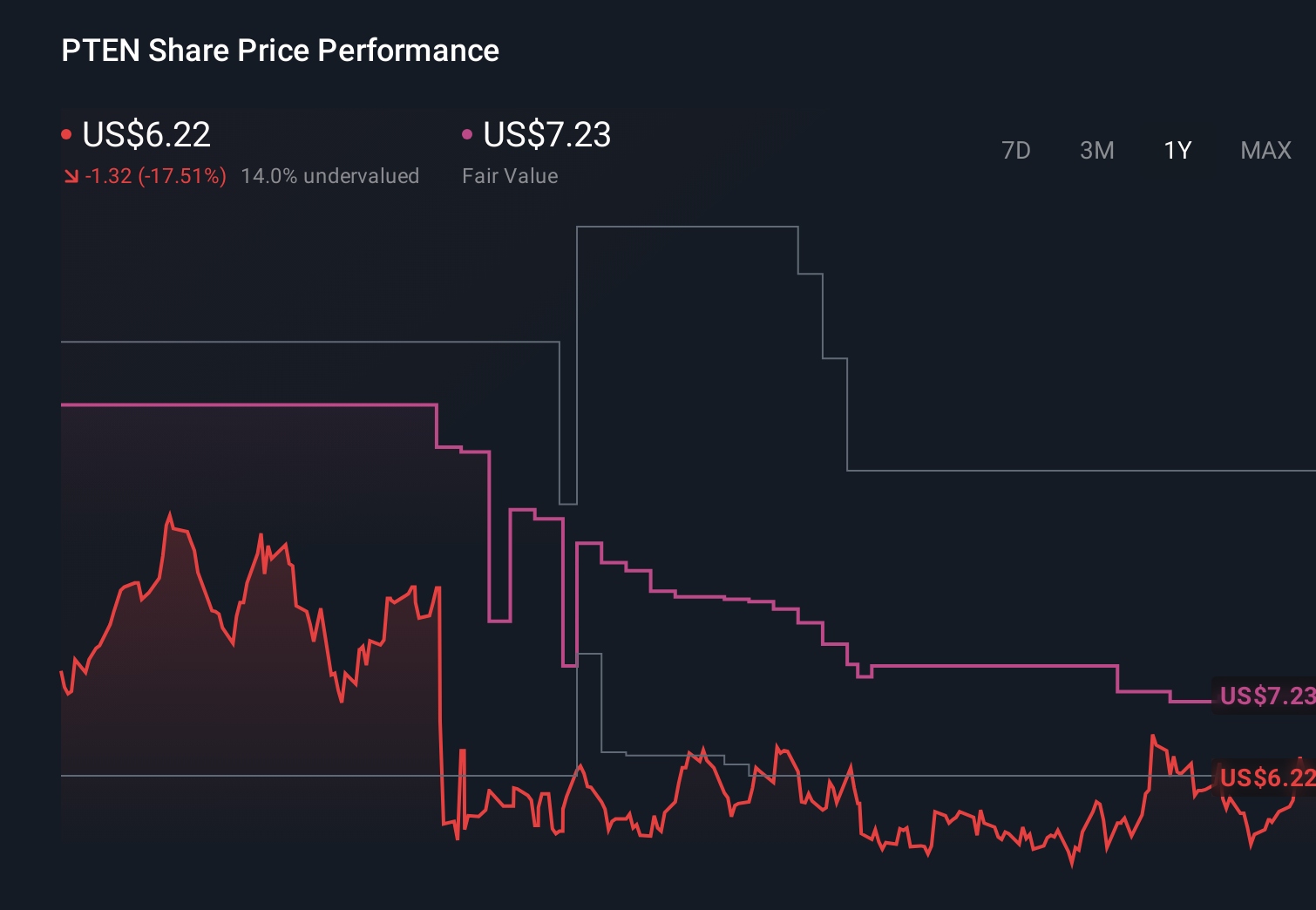

- Patterson-UTI Energy recently reported a first-quarter 2026 adjusted net loss that was narrower than expected, with revenue exceeding analyst estimates driven by its Drilling Services and Completion Services segments, and declared a quarterly dividend of US$0.10 per share payable on June 15, 2026.

- Despite year-over-year revenue declines across most business lines, upward revisions to earnings estimates and a favorable Zacks ranking highlight improving sentiment toward the company’s outlook.

- Against this backdrop of a narrower-than-expected quarterly loss, we’ll examine how the latest earnings update reshapes Patterson-UTI Energy’s investment narrative.

AI is about to change healthcare. These 34 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

Patterson-UTI Energy Investment Narrative Recap

To own Patterson-UTI Energy, you need to believe that U.S. drilling and completion activity will be healthy enough for its high-spec rigs and completion fleets to stay meaningfully utilized, and that its technology and integration efforts can eventually translate into consistent profitability. The latest quarter’s narrower-than-expected loss and revenue beat mildly support this case, but they do not remove the near term risk that softer drilling and completion demand could continue to pressure margins and delay a cleaner earnings recovery.

Against that backdrop, the recent amendment to Patterson-UTI’s US$500,000,000 revolving credit facility, which extended US$450,000,000 of commitments to 2031, stands out. For investors focused on catalysts, maintaining and extending this liquidity line matters because it helps fund ongoing capital expenditure and technology investments at a time when earnings remain negative, but it also sits directly against the risk that high capital needs could weigh on free cash flow if activity levels stay muted.

Yet behind the improving sentiment, one key risk investors should be aware of is that elevated capital spending and softer activity could still...

Read the full narrative on Patterson-UTI Energy (it's free!)

Patterson-UTI Energy's narrative projects $4.8 billion revenue and $337.4 million earnings by 2028. This requires a 1.3% yearly revenue decline and an earnings increase of about $1.4 billion from -$1.1 billion today.

Uncover how Patterson-UTI Energy's forecasts yield a $8.84 fair value, a 28% downside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were expecting revenue around US$4.8 billion and earnings of roughly US$150 million by 2029, which is far more upbeat than consensus and assumes successful margin expansion despite risks like ongoing integration challenges; after a quarter with an adjusted net loss, this news could prompt you to rethink which version of Patterson-UTI’s future you find more convincing.

Explore 3 other fair value estimates on Patterson-UTI Energy - why the stock might be worth 34% less than the current price!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Patterson-UTI Energy research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Patterson-UTI Energy research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Patterson-UTI Energy's overall financial health at a glance.

Seeking Other Investments?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- Invest in the nuclear renaissance through our list of 88 elite nuclear energy infrastructure plays powering the global AI revolution.

- We've uncovered the 10 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Uncover the next big thing with 25 elite penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com