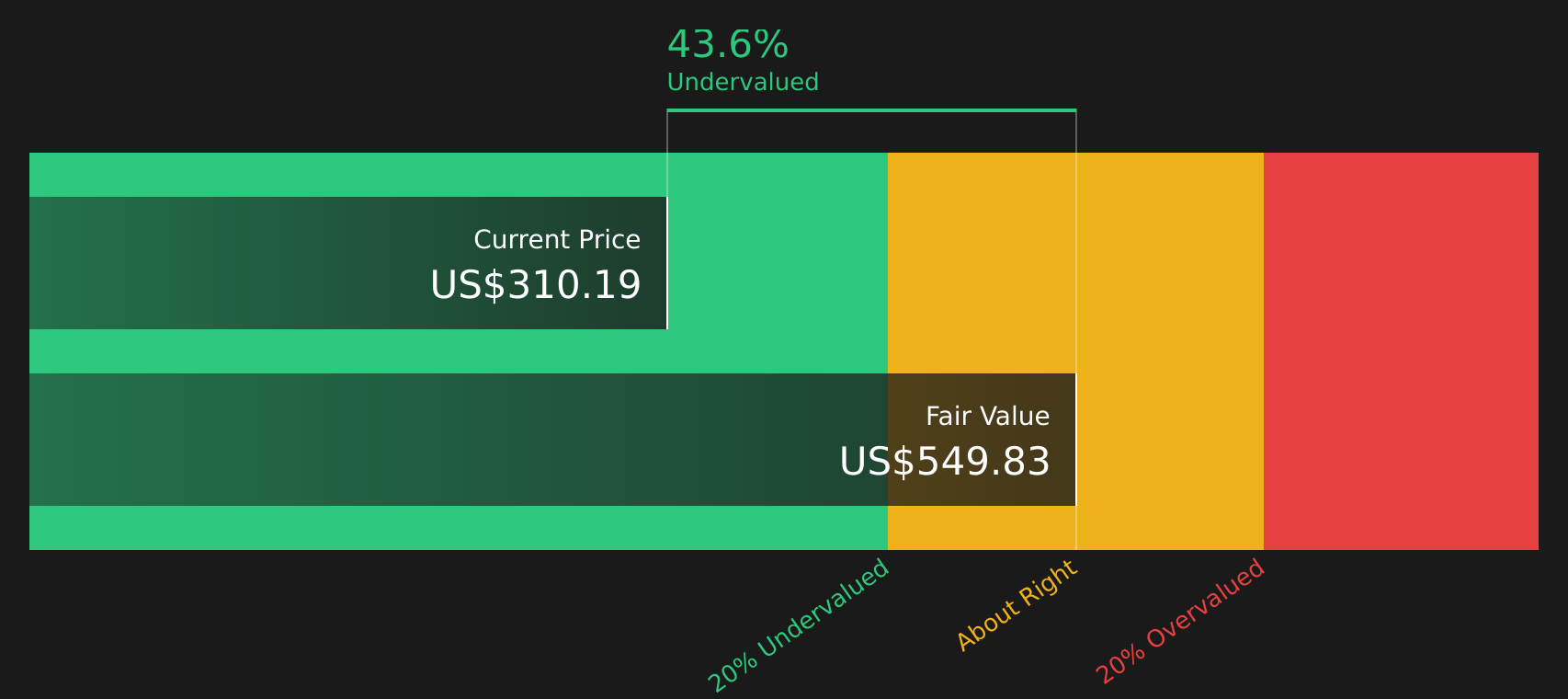

- If you are wondering whether Kinsale Capital Group at around US$310 per share still lines up with its underlying worth, the starting point is to look closely at what the current price implies.

- The stock has fallen 0.4% over the past week, 11.2% over the past month, 21.0% year to date and 33.0% over the last year. Over three and five years it has returned 1.5% and 87.9% respectively.

- Recent headlines around Kinsale Capital Group have focused on its role within the specialty insurance space and ongoing market debate about risk in financials. This helps frame these share price moves. For investors, this context matters because it shapes sentiment around the stock and how much of that risk debate might already be reflected in the price.

