- In late May 2026, Photronics, Inc. reported fiscal second-quarter results showing largely flat sales at US$209.94 million year over year but a sharp increase in net income to US$31.43 million, while also issuing third-quarter guidance that pointed to softer revenue and operating margins than many investors had anticipated.

- The company attributed its weaker outlook to delayed semiconductor design releases, elevated fab utilization, memory supply bottlenecks, and geopolitical uncertainty, even as it continued spending to expand advanced photomask capacity in the U.S. and Korea.

- Now we’ll examine how this weaker-than-expected revenue guidance and commentary on industry bottlenecks affects Photronics’ previously steady investment narrative.

AI is about to change healthcare. These 40 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

Photronics Investment Narrative Recap

To own Photronics, you need to believe that demand for complex photomasks tied to advanced chips and OLED displays will support earnings over time, despite industry swings. The latest quarter’s soft revenue guidance and commentary on delayed designs directly affects the near term catalyst of higher utilization in advanced nodes, while also underlining the key risk that tight fab capacity and memory bottlenecks can quickly unsettle quarterly results.

The most relevant update here is Photronics’ Q3 fiscal 2026 outlook for revenue of US$207 million to US$215 million and operating margins of 18% to 20%. This guidance, issued alongside flat Q2 sales but much higher net income, brings the risk of unpredictable quarterly revenue and earnings into sharper focus, given the company’s short order visibility and exposure to cyclical IC and display design activity.

Yet investors should be aware that limited order backlog visibility and exposure to abrupt design delays can...

Read the full narrative on Photronics (it's free!)

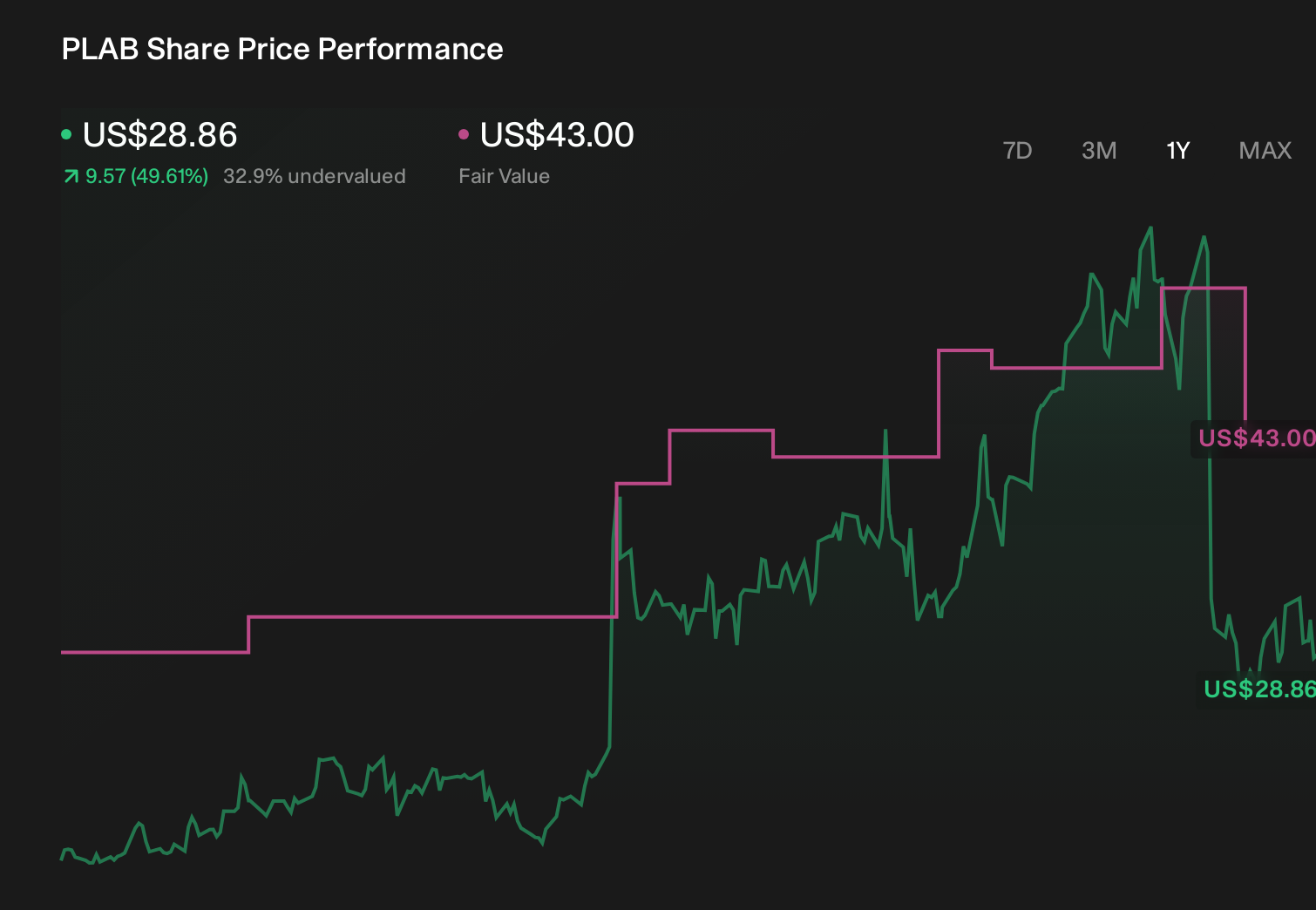

Photronics’ narrative projects $973.4 million revenue and $138.1 million earnings by 2029.

Uncover how Photronics' forecasts yield a $51.50 fair value, a 62% upside to its current price.

Exploring Other Perspectives

Six fair value estimates from the Simply Wall St Community span roughly US$22 to US$52 per share, reflecting a wide range of expectations. Against this backdrop, the recent weaker revenue guidance and industry bottlenecks highlight why understanding differing views on Photronics’ earnings resilience matters if you want to compare several perspectives before deciding.

Explore 6 other fair value estimates on Photronics - why the stock might be worth as much as 62% more than the current price!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Photronics research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Photronics research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Photronics' overall financial health at a glance.

Searching For A Fresh Perspective?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Find 48 companies with promising cash flow potential yet trading below their fair value.

- Uncover the next big thing with 24 elite penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com