- In late May 2026, Cheniere Energy Partners, L.P. awarded Bechtel a US$4.69 billion engineering, procurement and construction contract for Train 7 and related infrastructure at its Sabine Pass LNG expansion project in Louisiana.

- This new contract extends a long-standing collaboration between the two companies at Sabine Pass and signals a substantial multi-decade commitment to expanding US LNG export capacity.

- We’ll examine how this large Sabine Pass Train 7 contract shapes Cheniere Energy Partners’ investment narrative around growth, capital intensity and execution.

Uncover the next big thing with 24 elite penny stocks that balance risk and reward.

What Is Cheniere Energy Partners' Investment Narrative?

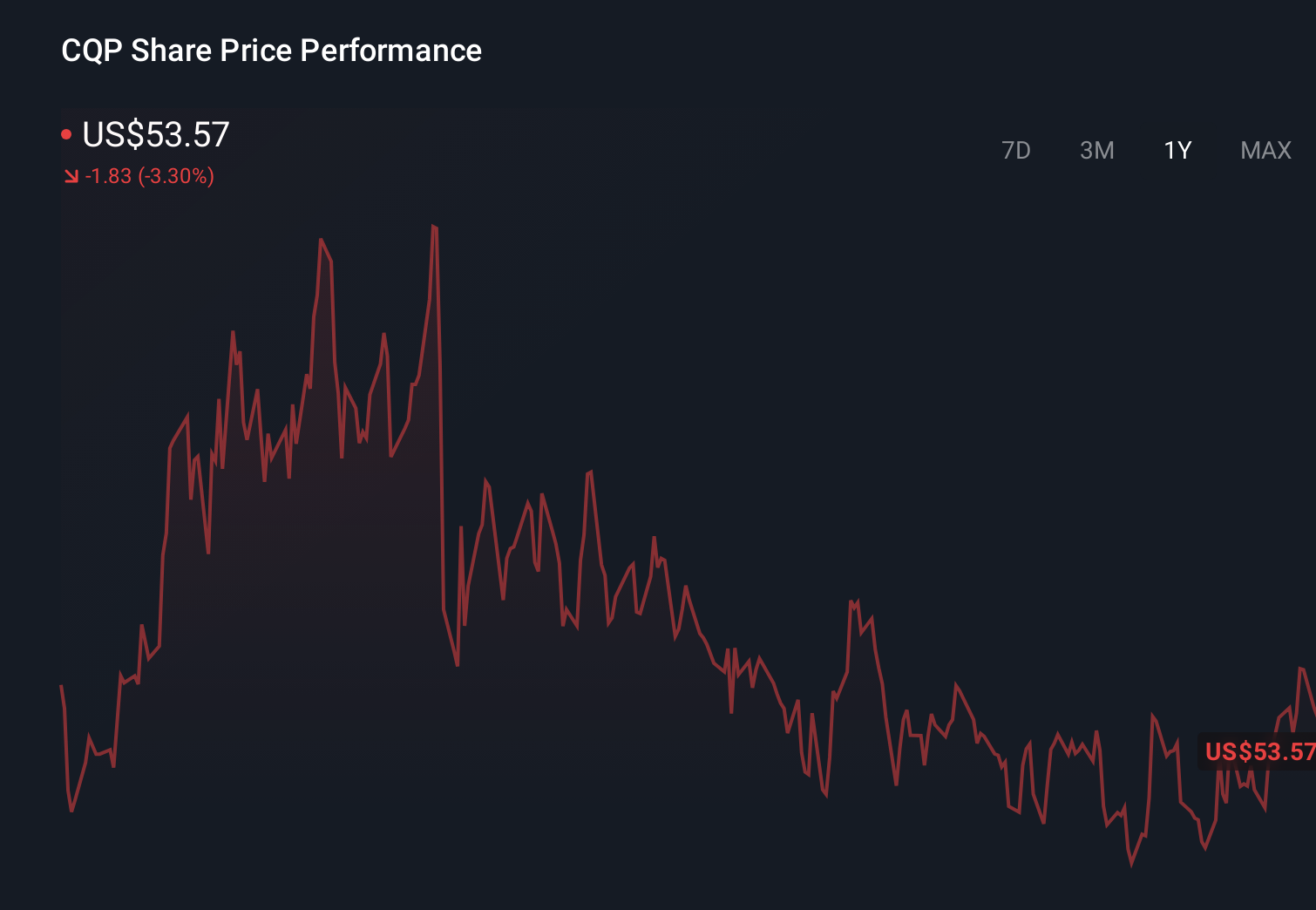

To own Cheniere Energy Partners today, you need to be comfortable with a capital‑heavy LNG story where debt-funded expansion and long-term contracts sit at the center. The new US$4.69 billion Bechtel EPC award for Sabine Pass Train 7, paired with fresh 2036 and 2056 senior notes, reinforces that narrative: management is leaning into bigger projects and longer-dated financing rather than pulling back. In the near term, the key catalysts remain execution at Sabine Pass, stability of cash flows to support the US$3.10–US$3.40 per‑unit distribution guidance, and how efficiently CQP refinances nearer‑term maturities like the SPL 2027 notes. At the same time, higher leverage and already softer net margins keep balance sheet risk front and center, and the recent share price strength suggests the market is starting to price that mix in.

However, rising leverage tied to Train 7 and long-dated notes is something investors should understand. Cheniere Energy Partners' shares are on the way up, but could they be overextended? Uncover how much higher they are than fair value.Exploring Other Perspectives

Explore 2 other fair value estimates on Cheniere Energy Partners - why the stock might be worth less than half the current price!

Decide For Yourself

Disagree with this assessment? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Cheniere Energy Partners research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Cheniere Energy Partners research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Cheniere Energy Partners' overall financial health at a glance.

No Opportunity In Cheniere Energy Partners?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- Invest in the nuclear renaissance through our list of 88 elite nuclear energy infrastructure plays powering the global AI revolution.

- We've uncovered the 9 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Outshine the giants: these 13 early-stage AI stocks could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com