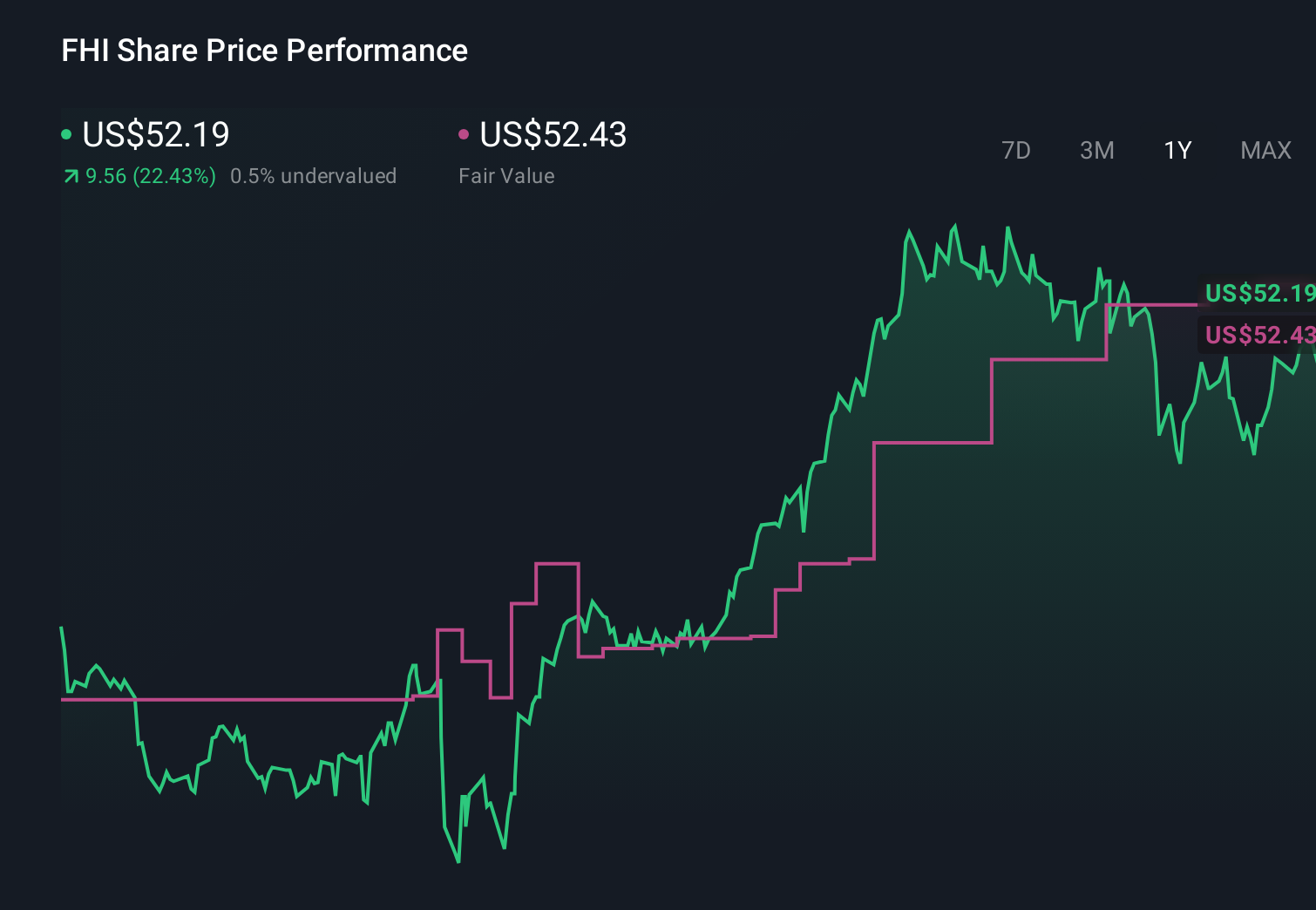

- In recent months, Federated Hermes has continued paying a US$0.38 per share dividend with a 2.77% yield, raised its annualized payout by 14.3%, and reported earnings expected to grow 2.41% year over year alongside record assets under management.

- These developments, combined with analysis earlier identifying the stock as undervalued and later supported by strong operational performance, have reinforced investor attention on its income profile and core money market franchise.

- With dividend growth front and center, we'll now examine how this operational momentum influences Federated Hermes' broader investment narrative.

Explore 29 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

Federated Hermes Investment Narrative Recap

To own Federated Hermes, you need to believe its income focused model and money market franchise can keep supporting dividends while navigating fee pressure and competition from low cost products. The latest dividend increase and modest earnings growth projections do not materially change the near term catalyst around money market fund demand, nor do they reduce the key risk that a shift in client preferences or regulation could pressure this core engine.

The 14.3% increase in the annualized dividend, to a quarterly US$0.38 per share with a 2.77% yield, is the most relevant development here, keeping the income story in focus. It ties directly into the catalyst of growing demand for cash and income solutions, but also sharpens the risk that any setback in money market profitability or assets under management could quickly matter more to shareholders than the recent record AUM headlines.

Yet investors should be aware that the company’s reliance on money market funds leaves it more exposed if...

Read the full narrative on Federated Hermes (it's free!)

Federated Hermes' narrative projects $2.0 billion revenue and $422.2 million earnings by 2029.

Uncover how Federated Hermes' forecasts yield a $57.14 fair value, a 4% upside to its current price.

Exploring Other Perspectives

Four members of the Simply Wall St Community currently see fair value between US$52.35 and US$69.06, reflecting a wide spread of expectations. You can weigh these views against the central risk that fee compression and rising competition in active management could pressure margins and ultimately shape how the company’s performance aligns with any of those estimates.

Explore 4 other fair value estimates on Federated Hermes - why the stock might be worth just $52.35!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Federated Hermes research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Federated Hermes research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Federated Hermes' overall financial health at a glance.

Contemplating Other Strategies?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- Invest in the nuclear renaissance through our list of 88 elite nuclear energy infrastructure plays powering the global AI revolution.

- Uncover the next big thing with 25 elite penny stocks that balance risk and reward.

- Capitalize on the AI infrastructure supercycle with our selection of the 47 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com