Centuri Holdings (CTRI) has drawn fresh attention after reporting Q1 2026 revenue up 31% year over year and gross profit up 76%, alongside $1.3b in bookings and a backlog reaching $6.5b.

See our latest analysis for Centuri Holdings.

At a share price of $31.32, Centuri’s recent 3.71% 1 day and 8.15% 7 day share price returns follow a period where the 30 day share price return fell 9.84%. The year to date share price return of 21.30% and 1 year total shareholder return of 58.02% show notable recent performance around its growth plan and record backlog.

If Q1’s strong bookings and “Vision One Centuri” plan have you thinking about longer term infrastructure themes, it could be a good time to assess 35 power grid technology and infrastructure stocks

With Centuri trading at $31.32 and data pointing to an implied discount to some valuation estimates, the key question is whether the recent gains still leave upside on the table or if the stock already reflects future growth.

Most Popular Narrative: 28.7% Overvalued

At $31.32, Centuri trades above the most followed fair value estimate of $24.33, which is built using a 9.66% discount rate and detailed earnings forecasts.

In order for you to agree with the analysts, you would need to believe that by 2028, revenues will be $3.7 billion, earnings will come to $123.6 million, and it would be trading on a PE ratio of 23.1x, assuming you use a discount rate of 9.7%.

Curious what sits behind that earnings jump, margin shift, and lower future P/E multiple assumption? Those moving parts drive the fair value math, and the full narrative ties them together.

Result: Fair Value of $24.33 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, if contract wins from the $13b pipeline or margin gains from higher priced project work exceed current assumptions, that overvaluation narrative could look very different.

Find out about the key risks to this Centuri Holdings narrative.

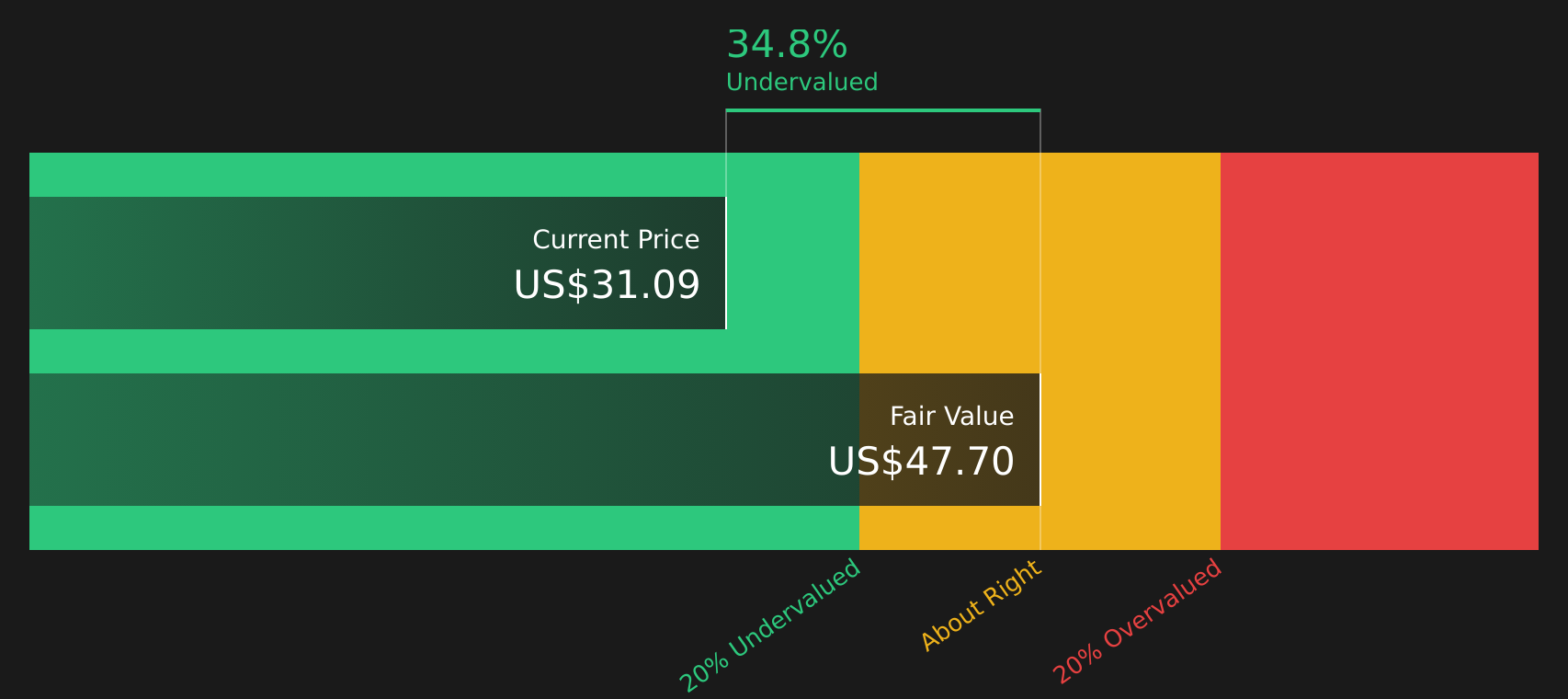

Another View: Cash Flows Point the Other Way

Analysts see Centuri as 28.7% overvalued at $31.32 against a $24.33 fair value, but our DCF model paints a different picture, with a future cash flow value of $47.13. That implies the stock trades at a 33.5% discount. The question is which story should guide your expectations?

For a closer look at how this cash flow view is built, and where the key assumptions sit, Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Centuri Holdings for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 46 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With sentiment mixed between overvaluation concerns and supportive cash flow and growth assumptions, it makes sense to move quickly and stress test the data yourself. To balance both sides of the story, start by weighing 3 key rewards and 2 important warning signs

Looking for more investment ideas?

If Centuri has sparked your interest, do not stop here, the wider market holds plenty of other opportunities that could suit your style and risk comfort.

- Target potential mispricings by scanning 46 high quality undervalued stocks where solid fundamentals and attractive valuations come together in one focused list.

- Strengthen your income approach by reviewing 10 dividend fortresses that aim to combine higher yields with resilience through different conditions.

- Protect your capital first by checking 65 resilient stocks with low risk scores built around companies with steadier profiles and lower risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com