- In May 2026, The Gap, Inc. reported first‑quarter sales of US$3,497 million and net income of US$339 million, alongside completing a US$401 million buyback of 16,685,674 shares.

- The company also tightened full‑year guidance to more modest net sales growth while targeting diluted EPS of about US$2.83 to US$2.93, highlighting a focus on margin and cost discipline despite uneven brand performance.

- We’ll now examine how Gap’s raised full‑year earnings guidance, despite softer quarterly performance, affects the broader investment narrative for the company.

Uncover the next big thing with 23 elite penny stocks that balance risk and reward.

Gap Investment Narrative Recap

To own Gap today, you need to believe management can convert modest sales progress into stronger, more consistent earnings through tighter execution, even as individual brands remain uneven. The latest quarter did not resolve that brand dispersion, so the key short term catalyst is still margin improvement rather than top line growth, while the biggest risk remains flat overall sales if core concepts like Old Navy or Athleta stumble again. This news does not fundamentally change that balance.

The most relevant piece of recent news here is Gap’s raised full year diluted EPS guidance to about US$2.83 to US$2.93, even as expected net sales growth was trimmed to 1% to 2%. That shift reinforces the idea that cost control and operating discipline, rather than rapid revenue expansion, are doing most of the near term heavy lifting, which matters a lot if you are focused on earnings resilience over the next few quarters.

But against this improving margin story, investors should also be aware that...

Read the full narrative on Gap (it's free!)

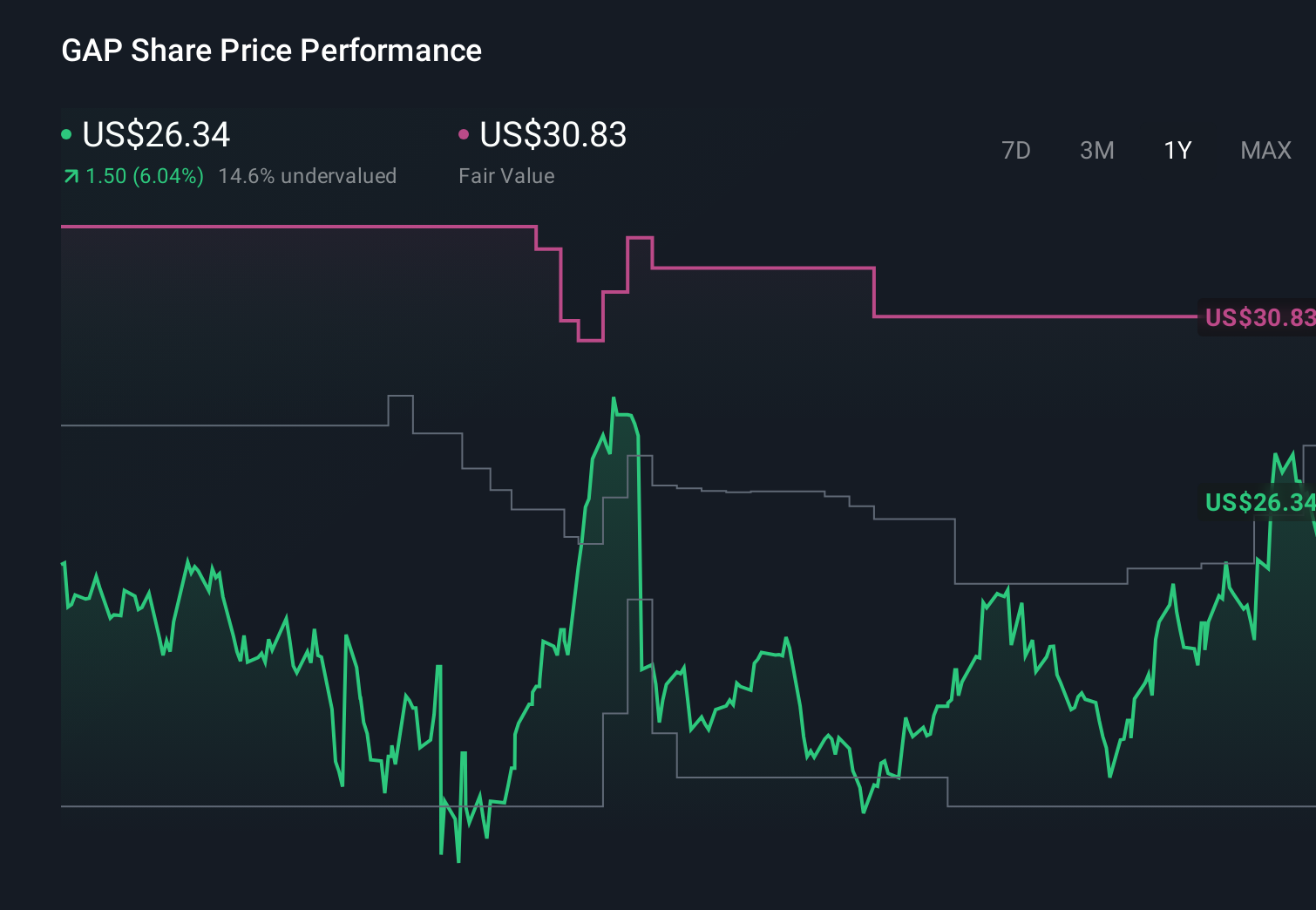

Gap's narrative projects $16.6 billion revenue and $1.0 billion earnings by 2029. This requires 2.7% yearly revenue growth and a $184.0 million earnings increase from $816.0 million today.

Uncover how Gap's forecasts yield a $30.65 fair value, a 44% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were already assuming Gap could reach around US$17.3 billion in revenue and US$1.1 billion in earnings, so this latest earnings beat and guidance tweak may either support or challenge those expectations depending on how you see the risk of persistent brand and inventory missteps evolving from here.

Explore 7 other fair value estimates on Gap - why the stock might be worth just $22.60!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Gap research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Gap research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Gap's overall financial health at a glance.

Contemplating Other Strategies?

Our top stock finds are flying under the radar-for now. Get in early:

- AI is about to change healthcare. These 39 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Invest in the nuclear renaissance through our list of 88 elite nuclear energy infrastructure plays powering the global AI revolution.

- Outshine the giants: these 13 early-stage AI stocks could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com