- In recent days, progress toward an Iran-US peace deal has coincided with a pullback in crude oil and diesel prices, easing fuel costs for logistics-intensive businesses such as Carvana.

- Because Carvana’s model relies heavily on long-distance vehicle transport, lower fuel prices could meaningfully reduce operating expenses and improve its cost efficiency.

- We’ll now explore how easing fuel and logistics costs might influence Carvana’s existing investment narrative and expectations for its business model.

Explore 28 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

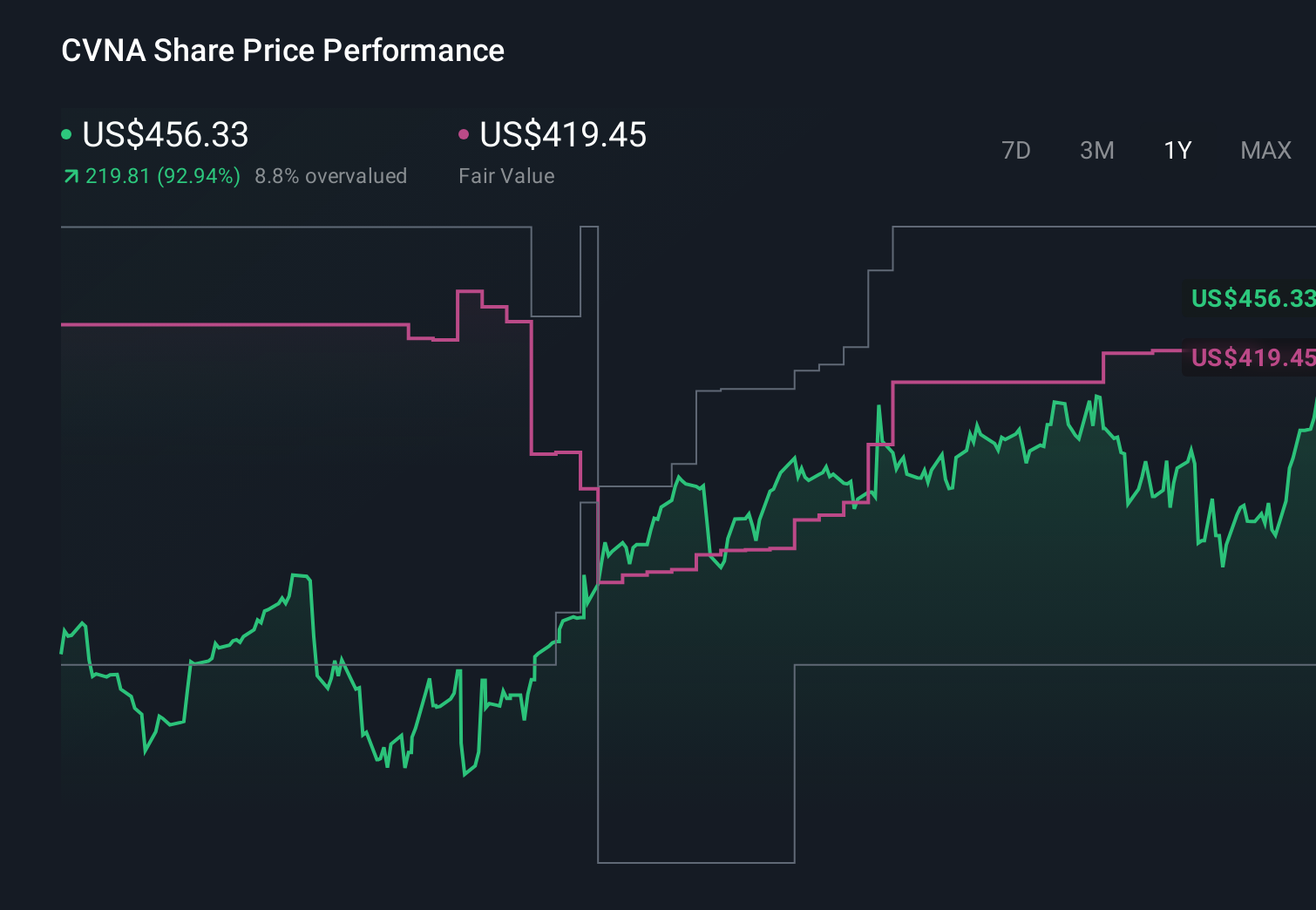

Carvana Investment Narrative Recap

To own Carvana, you generally need to believe its online, logistics heavy model can scale efficiently while maintaining profitability. The recent pullback in oil and diesel helps the near term margin story, but it does not remove key execution risks around reconditioning, logistics utilization and marketing spend. The most important short term catalyst still sits in Carvana’s ability to grow units through its expanding infrastructure without letting per unit costs creep higher.

In that context, the ongoing build out of Inspection and Reconditioning Center capabilities at ADESA sites like Chicago and Syracuse looks especially relevant. Lower fuel costs can complement these investments by easing delivery and inbound transport expenses, potentially improving the economics of faster local and next day delivery. How well these new facilities ramp toward efficient utilization remains central to whether lower fuel prices translate into sustained margin benefits.

Yet beneath the benefit of cheaper fuel, investors should be aware that Carvana’s high capital needs and debt load could still...

Read the full narrative on Carvana (it's free!)

Carvana's narrative projects $40.2 billion revenue and $3.0 billion earnings by 2029.

Uncover how Carvana's forecasts yield a $428.50 fair value, a 483% upside to its current price.

Exploring Other Perspectives

Some of the lowest estimate analysts were already assuming margins would shrink to 4.5 percent on about US$38.4 billion of revenue, so even with cheaper fuel, you should recognize how differently people can view Carvana’s capital intensity and execution risks and consider how this news might shift those expectations.

Explore 13 other fair value estimates on Carvana - why the stock might be worth over 5x more than the current price!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Carvana research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Carvana research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Carvana's overall financial health at a glance.

Seeking Other Investments?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- The latest GPUs need a type of rare earth metal called Terbium and there are only 29 companies in the world exploring or producing it. Find the list for free.

- The future of work is here. Discover the 34 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Find 46 companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com