- Wondering if Flywire's current share price makes sense, or if the stock might be mispriced? This article breaks down what the numbers say about value.

- Flywire's stock has returned 0.4% over the last week, 19.0% over the last month and 16.0% year to date, with a 46.1% return over the past year but a decline of 45.4% over three years and 53.1% over five years.

- These mixed returns highlight how sentiment toward Flywire has shifted over time, which makes understanding valuation especially important. Recent coverage has focused on how investors are reassessing growth potential against earlier share price declines, adding context to the strong 1 year return.

- Flywire currently has a valuation score of 2 out of 6. The next sections will walk through what different valuation methods imply about the stock, before ending with a broader way to think about value beyond the headline numbers.

Flywire scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

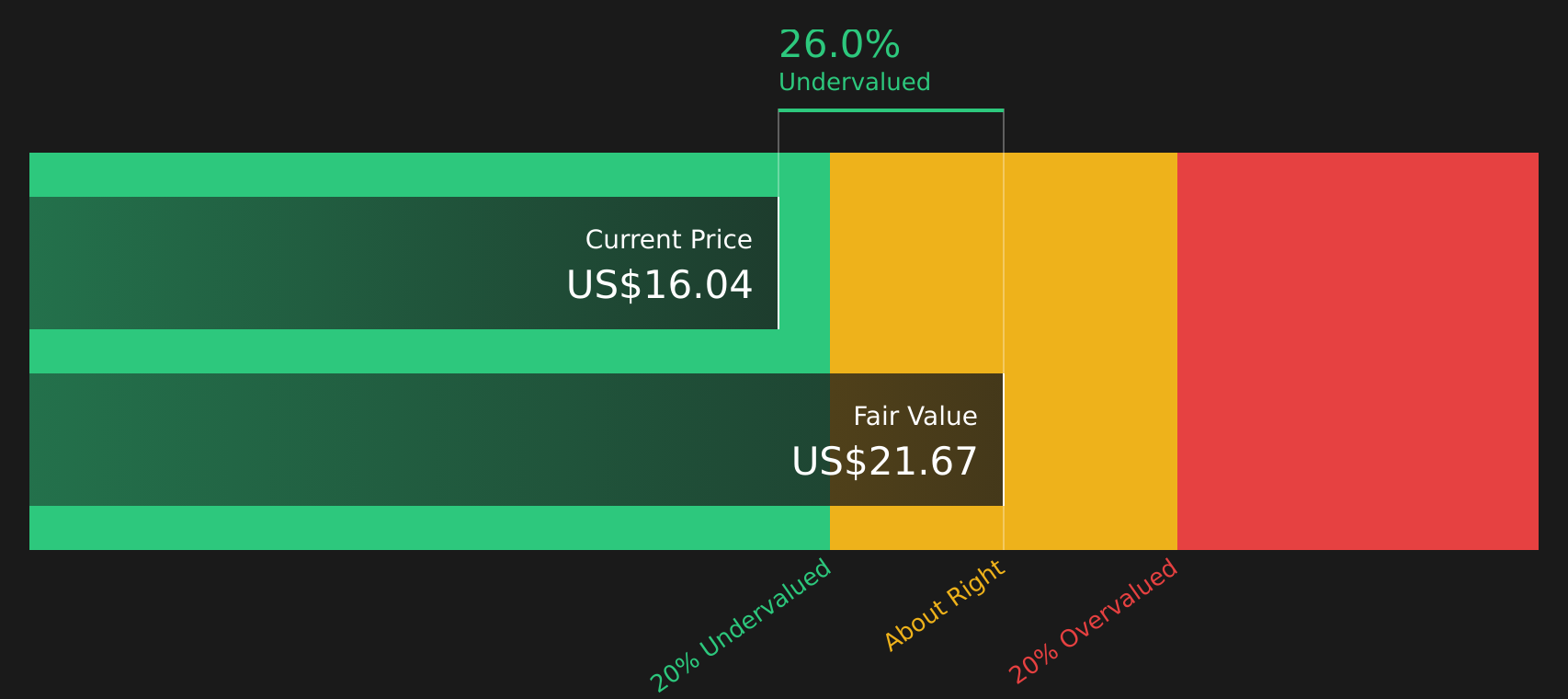

Approach 1: Flywire Excess Returns Analysis

The Excess Returns model looks at how much value a company can create above the return that shareholders require, based on its book value and earnings power. Instead of focusing on cash flows, it uses projected returns on equity to estimate what the stock could be worth today.

