Growing enthusiasm around artificial intelligence infrastructure is back in focus for Seagate Technology Holdings (STX). Investors are reacting to expectations of stronger data center storage demand, tighter industry capacity, and improving profitability signals.

See our latest analysis for Seagate Technology Holdings.

At a share price of $812.73, Seagate has seen a 30 day share price return of 38.63% and a 90 day move of 99.49%. The 1 year total shareholder return is also very large, which points to strong momentum rather than a short lived spike.

If AI storage demand has your attention, it can be useful to see how other infrastructure suppliers are trading right now. You can start with 46 AI infrastructure stocks

With Seagate now trading near its analyst target and far above some intrinsic value estimates, the key question for you is simple: is this AI storage leader still undervalued, or is the market already pricing in years of growth?

Most Popular Narrative: 5.5% Overvalued

Compared to the latest fair value estimate of $770.43, Seagate’s last close at $812.73 reflects a premium that the leading narrative still regards as modest.

Seagate is ramping up its HAMR based Mozaic drives, which represent a technological breakthrough. The transition to these drives is expected to lead to sustained and profitable growth, impacting both revenue and net margins positively.

Curious what kind of revenue curve and margin profile sit behind that fair value, and how long the market expects this AI storage cycle to run? The narrative spells out the growth math, the profitability step change, and the valuation multiple that have to line up for today’s premium price to keep making sense.

Result: Fair Value of $770.43 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, the bullish setup can quickly look different if trade policy shifts hit major customers or if high debt levels begin to limit flexibility and compress margins.

Find out about the key risks to this Seagate Technology Holdings narrative.

Another Lens On Seagate’s Valuation

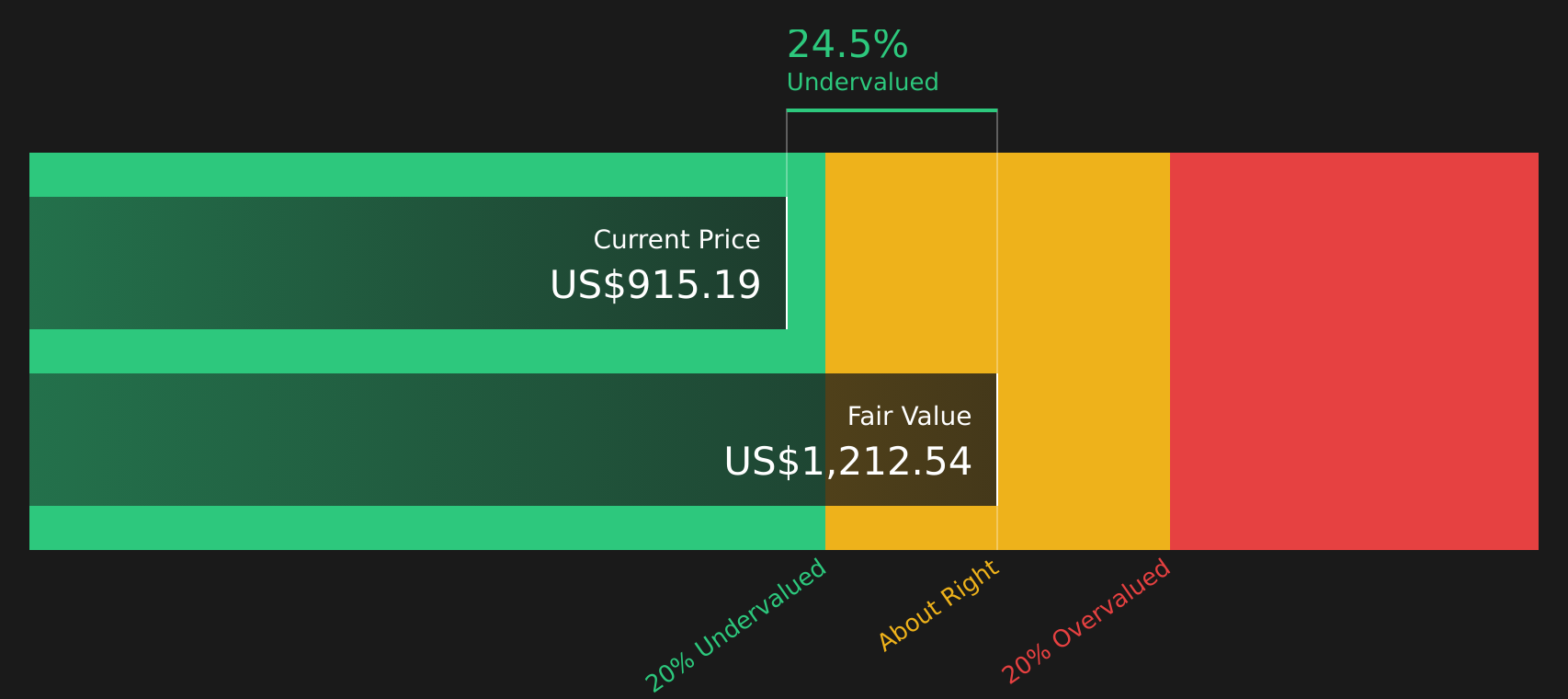

The analyst narrative tags Seagate as 5.5% overvalued at $812.73 versus a $770.43 fair value, yet our DCF model points the other way, with an estimate of $1,310.59 and an undervalued signal. When two structured models disagree this much, which set of assumptions do you trust more?

Look into how the SWS DCF model arrives at its fair value.

Next Steps

With such mixed signals on value, sentiment, and the AI storage story, it makes sense to check the numbers yourself and move quickly to shape your own view with 3 key rewards and 2 important warning signs.

Looking for more investment ideas?

If Seagate has sharpened your interest in AI and infrastructure themes, do not stop here. Broaden your watchlist now so you do not miss the next opportunity.

- Spot potential mispricings early by reviewing 49 high quality undervalued stocks, and see which stocks the data suggests may offer more value for each dollar you put to work.

- Strengthen your search for income opportunities by scanning 10 dividend fortresses, and quickly compare stocks that pair higher yields with balance sheets you can assess in one place.

- Prioritise resilience by looking through 67 resilient stocks with low risk scores, and focus your research on companies that score better on risk metrics before you commit fresh capital.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com