Weyerhaeuser (WY) is back on investors’ radar after its recent trading session, with the stock closing at $24.39 and posting measured moves over the past week, month and past 3 months.

See our latest analysis for Weyerhaeuser.

Recent trading has been mildly positive, with the 1 day share price return of 2.87% and year to date share price return of 2.48% contrasting with a 1 year total shareholder return that is down 3.18%. This suggests momentum is improving in the short term but still subdued over a longer horizon.

If you are looking beyond timber and real estate, this could be a good moment to see what else is moving and check out 33 power grid technology and infrastructure stocks

With Weyerhaeuser trading at $24.39 against an analyst price target of $31.18 and an indicated intrinsic discount of 78%, you have to ask: is this a genuine value opportunity, or is the market already pricing in future growth?

Most Popular Narrative: 22.7% Undervalued

Against the latest close at $24.39, the most followed narrative puts Weyerhaeuser's fair value at $31.55, which frames the analyst enthusiasm behind the stock.

The analysts have a consensus price target of $31.55 for Weyerhaeuser based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $38.0, and the most bearish reporting a price target of just $27.0.

Want to see what is behind that fair value gap? The narrative leans on a tighter share count, rising margins and a future earnings profile usually associated with higher growth stocks.

Result: Fair Value of $31.55 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this depends on risks such as weaker lumber demand or additional trade and tariff pressures, which could limit pricing power and reduce earnings expectations.

Wall Street's queuing for one rocket. While SpaceX counts down to its IPO, other companies tied to the new space race are already in orbit. → 20 Compelling Space Companies watchlist · Global Space Race Investing Ideas screener · Scan the sector by valuation on Rocket Lab's valuation page.

Another Way To Look At Valuation

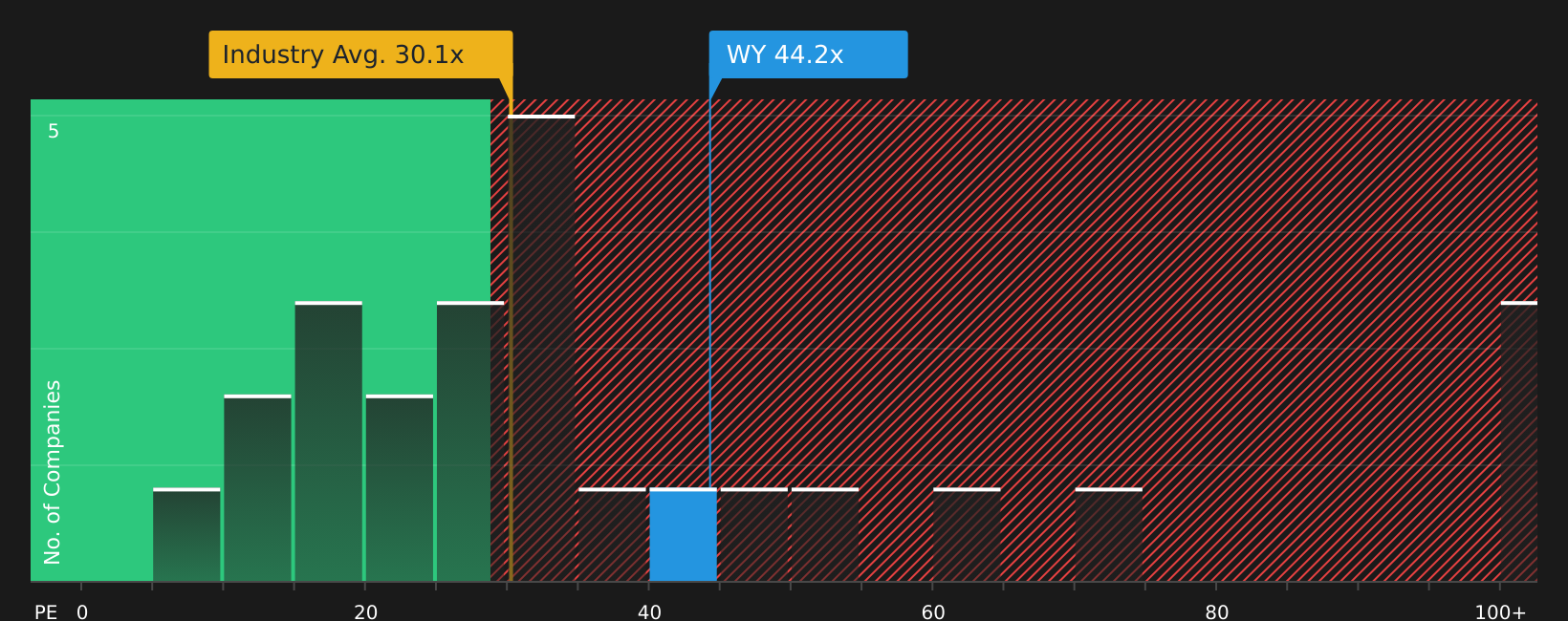

The analyst narrative leans on earnings and fair value estimates, but the current P/E of 44.3x tells a different story. It sits slightly above both the 43.6x fair ratio and the 30.4x industry average. This points to richer pricing and less margin for error if expectations shift. Is that a premium you are comfortable with?

See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

With sentiment mixed after reviewing valuation, growth assumptions, and industry context, it makes sense to move quickly, review the underlying data, and decide where you stand on 3 key rewards and 3 important warning signs

Looking for more investment ideas?

If you stop with one stock, you risk missing other opportunities. Take a few minutes to scan fresh ideas built from consistent, data driven filters.

- Target potential upside by reviewing companies that screen as 47 high quality undervalued stocks based on cash flows and balance sheet strength.

- Prioritise resilience by checking stocks highlighted in the 63 resilient stocks with low risk scores that focus on steadier risk profiles.

- Spot less crowded opportunities by scanning the screener containing 22 high quality undiscovered gems that combine quality fundamentals with lower market attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com