- Right now Kinsale Capital Group has a valuation score of 2 out of 6. The next sections will walk through what different valuation methods suggest about the stock, before finishing with a framework that can help you read beyond any single metric.

Kinsale Capital Group scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Kinsale Capital Group Excess Returns Analysis

The Excess Returns model looks at how much profit Kinsale Capital Group generates over and above the return that shareholders are assumed to require, then capitalises those “excess” profits into an intrinsic value per share.

For Kinsale Capital Group, the model uses a Book Value of US$85.31 per share and a Stable EPS of US$23.36 per share, based on weighted future Return on Equity estimates from 9 analysts. The Average Return on Equity used in the model is 22.09%, while the Cost of Equity is US$7.52 per share. That gap between what the equity is expected to earn and what it is expected to cost produces an Excess Return of US$15.85 per share.

The model also assumes a Stable Book Value of US$105.73 per share, again sourced from weighted future Book Value estimates from 9 analysts. Combining these inputs, the Excess Returns approach arrives at an intrinsic value of about US$549.83 per share. Compared with the current share price of around US$310, this suggests the stock is 43.6% undervalued on this view.

Result: UNDERVALUED

Our Excess Returns analysis suggests Kinsale Capital Group is undervalued by 43.6%. Track this in your watchlist or portfolio, or discover 49 more high quality undervalued stocks.

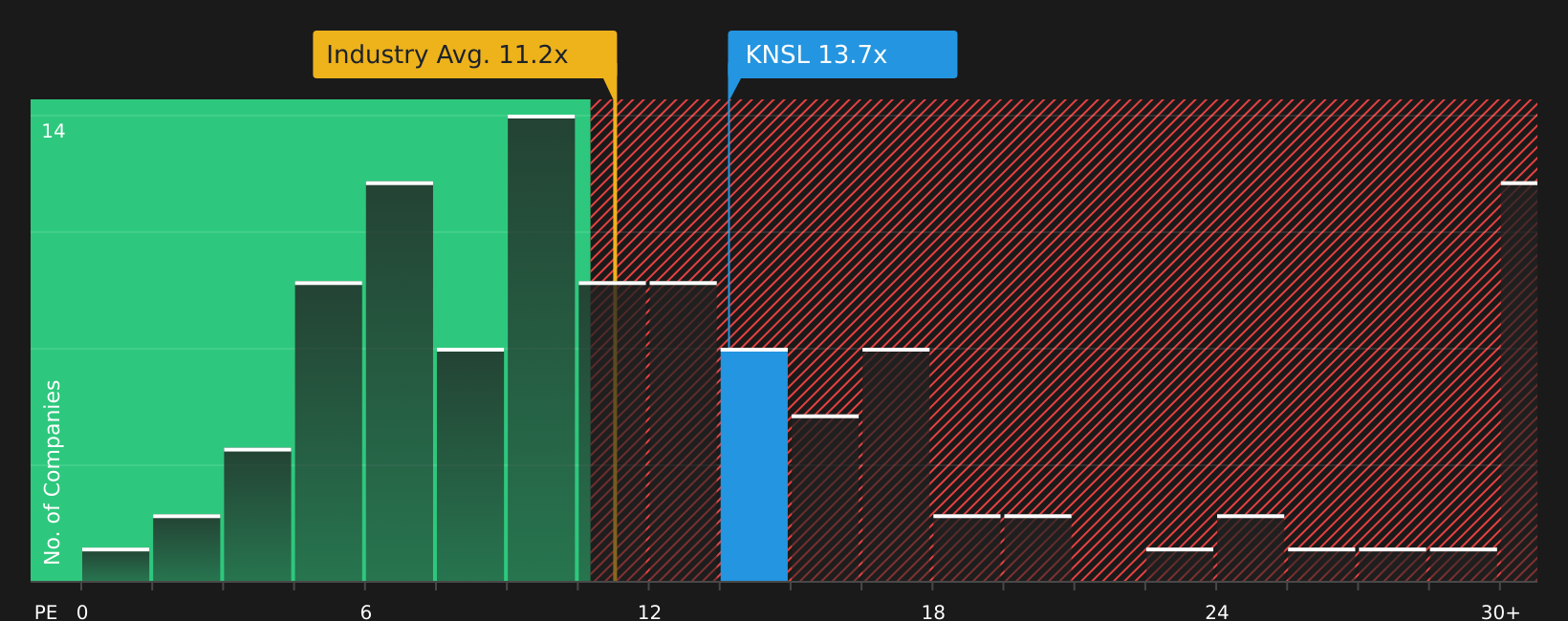

Approach 2: Kinsale Capital Group Price vs Earnings

For a profitable company, the P/E ratio is a straightforward way to see how much you are paying for each dollar of earnings. It links directly to what the business is currently earning, which many investors find easier to relate to than more complex cash flow models.

