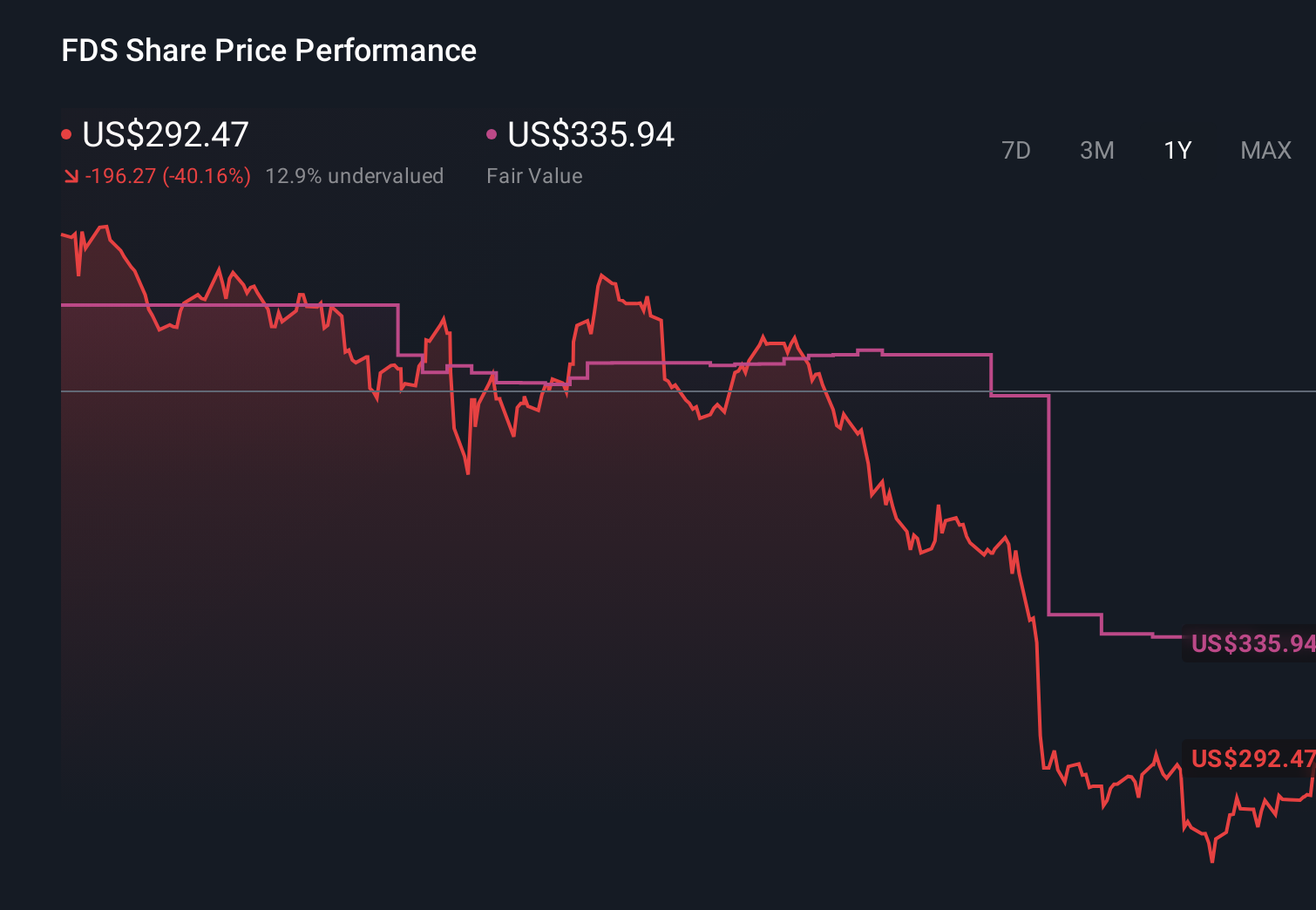

- In recent days, FactSet Research Systems has drawn attention as investors react to its upcoming fiscal third-quarter 2026 earnings release on 1 July and reassess the company’s positioning in the broader financial data sector.

- Amid this heightened focus, questions around perceived undervaluation, recent volatility and the lack of recent insider transactions have become central to how the market interprets FactSet’s outlook.

- We’ll now examine how this increased scrutiny around perceived undervaluation and upcoming earnings could influence FactSet’s existing investment narrative.

Find 49 companies with promising cash flow potential yet trading below their fair value.

FactSet Research Systems Investment Narrative Recap

To own FactSet, you generally need to believe in the resilience of its data and workflow platform, its AI product roll out, and its ability to keep expanding within asset management, banking and wealth despite sector belt tightening. Recent share price swings and claims of undervaluation do not materially alter the near term catalyst of the upcoming Q3 2026 earnings release, while the biggest risk remains pressure on growth and margins if client budgets stay constrained.

The most relevant recent announcement for this context is FactSet’s plan to report fiscal third quarter 2026 results on 1 July, alongside a live Q&A. That event will likely sharpen market focus on whether AI initiatives, new partnerships and cost discipline can offset headwinds from weaker pricing power, higher technology expenses and uneven international performance, all of which sit at the heart of today’s debate around the stock’s perceived mispricing.

Yet against this potential upside, investors should be aware of the risk that rising technology and cloud costs could...

Read the full narrative on FactSet Research Systems (it's free!)

FactSet Research Systems' narrative projects $2.8 billion revenue and $712.8 million earnings by 2029. This requires 5.5% yearly revenue growth and about a $125 million earnings increase from $587.8 million today.

Uncover how FactSet Research Systems' forecasts yield a $252.25 fair value, in line with its current price.

Exploring Other Perspectives

While the recent volatility raises fresh questions, some of the most optimistic analysts were previously assuming revenue of about US$2.8 billion and earnings near US$726.5 million by 2028, which is a far more upbeat story than the consensus view and shows just how much opinions can differ as new information like the latest price moves filters through.

Explore 6 other fair value estimates on FactSet Research Systems - why the stock might be worth just $252.25!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your FactSet Research Systems research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free FactSet Research Systems research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate FactSet Research Systems' overall financial health at a glance.

Interested In Other Possibilities?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Explore 30 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- We've uncovered the 9 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com