- Krystal Biotech recently received marketing authorization from the UK Medicines and Healthcare products Regulatory Agency for VYJUVEK, a genetic therapy for dystrophic epidermolysis bullosa with COL7A1 mutations, making it the first approved genetic medicine for this condition in the UK and granting up to 12 years of orphan market exclusivity.

- The approval’s flexible at‑home or healthcare‑setting dosing, including administration by patients or caregivers, could materially influence treatment uptake and patient quality of life across this rare disease population.

- We’ll now examine how UK orphan exclusivity and at‑home dosing options for VYJUVEK could reshape Krystal Biotech’s broader investment narrative.

Uncover the next big thing with 25 elite penny stocks that balance risk and reward.

Krystal Biotech Investment Narrative Recap

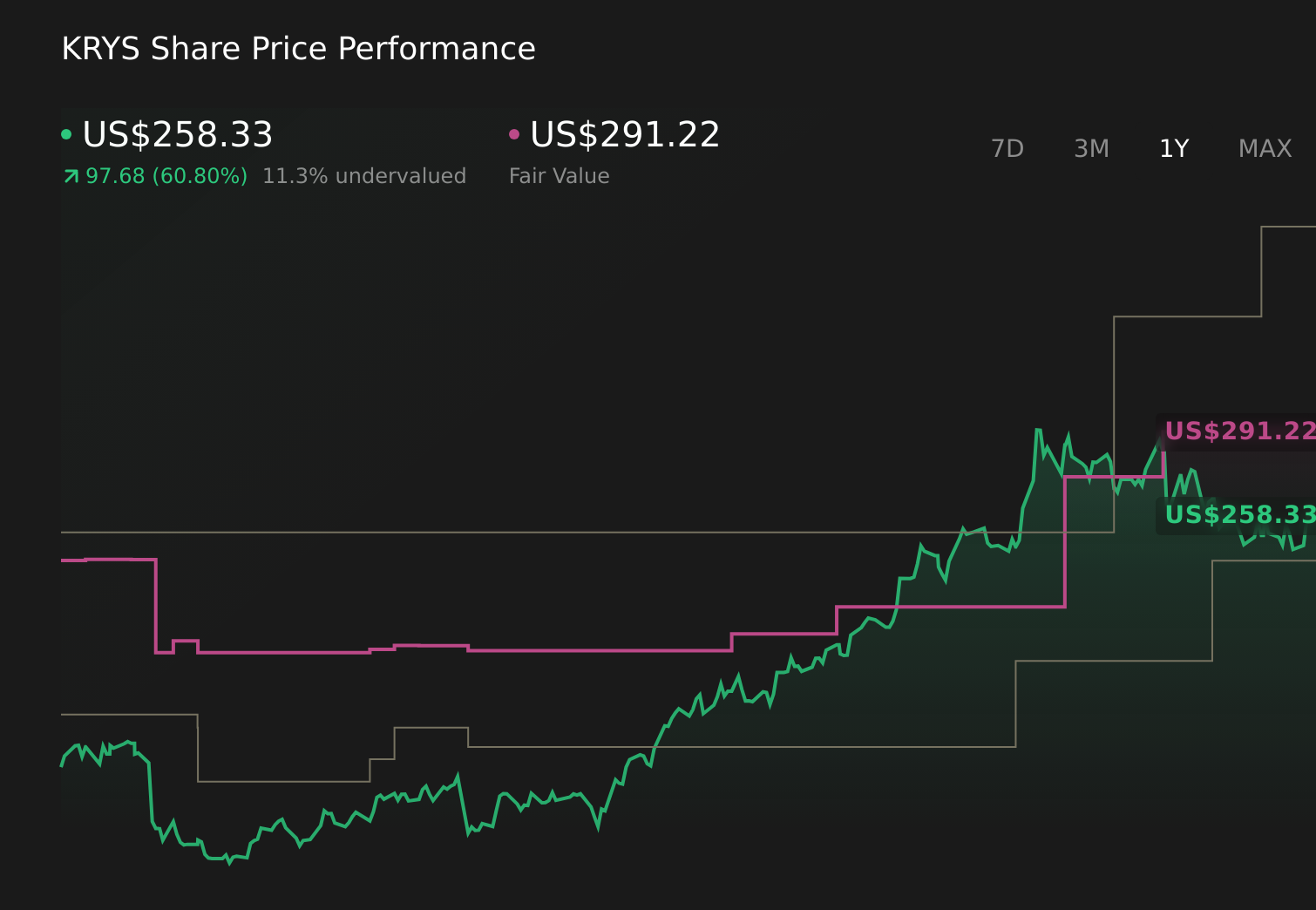

To own Krystal Biotech, you need to believe VYJUVEK can support a durable, profitable rare disease franchise while the broader gene therapy pipeline matures. The new UK approval meaningfully reinforces the near term VYJUVEK rollout story, but it does not remove the key risk of quarterly revenue volatility from unpredictable treatment patterns and heavy dependence on a single product, especially as international reimbursement decisions and patient uptake remain key swing factors.

The most relevant prior catalyst here is the April 2025 European Commission approval of VYJUVEK, which, like the UK decision, paired orphan status with flexible at home dosing. Together, EU and UK authorizations frame a clearer path for Krystal’s European rare disease business, but they also sharpen the focus on a shared risk across regions: how quickly payers finalize reimbursement and how consistently patients remain on therapy over time.

Yet behind the optimism around UK exclusivity and at home dosing, there is a less visible risk investors should be aware of around reimbursement delays and pricing pressure...

Read the full narrative on Krystal Biotech (it's free!)

Krystal Biotech's narrative projects $1.0 billion revenue and $568.7 million earnings by 2029.

Uncover how Krystal Biotech's forecasts yield a $322.78 fair value, a 8% upside to its current price.

Exploring Other Perspectives

While the UK approval strengthens the bullish view, the most pessimistic analysts were already modeling about US$797,200,000 in 2029 revenue and US$310,000,000 in earnings, reminding you that views on future reimbursement, pricing, and treatment persistence can differ sharply and may shift again as this latest decision is fully reflected in expectations.

Explore 6 other fair value estimates on Krystal Biotech - why the stock might be worth 20% less than the current price!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Krystal Biotech research is our analysis highlighting 3 key rewards that could impact your investment decision.

- Our free Krystal Biotech research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Krystal Biotech's overall financial health at a glance.

Want Some Alternatives?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- Find 48 companies with promising cash flow potential yet trading below their fair value.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 27 best rare earth metal stocks of the very few that mine this essential strategic resource.

- This technology could replace computers: discover 28 stocks that are working to make quantum computing a reality.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com