- On June 3, 2026, Alnylam Pharmaceuticals and Inceptive Nucleics announced a collaboration worth up to US$2.00 billion, including US$30 million upfront in cash and equity, to apply generative AI to accelerate RNAi drug discovery within Alnylam’s R&D engine.

- A distinctive aspect of the agreement is Alnylam’s access to Inceptive’s foundation models and AI talent, including Transformer co-inventor Jakob Uszkoreit, aiming to sharpen siRNA design and boost R&D productivity under the Alnylam 2030 plan.

- We’ll now examine how integrating frontier generative AI into Alnylam’s RNAi platform could reshape its investment narrative and long-term pipeline ambitions.

Rare earth metals are the new gold rush. Find out which 27 stocks are leading the charge.

Alnylam Pharmaceuticals Investment Narrative Recap

To own Alnylam, you need to believe its RNAi platform and TTR franchise can support a durable, profitable portfolio while it broadens beyond a few core drugs. The Inceptive Nucleics AI deal could influence how quickly Alnylam refreshes and diversifies its pipeline, but it does not directly change near term dependence on AMVUTTRA pricing, payer behavior, or TTR concentration risk.

Among recent events, the appointment of Benjamin Cravatt to the Board and Science and Technology Committee feels especially relevant here. His drug discovery background may matter as Alnylam tries to turn AI enabled siRNA design and a larger cardiovascular pipeline into concrete late stage assets, which many investors see as key to reducing single franchise risk and justifying premium multiples.

Yet while the AI collaboration may excite many shareholders, investors should also be aware of the risk that AMVUTTRA price pressure and payer pushback could...

Read the full narrative on Alnylam Pharmaceuticals (it's free!)

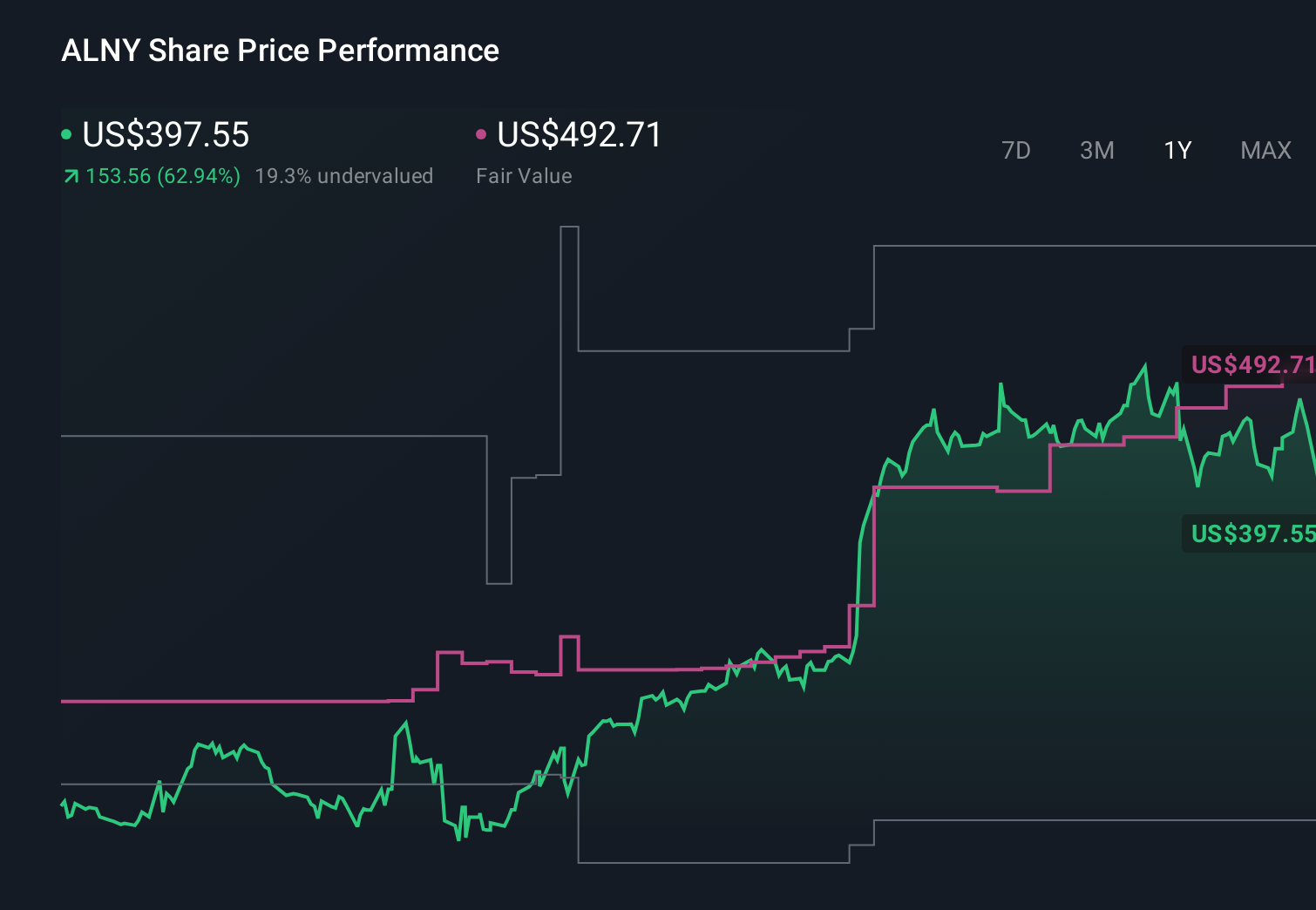

Alnylam Pharmaceuticals’ valuation narrative projects $7.0 billion in revenue and $1.9 billion in earnings by 2028.

Uncover how Alnylam Pharmaceuticals' forecasts yield a $491.92 fair value, a 62% upside to its current price.

Exploring Other Perspectives

Some of the lowest estimate analysts were already cautious, projecting about US$8.3 billion in 2029 revenue and US$1.3 billion in earnings, so if you read their view alongside the AI collaboration and Alnylam’s heavy TTR exposure, you see how sharply opinions can diverge and why it is worth comparing several narratives before deciding what you think could change.

Explore 5 other fair value estimates on Alnylam Pharmaceuticals - why the stock might be worth just $310.31!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Alnylam Pharmaceuticals research is our analysis highlighting 3 key rewards that could impact your investment decision.

- Our free Alnylam Pharmaceuticals research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Alnylam Pharmaceuticals' overall financial health at a glance.

Contemplating Other Strategies?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- We've uncovered the 9 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Outshine the giants: these 13 early-stage AI stocks could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com