- In May 2026, Hilton Grand Vacations Inc. filed a US$61.21 million shelf registration for 1,250,000 common shares linked to its employee stock ownership plan and closed an upsized US$1.00 billion revolving warehouse facility that extends liquidity for timeshare receivables through 2029.

- By expanding receivables capacity and tying new equity issuance to employee ownership, the company is simultaneously reinforcing financing flexibility and aligning staff incentives with long-term business performance.

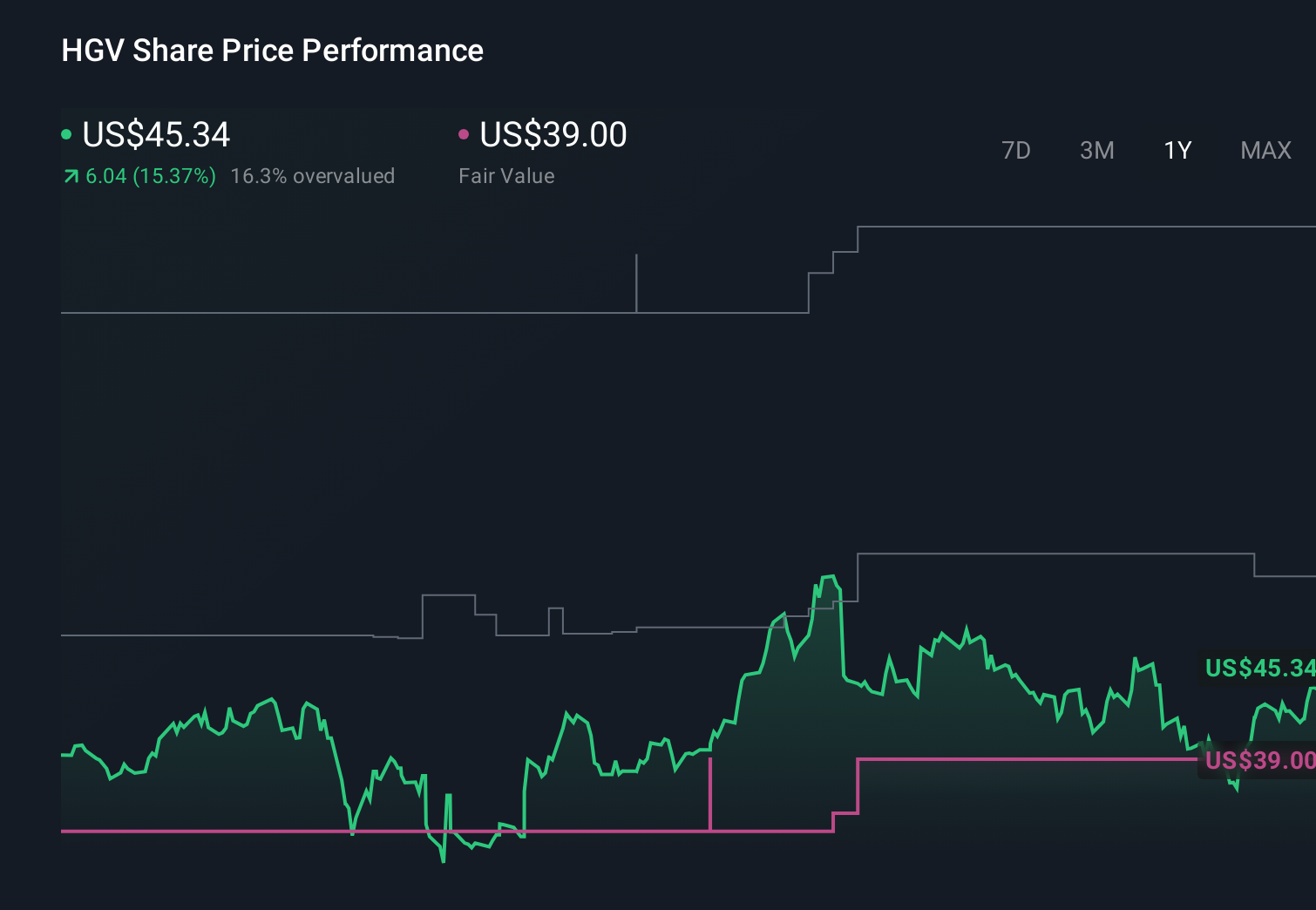

- We’ll now explore how this expanded US$1.00 billion warehouse facility shapes Hilton Grand Vacations’ existing investment narrative and risk balance.

Capitalize on the AI infrastructure supercycle with our selection of the 46 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

Hilton Grand Vacations Investment Narrative Recap

To own Hilton Grand Vacations, you need to believe its timeshare model and membership platform can keep attracting and upgrading owners while managing credit risk on its loan book. The upsized US$1.00 billion warehouse facility modestly supports the near term catalyst around receivables financing and liquidity, but it does not fully resolve the key risk of elevated bad debt and potential pressure from higher delinquencies.

The expanded revolving warehouse facility is most relevant here because it directly affects how HGV funds its US$4 billion receivables portfolio and supports sales tied to Elara in Las Vegas. By securing committed liquidity out to 2029, HGV has more room to manage owner financing and potential stress in key markets without immediately relying on more expensive funding, which interacts closely with both growth ambitions and credit quality.

Yet investors should be aware that rising defaults or tougher collection trends could still weaken earnings quality and...

Read the full narrative on Hilton Grand Vacations (it's free!)

Hilton Grand Vacations’ narrative projects $6.2 billion revenue and $472.1 million earnings by 2029. This requires 10.3% yearly revenue growth and about a $308 million earnings increase from $164.0 million today.

Uncover how Hilton Grand Vacations' forecasts yield a $56.00 fair value, a 16% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were already counting on earnings reaching about US$550 million, and the new US$1.00 billion facility could either support that view or test it if elevated defaults begin to bite.

Explore 4 other fair value estimates on Hilton Grand Vacations - why the stock might be a potential multi-bagger!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Hilton Grand Vacations research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Hilton Grand Vacations research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Hilton Grand Vacations' overall financial health at a glance.

Curious About Other Options?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- The latest GPUs need a type of rare earth metal called Dysprosium and there are only 27 companies in the world exploring or producing it. Find the list for free.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 13 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- AI is about to change healthcare. These 34 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com