For Flywire, the model uses a Book Value of $6.91 per share and a Stable EPS of $1.11 per share, based on weighted future Return on Equity estimates from 4 analysts. The Average Return on Equity is 12.62%, while the Cost of Equity is $0.63 per share. That leaves an estimated Excess Return of $0.48 per share, with a Stable Book Value of $8.79 per share, again sourced from 4 analysts.

These inputs feed into an intrinsic value estimate of $21.83 per share under the Excess Returns approach. Compared with the current share price, this model indicates the stock is 26.2% undervalued.

Result: UNDERVALUED

Our Excess Returns analysis suggests Flywire is undervalued by 26.2%. Track this in your watchlist or portfolio, or discover 49 more high quality undervalued stocks.

Approach 2: Flywire Price vs Earnings

P/E is a common way to value profitable companies because it connects what you pay for each share with the earnings that support that price. In general, higher growth expectations or lower perceived risk can justify a higher P/E, while slower growth or higher risk can point to a lower, more conservative P/E being reasonable.

Flywire currently trades on a P/E of 65.93x. This is above the Diversified Financial industry average of 17.90x and also above the peer average of 11.02x, which indicates that the market is paying a much higher price for each dollar of Flywire’s earnings than for many peers.

Simply Wall St’s Fair Ratio framework estimates a P/E of 22.89x for Flywire. This is a proprietary metric that looks beyond simple comparisons and incorporates factors such as earnings growth, profit margins, risk profile, industry and market cap. Because it adjusts for these company specific features, it can offer a more tailored yardstick than using broad industry or peer averages alone.

Comparing the Fair Ratio of 22.89x with the current P/E of 65.93x, Flywire’s share price appears expensive relative to this earnings based benchmark.

Result: OVERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 20 top founder-led companies.

Upgrade Your Decision Making: Choose your Flywire Narrative

Earlier it was mentioned that there is an even better way to understand valuation, so Narratives are introduced here as a simple idea where you set out your story about Flywire, connect it to a forecast for revenue, earnings and margins, and then see what fair value that story implies.

On Simply Wall St’s Community page, Narratives let millions of investors turn this story into numbers by pairing a view on Flywire’s business with explicit assumptions and a fair value that can be compared with the current share price to help decide whether the stock looks attractive or not for their own portfolio and time horizon.

Because Narratives update when fresh information such as earnings results, news or guidance is added, your view does not stay static and you can quickly see whether the new data still fits the story you chose or if it pushes you toward a different one.

For Flywire, one investor might align with a more optimistic Narrative that assumes a fair value of US$22.00 and earnings of US$172.4 million by about 2029. Another might lean toward a more cautious Narrative that uses a fair value of US$13.00 and earnings of US$78.6 million. Comparing these ranges can help you decide which story, and which fair value, best matches your expectations.

For Flywire, however, we will make it really easy for you with previews of two leading Flywire Narratives:

Fair value in this bullish narrative: US$22.00 per share

Implied discount to this fair value vs the last close of US$16.12: about 26.7% undervalued

Revenue growth assumption: 16.94% a year

- Assumes Flywire scales its multi-vertical payments platform, with the Sertifi acquisition and software-plus-payments model helping to support higher revenue and margins across education, healthcare, B2B and travel.

- Builds in material efficiency gains from AI and automation, which are expected to support higher profitability over time while Flywire expands in markets such as Singapore, Spain, France and Latin America.

- Reflects confidence that regulatory complexity and deep client integrations create high switching costs, supporting recurring revenue strength and a higher long-term valuation multiple.

Fair value in this cautious narrative: US$13.00 per share

Implied premium to this fair value vs the last close of US$16.12: about 24.0% overvalued

Revenue growth assumption: 17.04% a year

- Assumes higher regulatory and compliance costs, plus tougher competition in cross-border payments, which could pressure margins even if revenue continues to grow.

- Builds in the risk that de-globalisation, visa policies and geopolitical tensions weigh on international student flows and transaction volumes in Flywire’s core education segment.

- Sees execution risk in expanding into new verticals and regions, with the possibility that higher customer acquisition costs and emerging technologies like blockchain limit the value that can be earned from future growth.

These two narratives frame a clear valuation range around Flywire stock, so your next step is to decide which story, assumptions and fair value line up more closely with how you see the company and its risks.

Do you think there's more to the story for Flywire? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com