UGI (UGI) has just completed a US$500 million fixed income offering, issuing 6.875% senior notes due 2031 under Regulation S and Rule 144A. This move puts its capital structure in focus for shareholders.

See our latest analysis for UGI.

UGI's US$500 million note issue comes as the stock trades at US$35.65, with the share price down 5.3% year to date but supported by a 2.97% one year total shareholder return and a strong 47.65% three year total shareholder return. This suggests that recent share price pressure contrasts with a longer record of value creation.

If this refinancing has you thinking about where else capital might flow next, it could be a good moment to scan 35 power grid technology and infrastructure stocks

So with UGI raising fresh debt, a recent share price pullback, and mixed return history, is the stock quietly offering value, or is the market already pricing in everything investors expect from future growth?

Most Popular Narrative: 19.9% Undervalued

UGI's most followed narrative places fair value at $44.50 per share, compared with the recent $35.65 close, framing the refinancing against a higher long term value marker.

Divestiture of non core, low margin LPG assets and redeployment of proceeds into higher return, regulated utility and energy services businesses enable greater financial flexibility, prudent deleveraging, and improved overall earnings quality.

Want to see what sits behind that $44.50 figure? The narrative leans on steady revenue build, margin uplift, and a future earnings multiple that assumes more than just business as usual.

Result: Fair Value of $44.50 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, there are clear pressure points, including structural LPG demand erosion at UGI International and ongoing AmeriGas customer attrition, that could challenge the upside case if they persist.

Find out about the key risks to this UGI narrative.

Another View: DCF Paints A Tougher Picture

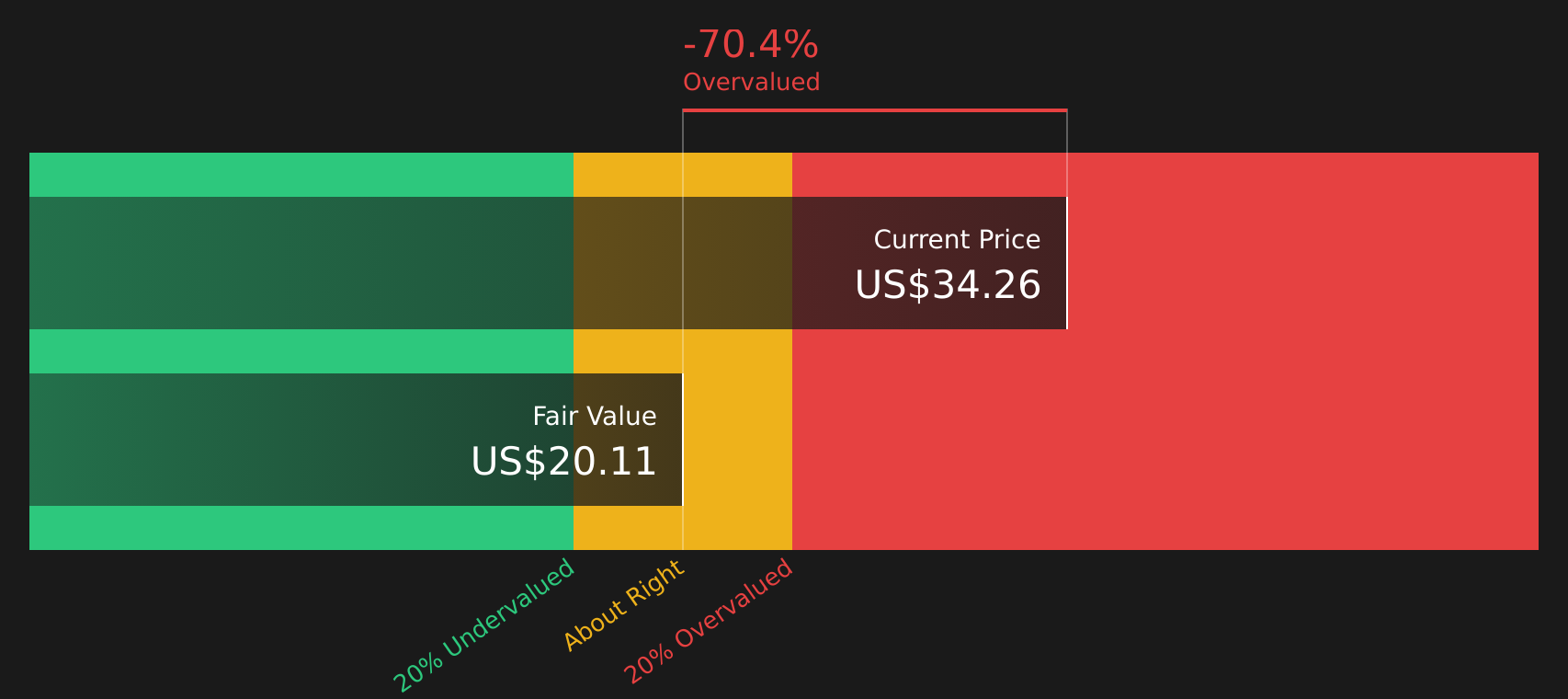

That 19.9% undervalued narrative is built around future earnings and multiples, but our DCF model lands in a very different place. On a cash flow basis, UGI screens as expensive, with our estimate of future cash flow value at $19.65 compared with the current $35.65 share price.

This gap means investors relying on DCF see much less room for error if growth or margins fall short. This raises the question of which lens you trust more when judging what today’s price really offers.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out UGI for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 49 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

Mixed signals or a clear story taking shape, the key is to weigh the evidence yourself and not wait for the crowd to decide first. Take a closer look at the 5 key rewards and 2 important warning signs.

Looking for more investment ideas?

If you stop with just one stock, you could miss opportunities that fit your goals even better, so put the Simply Wall St Screener to work for you.

- Target potential upside in quality companies by scanning 49 high quality undervalued stocks that balance solid fundamentals with prices the market may be overlooking.

- Strengthen your portfolio foundations by reviewing the solid balance sheet and fundamentals stocks screener (46 results) and focusing on businesses with healthier financial structures.

- Spot lesser known opportunities early by checking the screener containing 21 high quality undiscovered gems before they gain wider attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com