Carrier Global (CARR) has caught investor attention after reporting quarterly results that topped analyst expectations on revenue and adjusted EPS, while keeping its quarterly dividend intact despite ongoing pressure in the residential HVAC market.

See our latest analysis for Carrier Global.

At a share price of US$67.35, Carrier has posted a 15.27% 90 day share price return and a 25.84% year to date share price return. The 1 year total shareholder return is down 4.62% and the 3 year total shareholder return is 53.11%, suggesting momentum has picked up recently even though longer term holders have seen a mix of gains and setbacks.

If Carrier's focus on data center cooling has your attention, it could be a good time to widen your research and check out 48 AI infrastructure stocks

With Carrier trading at US$67.35 and sitting at roughly a 13% discount to the average analyst price target, along with an indicated intrinsic discount of about 32%, investors may question whether there is still a buying opportunity or if the market is already pricing in future growth.

Most Popular Narrative: 11.7% Undervalued

Carrier Global's most followed narrative pegs fair value at $76.31, above the last close of $67.35, which frames the recent price strength in a different light.

Carrier's strategic expansion into the data center cooling market, including the development of integrated quantum leap cooling systems, is presented as a factor that could influence future earnings by increasing market share and exposure to this sector.

The narrative points to steadily compounding revenue, widening margins, and a future earnings base that has bulls and bears taking very different views.

Result: Fair Value of $76.31 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, weaker trends in Climate Solutions Asia, Middle East and Africa, and the remaining US$300m tariff exposure could pressure margins and challenge the current undervaluation story.

Wall Street's queuing for one rocket. While SpaceX counts down to its IPO, other companies tied to the new space race are already in orbit. → 20 Compelling Space Companies watchlist · Global Space Race Investing Ideas screener · Scan the sector by valuation on Rocket Lab's valuation page.

Another View: Pricing Tension From Earnings Multiples

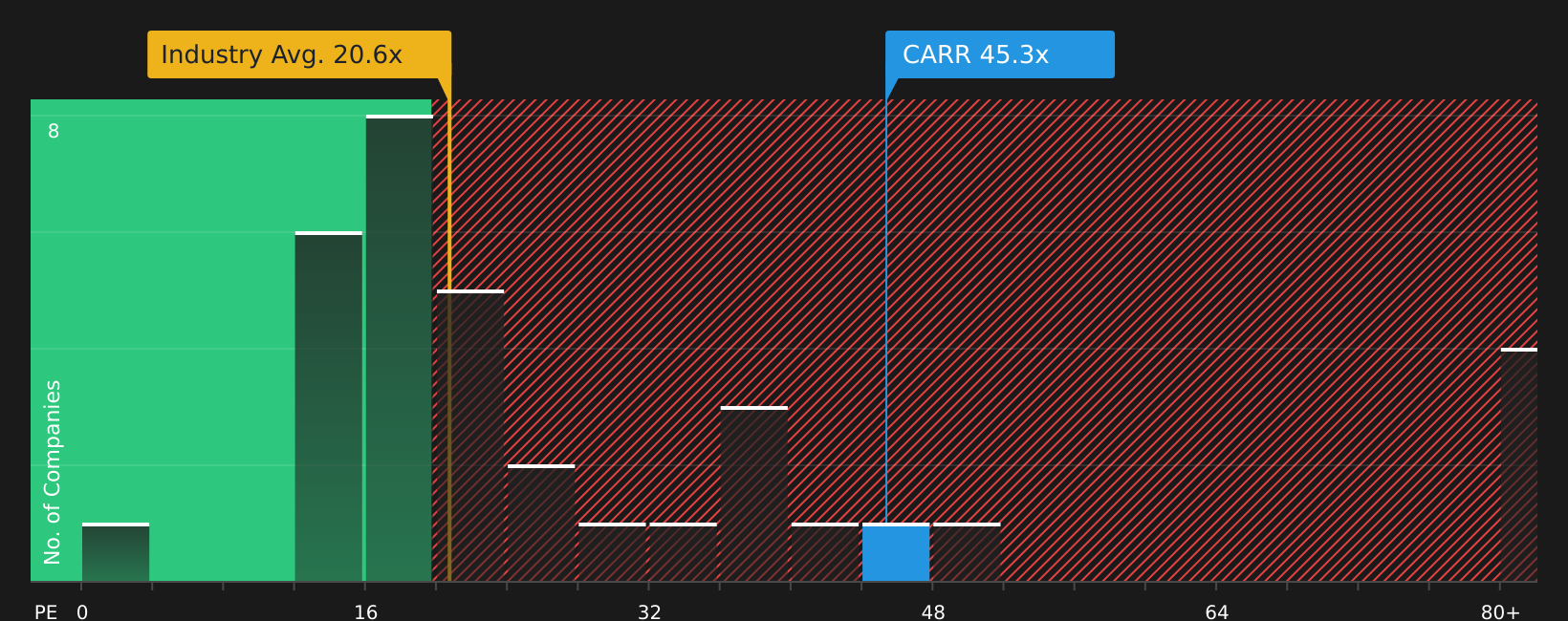

While the SWS DCF model suggests Carrier is trading about 31.7% below estimated fair value at $98.54, the current P/E of 43.6x tells a different story. That multiple sits above the fair ratio of 38.7x, the US Building industry on 20.3x, and peers at 29.7x. This points to meaningful valuation risk if expectations reset closer to those levels. Which signal do you trust more: the cash flow model or the earnings multiple?

See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

If this mix of risks and upside potential leaves you unsure, act while the data is fresh and shape your own view with the 2 key rewards and 1 important warning sign.

Looking for more investment ideas?

If Carrier has sharpened your focus, do not stop here. Broaden your watchlist now so you are not catching up after the next move.

- Spot potential value plays early by checking companies our tools flag as 47 high quality undervalued stocks.

- Strengthen your income stream by reviewing stocks in the 10 dividend fortresses.

- Dial down risk while staying invested by scanning the 62 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com