Why Bank of Hawaii (BOH) is in focus after its latest earnings

Bank of Hawaii (BOH) drew fresh attention after reporting first quarter 2026 earnings per share of $1.30, missing a widely followed estimate as lower fee income and higher expenses weighed on results.

At the same time, management pointed to firmer net interest income, healthier credit quality, and strong capital ratios. They also outlined their expectations for loan growth, net interest margin and share repurchases over the rest of 2026.

See our latest analysis for Bank of Hawaii.

At a share price of $77.79, Bank of Hawaii has a year to date share price return of 13.69%, while its 1 year total shareholder return of 21.07% suggests momentum has been building over a longer stretch, especially compared to much more modest moves over the past month and quarter.

If the latest earnings miss has you reassessing your watchlist, this can be a useful moment to broaden your search with 20 top founder-led companies

With Bank of Hawaii trading at $77.79, a 13.69% year to date gain and a 21.07% 1 year total return, plus an implied discount to both analyst targets and intrinsic value, is there still upside here, or is the stock already pricing in future growth?

Most Popular Narrative: 10.2% Undervalued

With Bank of Hawaii last closing at $77.79 against a most followed fair value estimate of $86.67, the current gap centers on how durable its core franchise really is.

Stable and "sticky" deposit base, aided by the bank's fortress local market position, is enabling effective deposit repricing and lowering the cost of funds, which supports continued improvement in net interest margin (NIM) and net interest income. Balanced, high-quality loan portfolio largely secured by local real estate with low average loan to value and high FICO scores positions Bank of Hawaii for superior asset quality and lower provision expense, preserving profitability and capital ratios over time.

Want to see what is sitting behind that confidence in profitability and capital? The narrative focuses on the interaction of revenue, margins and earnings, all filtered through a single discount rate and future earnings multiple that have a significant impact on the outcome.

Result: Fair Value of $86.67 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this hinges on Hawaii-concentrated real estate exposure and ongoing digital investment, where weaker property trends or rising technology costs could quickly challenge that undervalued story.

Find out about the key risks to this Bank of Hawaii narrative.

Another Angle On Valuation

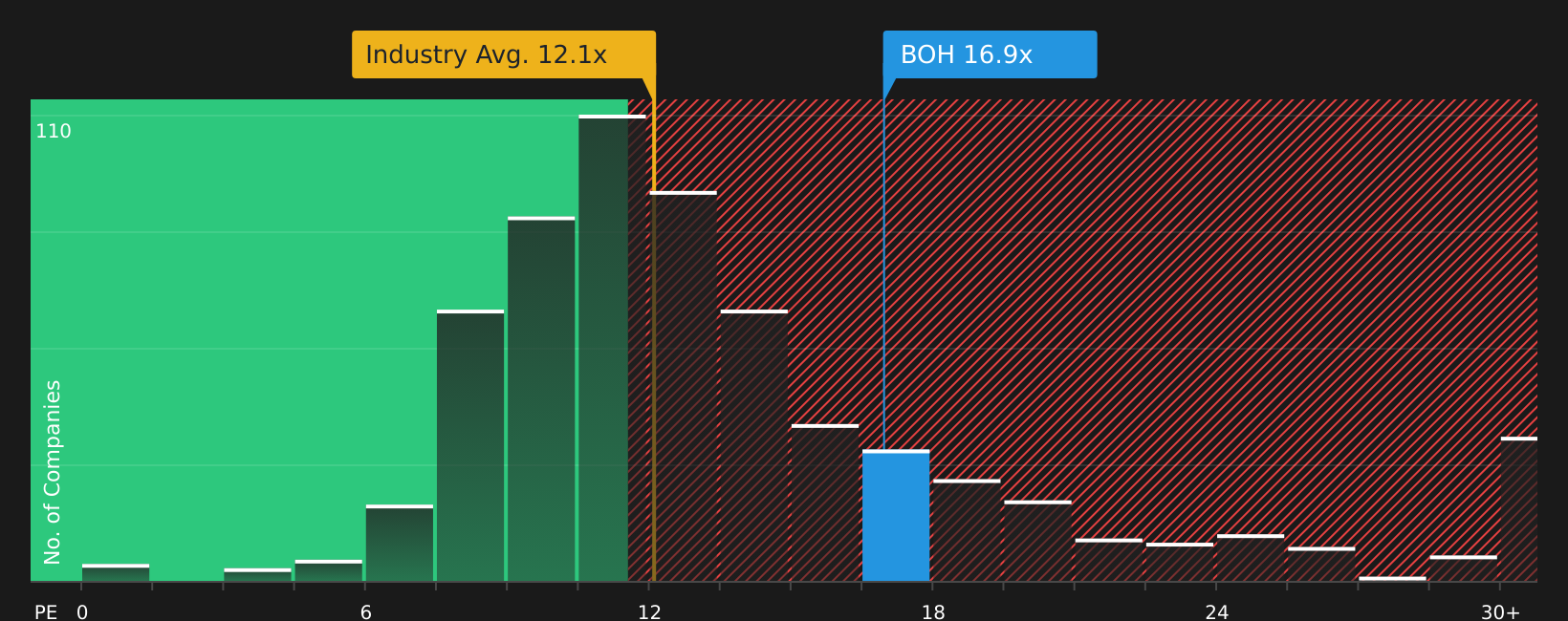

The narrative and analyst target point to Bank of Hawaii as undervalued, yet the current P/E of 15.5x sits well above both the US Banks industry at 11.5x and peer average at 10.5x, and even above a 13.8x fair ratio. That premium can be read as confidence, but also as less room for error if expectations change. See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

With mixed signals on valuation, risks and rewards, this is a good moment to review the numbers yourself and act promptly while sentiment is still forming, starting with 4 key rewards and 1 important warning sign.

Looking for more investment ideas?

Bank of Hawaii might be in focus today, but the market is full of other opportunities that could suit your goals and risk comfort.

- Target resilient potential by scanning 66 resilient stocks with low risk scores that may help cushion your portfolio when conditions get choppy.

- Hunt for quality at a discount with the 49 high quality undervalued stocks, so you are not relying on a single stock to carry your returns.

- Boost your income search by checking the 10 dividend fortresses and see which companies currently offer stronger yield potential than cash sitting on the sidelines.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com