Recent performance snapshot

Pursuit Attractions and Hospitality (PRSU) has quietly attracted attention after a solid share price run, with the stock up about 4% over the past month and roughly 19% in the past 3 months.

Over the past year, the stock has returned about 50%, while year to date it is up roughly 31%. That move now aligns with a market value of about US$1.2b and a recent close of US$43.92.

See our latest analysis for Pursuit Attractions and Hospitality.

Short term momentum looks a little softer, with the 7 day share price return down 2.31%, but the broader trend remains constructive given the 1 year total shareholder return of 50.36%.

If Pursuit’s move has you curious about where else capital is flowing in travel, leisure, and experiences, it could be worth scanning 20 top founder-led companies

With PRSU trading at US$43.92 and analysts pointing to a US$52.25 price target, the stock appears to trade at a discount on paper. The key question is whether this represents genuine value or whether the market is already accounting for future growth.

Most Popular Narrative: 15.9% Undervalued

Analysts following Pursuit Attractions and Hospitality see fair value at about $52.25 per share, compared with the recent $43.92 close. They build that view off detailed assumptions about growth, margins, and capital allocation.

Significant long-term pipeline of organic reinvestment ("Refresh and Build" projects) and disciplined acquisition strategy (with financial flexibility for larger and smaller deals) provides opportunities to scale, drive operational leverage, and enhance earnings reliability and growth over multiple years. The new $50 million share repurchase authorization, in context of management's belief that the stock is undervalued, provides a near-term capital return catalyst. This should contribute to higher EPS and signal confidence in the company's long-term value creation trajectory.

Want to see what kind of revenue profile, margin lift, and future earnings power analysts are building into that fair value story? The narrative walks through a detailed earnings ramp, a higher profitability base, and a future valuation multiple that together need to line up for $52.25 to make sense.

Result: Fair Value of $52.25 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, the story can change quickly if climate related disruptions hit key destinations, or if high capital spending fails to translate into the earnings analysts are modeling.

Find out about the key risks to this Pursuit Attractions and Hospitality narrative.

Another angle on valuation

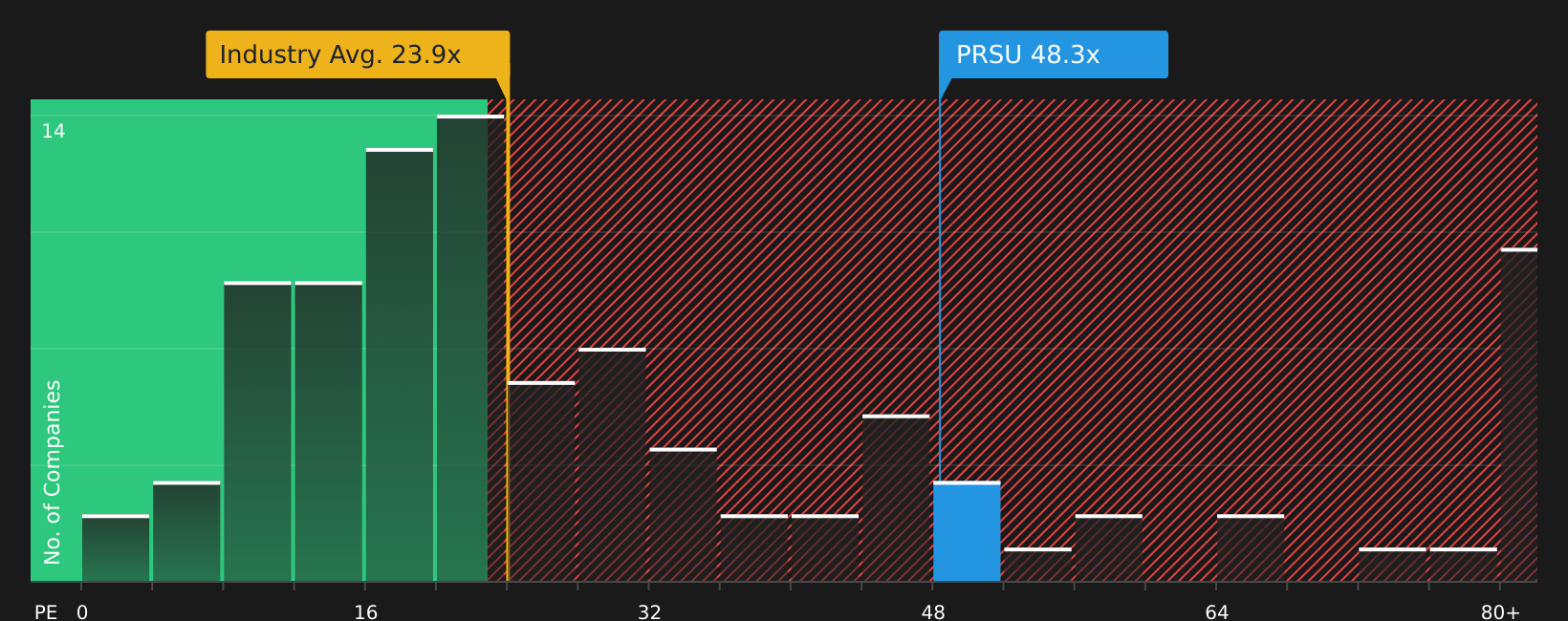

The analyst target frames PRSU as about 15.9% undervalued, but its P/E of 38.7x tells a tougher story. That is much higher than the 20.2x industry average, the 17.4x peer average, and even the 22.5x fair ratio the market could gravitate toward. This raises the question of how much execution risk is already priced in.

See what the numbers say about this price, find out in our valuation breakdown See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

The setup here includes both optimism and open questions. If it feels relevant, take a closer look at the details, form your own view, and then check the 2 key rewards.

Looking for more investment ideas?

If Pursuit has sharpened your focus, do not stop here. Broaden your watchlist now so you are not late to the next opportunity.

- Target potential bargains by scanning 48 high quality undervalued stocks that pair quality fundamentals with prices that may not fully reflect their underlying strength.

- Prioritise resilience by reviewing 63 resilient stocks with low risk scores that score well on financial health and business stability.

- Hunt for future standouts through screener containing 21 high quality undiscovered gems that sit off the usual radar yet show solid underlying metrics.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com