What counts as a “normal” or “fair” P/E often reflects what the market expects for future earnings and how risky those earnings appear. Higher expected growth or lower perceived risk can justify a higher P/E, while slower expected growth or higher perceived risk can be associated with a lower P/E.

Kinsale Capital Group currently trades on a P/E of 13.58x. That sits above the Insurance industry average P/E of 11.29x and the peer average of 8.01x. Simply Wall St’s Fair Ratio for Kinsale Capital Group is 11.05x. This Fair Ratio is a proprietary estimate of what the P/E might be, given factors such as earnings growth, industry, profit margin, market cap and company specific risks, rather than relying only on broad industry or peer comparisons.

Because the current P/E of 13.58x is higher than the Fair Ratio of 11.05x by more than 0.10, this approach points to the stock trading at a richer level than those fundamentals suggest.

Result: OVERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 20 top founder-led companies.

Upgrade Your Decision Making: Choose your Kinsale Capital Group Narrative

Earlier it was mentioned that there is an even better way to understand valuation, so Narratives take center stage as your way to attach a clear story about Kinsale Capital Group to hard numbers like fair value, and estimates for future revenue, earnings and margins. This links what you believe about the business to a financial forecast and then to a fair value that can be compared with the current share price.

On Simply Wall St’s Community page, Narratives are built and shared by millions of investors as an easy tool you can use without complex models. They update automatically as new information such as news or earnings is added, so your Kinsale Capital Group view stays aligned with the latest data instead of a one off snapshot.

For example, one Kinsale Capital Group Narrative might lean closer to the more optimistic fair value of about US$450, while another might anchor on the more cautious fair value of about US$309. Each Narrative spells out the assumptions behind those figures so you can decide which story feels closer to your own view and what that implies when you compare each fair value with today’s market price.

For Kinsale Capital Group, however, we'll make it really easy for you with previews of two leading Kinsale Capital Group Narratives:

🐂 Kinsale Capital Group Bull Case

Fair value in this narrative: US$356.89 per share

Implied discount to that fair value at the recent US$310.19 share price: about 13.1% undervalued

Revenue growth used in this narrative: 3.41% per year

- Analysts in this Narrative see growth opportunities in excess and surplus lines, small business property and high value homeowners, with technology and expense discipline supporting margins.

- The view assumes revenue of about US$2.1b and earnings of US$493.6m by 2029, alongside a higher future P/E of 19.8x and modest share count reduction.

- Key risks focus on tougher competition, inflation, catastrophe exposure, slower submission growth and potential reserve pressures that could challenge those earnings and margin assumptions.

🐻 Kinsale Capital Group Bear Case

Fair value in this narrative: US$309.00 per share

Implied premium to that fair value at the recent US$310.19 share price: about 0.4% overvalued

Revenue growth used in this narrative: 6.04% per year

- This more cautious Narrative highlights reliance on a very low expense ratio and technology edge, with concern that competition and widespread AI adoption could narrow those advantages over time.

- Assumptions include revenue of about US$2.2b and earnings of US$492.6m by 2029, with a future P/E of 17.4x and a discount rate of 7.0%, pointing to a fair value close to US$309.

- It also flags litigation heavy casualty lines, exposure to competitive commercial property markets and expansion into newer segments as factors that could introduce more earnings and margin volatility.

These two Narratives give you a structured bullish and bearish case built from the same underlying data set. This can help you decide which assumptions feel closer to your own view and where the current US$310.19 share price sits relative to each story.See what the community is saying about Kinsale Capital Group

Do you think there's more to the story for Kinsale Capital Group? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com