Recent performance snapshot

Wells Fargo (WFC) has recently drawn attention after its stock closed at US$77.52, with returns up 1.47% over the past day but down over the month and the past 3 months.

See our latest analysis for Wells Fargo.

That short term bounce sits against a weaker stretch, with the share price down 18.57% year to date but a 3 year total shareholder return above 100% showing longer term holders have still been rewarded.

If Wells Fargo’s recent moves have you reassessing the financial sector, this is a good moment to broaden your watchlist and check out 20 top founder-led companies

With Wells Fargo shares down so far this year but supported by multi year total returns above 100%, plus an indicated discount to some valuation estimates, is there still a buying opportunity here, or has the market already priced in future growth?

Most Popular Narrative: 3.8% Overvalued

At a last close of $77.52 against a fair value narrative of $74.70, the current price sits slightly above what that framework suggests.

One of the reasons for its undervaluation is related to the broader economic environment, particularly the sluggishness in the housing and manufacturing sectors. However, Wells Fargo has significant advantages, such as a wide economic moat from its large customer base and low funding costs. Additionally, potential regulatory changes, like the lifting of the asset cap that limits the bank's growth, could drive future profitability.

This narrative from mschoen25 focuses on future earnings power, richer profit margins, and a valuation multiple that edges closer to higher-growth financial stocks.

Result: Fair Value of $74.70 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this narrative could be challenged if regulatory constraints such as the asset cap persist for longer, or if housing and manufacturing weakness drags on credit quality.

Find out about the key risks to this Wells Fargo narrative.

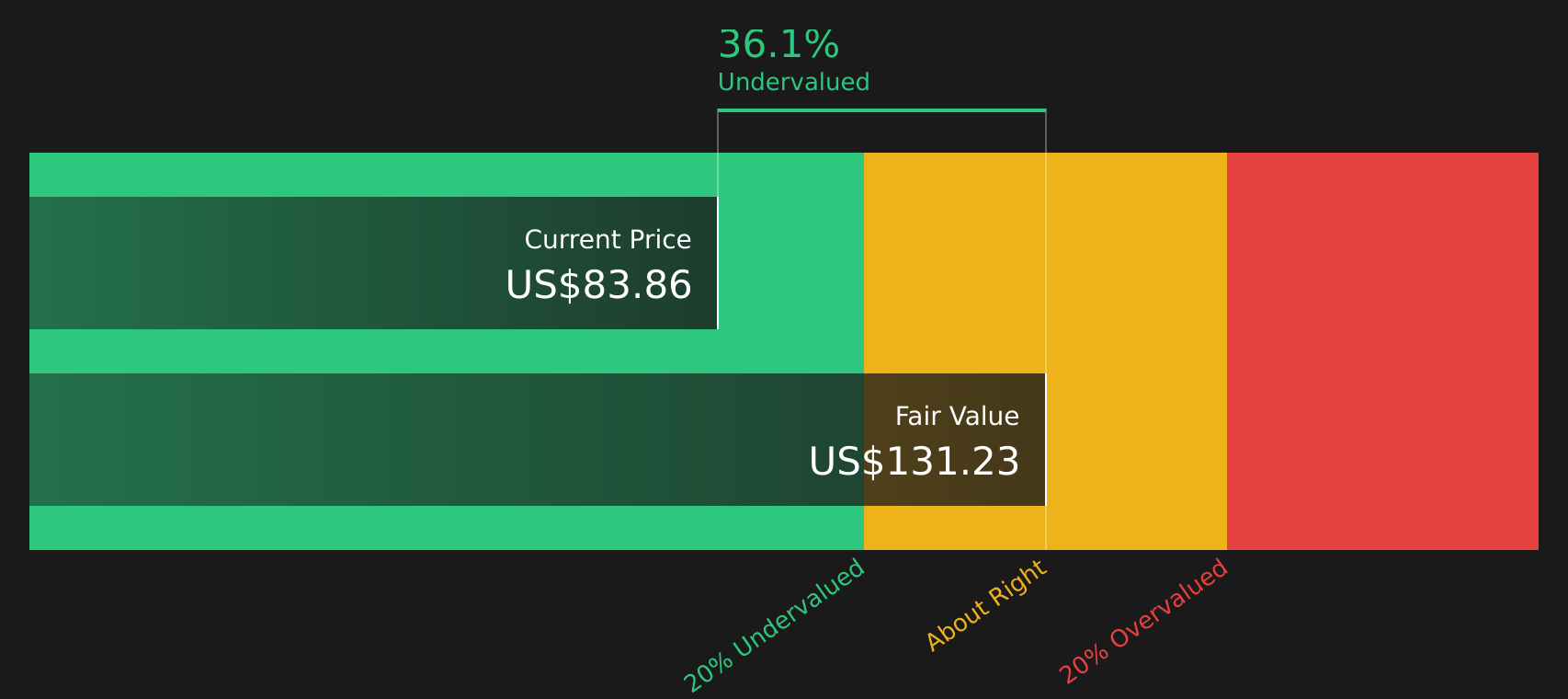

Another View: Cash Flow Points to Deep Undervaluation

While the popular narrative pegs Wells Fargo as 3.8% overvalued around $77.52 versus a $74.70 fair value, the SWS DCF model paints a very different picture, suggesting fair value nearer $129.56. That gap implies either an overly cautious narrative or cash flow assumptions that prove too optimistic. Which side are you on?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Wells Fargo for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 46 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With mixed signals on valuation and sentiment, this is a good time to review the data yourself and decide where you stand on Wells Fargo. To round out your view, take a look at the 4 key rewards and 1 important warning sign

Looking for more investment ideas?

If Wells Fargo has your attention, do not stop there. Use targeted stock lists to uncover fresh ideas that fit your goals before the crowd notices.

- Target value opportunities by reviewing companies highlighted in the 46 high quality undervalued stocks that combine quality fundamentals with attractive pricing signals.

- Prioritize resilience and capital preservation by scanning the 65 resilient stocks with low risk scores to spot stocks with lower overall risk profiles.

- Strengthen your core holdings by checking the solid balance sheet and fundamentals stocks screener (46 results) and focus on companies backed by healthier balance sheets and fundamentals.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com