Recent share performance and why Dropbox is back on investors’ radar

Dropbox (DBX) has drawn fresh attention after the stock gained about 7% over the past month and around 4% over the past 3 months, prompting investors to reassess the company’s current valuation and financial profile.

See our latest analysis for Dropbox.

At a share price of $27.20, Dropbox’s 7.04% 1 month share price return and 3.86% 7 day share price return suggest momentum has picked up recently, even though the 1 year total shareholder return declined 7.83% and the 5 year total shareholder return declined 8.57%.

If this shift in sentiment has you looking beyond a single stock, it could be a good moment to scan other opportunities and see which AI related platforms are gaining traction through the 31 AI small caps

With Dropbox trading at $27.20, sitting close to analysts’ average price target but with an intrinsic value model suggesting a large discount, you have to ask: is this a genuine mispricing, or is the market already banking on future growth?

Most Popular Narrative: 4% Overvalued

At $27.20, Dropbox trades slightly above the most followed narrative fair value of $26.17, setting up a tight debate around what really drives that figure.

The planned expansion and deeper integration of AI-driven productivity tools (Dash), including upcoming self-serve offerings and seamless bundling with Dropbox's existing file sync-and-share product, position the company to capture higher ARPU and accelerate recurring revenue growth as digital transformation and hybrid work drive demand for intelligent, collaborative cloud platforms.

Want to see what sits behind that AI push and the higher recurring revenue focus? The narrative leans on specific margin, growth and valuation assumptions that are not obvious from the headline numbers. The key moving parts are already mapped out. The only way to judge if they stack up is to see them in full.

Result: Fair Value of $26.17 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, the narrative still faces pressure from falling revenue and paying users, as well as intense competition from bundled suites that can squeeze pricing and margins.

Wall Street's queuing for one rocket. While SpaceX counts down to its IPO, other companies tied to the new space race are already in orbit. → 20 Compelling Space Companies watchlist · Global Space Race Investing Ideas screener · Scan the sector by valuation on Rocket Lab's valuation page.

Another view on Dropbox’s valuation

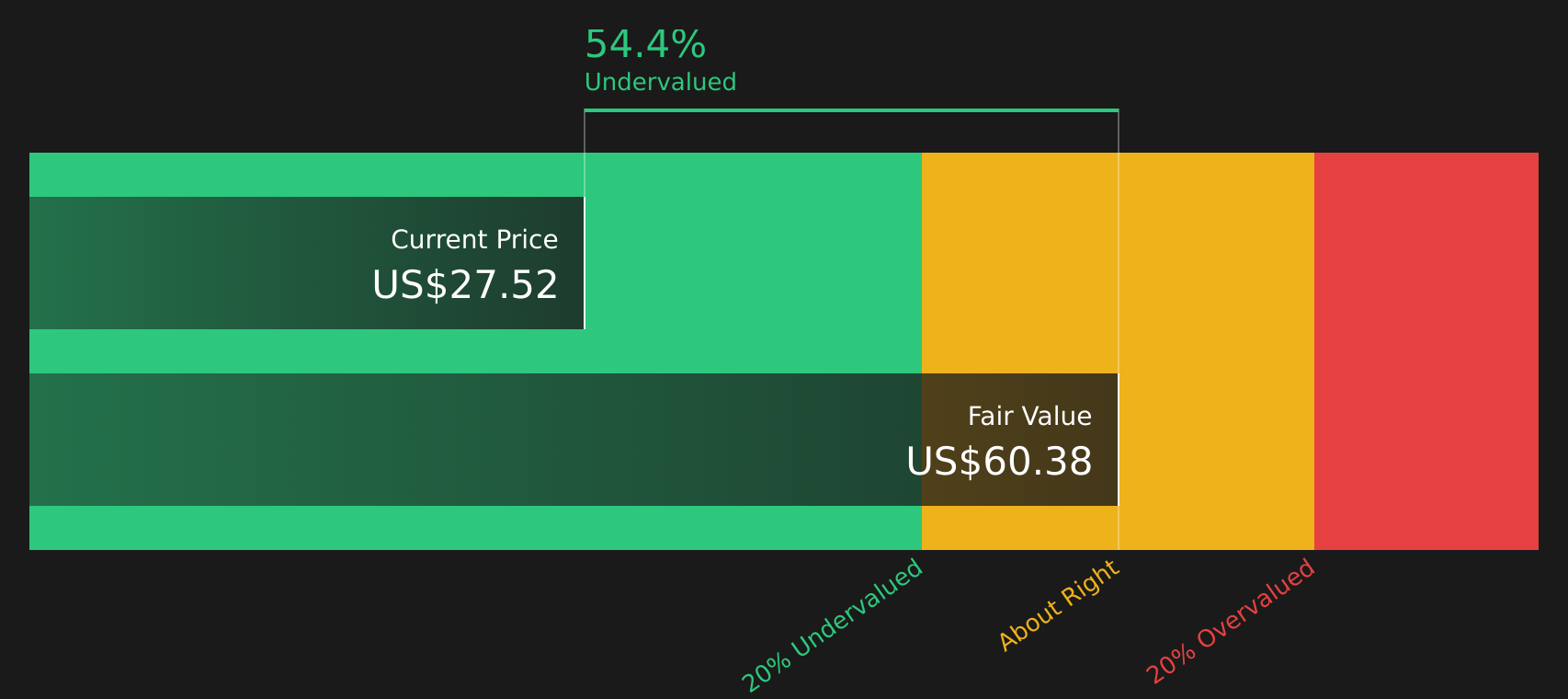

While the most followed narrative suggests Dropbox is slightly overvalued at $27.20 versus a fair value of $26.17, the SWS DCF model presents a different picture. It shows an estimated future cash flow value of $60.59, with the stock trading about 55.1% below that figure. Which story do you think is closer to reality?

Look into how the SWS DCF model arrives at its fair value.

Next Steps

With sentiment clearly split between opportunity and caution, it makes sense to move quickly, review the underlying data, and weigh both sides for yourself using the 3 key rewards and 2 important warning signs.

Looking for more investment ideas?

If Dropbox has you thinking differently about your portfolio, do not stop here. Use this moment to scan for other stocks that could sharpen your edge.

- Spot potential standouts trading below their estimated value by running your filters through the 47 high quality undervalued stocks.

- Anchor your portfolio with companies that pair income with resilience by checking out the 10 dividend fortresses.

- Hunt for lesser known opportunities with strong fundamentals by scanning the screener containing 22 high quality undiscovered gems.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com