Why Marathon Petroleum (MPC) Is Back on Investors’ Radar

Marathon Petroleum (MPC) is attracting fresh attention after recent share price strength, with the stock up around 1.6% over the past day, 8.2% in the past week, and 6% over the past month.

See our latest analysis for Marathon Petroleum.

The latest move fits into a strong run, with the 90 day share price return at 22.9% and the year to date share price return at 61.8%, while the 1 year total shareholder return stands at 73.6%. This points to momentum that investors are watching closely.

If this kind of strength has you looking around the energy space, it could be a good moment to scan other power grid and infrastructure plays using the 33 power grid technology and infrastructure stocks

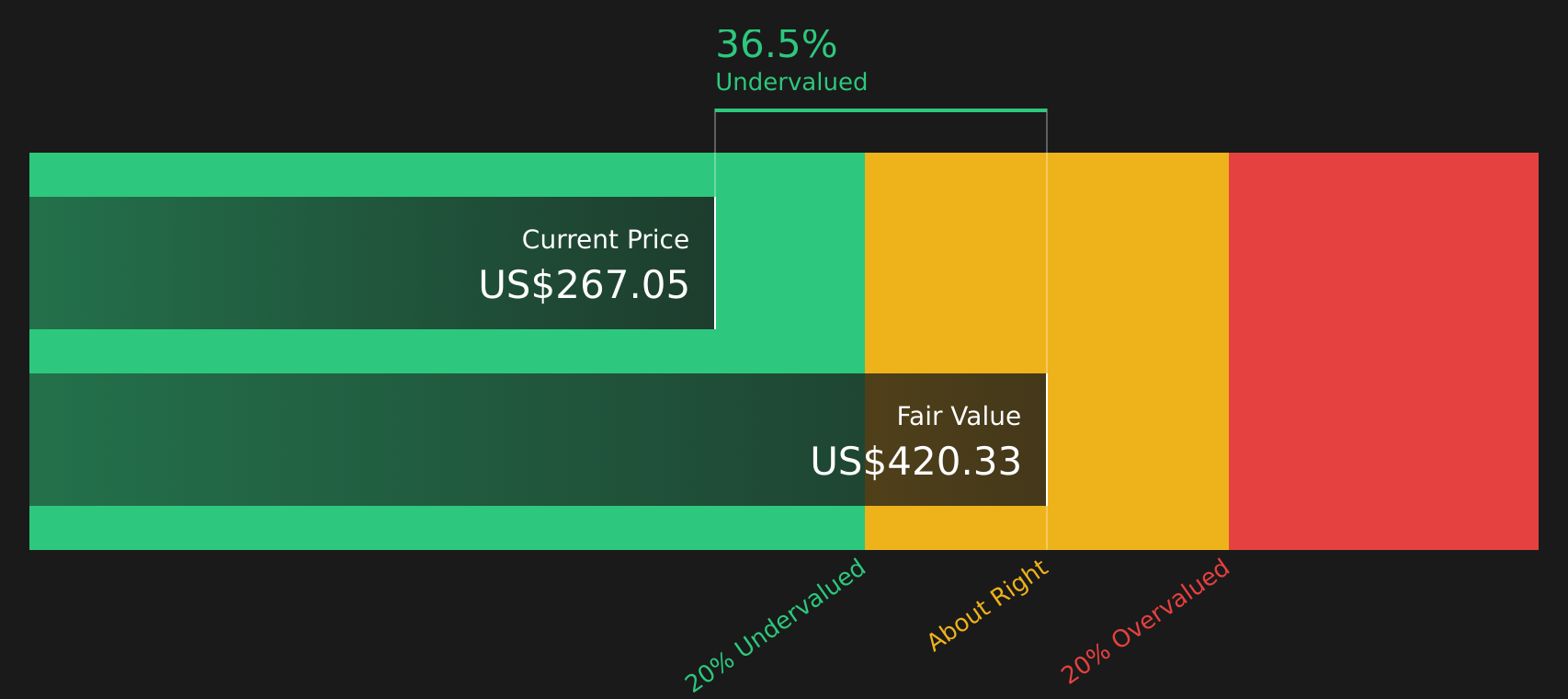

With Marathon trading around US$267 and an analyst price target near US$265, recent gains may suggest a lot of good news is already reflected in the stock. This raises the question of whether there is still a buying opportunity or if the market is already pricing in future growth.

Most Popular Narrative: 4% Overvalued

Analysts following Marathon Petroleum see fair value at about $256.83 per share, slightly below the last close of $267.21, which puts the current rally into context.

Disciplined capital allocation through continued share buybacks, increasing MPLX distributions, and maintenance of an investment-grade balance sheet are set to drive higher earnings per share and sustained shareholder returns, aligning with positive long-term company trends.

Want to see what that discipline looks like on a spreadsheet, not just in headlines? The narrative leans on earnings, margins, and a valuation multiple that has to compress from today’s level. Curious how those pieces fit together into that fair value number?

Result: Fair Value of $256.83 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, that story can shift quickly if long term fuel demand fades faster than expected, or if environmental rules make Marathon’s refining footprint less profitable.

Wall Street's queuing for one rocket. While SpaceX counts down to its IPO, other companies tied to the new space race are already in orbit. → 20 Compelling Space Companies watchlist · Global Space Race Investing Ideas screener · Scan the sector by valuation on Rocket Lab's valuation page.

Another View: Cash Flows Tell a Different Story

The analyst-based fair value of $256.83 suggests Marathon Petroleum is about 4% overvalued relative to that price target. Yet the SWS DCF model points to an estimated future cash flow value of $420.33 per share, implying the stock is trading at a steep discount. Which lens do you think fits your own assumptions better?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Marathon Petroleum for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 47 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

Reading all this and still on the fence about Marathon Petroleum’s momentum and valuation? Act while the data is fresh and weigh up the 3 key rewards and 2 important warning signs

Looking for more investment ideas?

If Marathon Petroleum has caught your attention, do not stop there. Widen your watchlist now so you are not the one hearing about the next opportunity late.

- Target potential mispricings by scanning 47 high quality undervalued stocks that combine strong fundamentals with prices that may not fully reflect their financial profile.

- Strengthen your income stream by reviewing 10 dividend fortresses that focus on higher yielding payouts with an emphasis on resilience.

- Reduce portfolio stress by checking 63 resilient stocks with low risk scores built around companies with more measured risk profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com