Iridium Communications (IRDM) drew fresh attention after Oppenheimer shifted its view to Outperform and raised its expectations for the stock, a supportive signal that arrived despite ongoing questions around valuation and insider share sales.

See our latest analysis for Iridium Communications.

That upgrade landed against a backdrop of strong recent momentum, with a 30 day share price return of 14.51% and a 90 day share price return of 91.20%. The 1 year total shareholder return of 70.84% contrasts with a weaker 3 year total shareholder return that declined 19.63%, suggesting sentiment has shifted more positively in the short term as investors reassess growth potential and risk.

If you are looking beyond Iridium and want to see what else is moving in connected technologies, now is a good time to scan 48 AI infrastructure stocks

So with Iridium trading at a premium to some valuation models yet still sitting on an implied intrinsic discount and fresh analyst optimism, should you view current levels as a potential entry point or as a market that has already priced in expectations for future performance?

Most Popular Narrative: 56.3% Overvalued

With Iridium closing at $47.48 against a narrative fair value of $30.38, the current price sits well above that widely followed estimate.

The analysts have a consensus price target of $30.38 for Iridium Communications based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $40.0, and the most bearish reporting a price target of just $16.0.

Want to see what kind of earnings path and margin profile could justify that valuation gap? The narrative leans on moderate growth, richer profitability, and a meaningfully higher future earnings multiple. Curious which specific assumptions pull the fair value down toward $30 rather than up to today’s price?

Result: Fair Value of $30.38 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, softer 2026 service revenue guidance and ongoing pressure from customers shifting to lower value plans could quickly challenge the upbeat, spectrum-driven narrative.

Wall Street's queuing for one rocket. While SpaceX counts down to its IPO, other companies tied to the new space race are already in orbit. → 20 Compelling Space Companies watchlist · Global Space Race Investing Ideas screener · Scan the sector by valuation on Rocket Lab's valuation page.

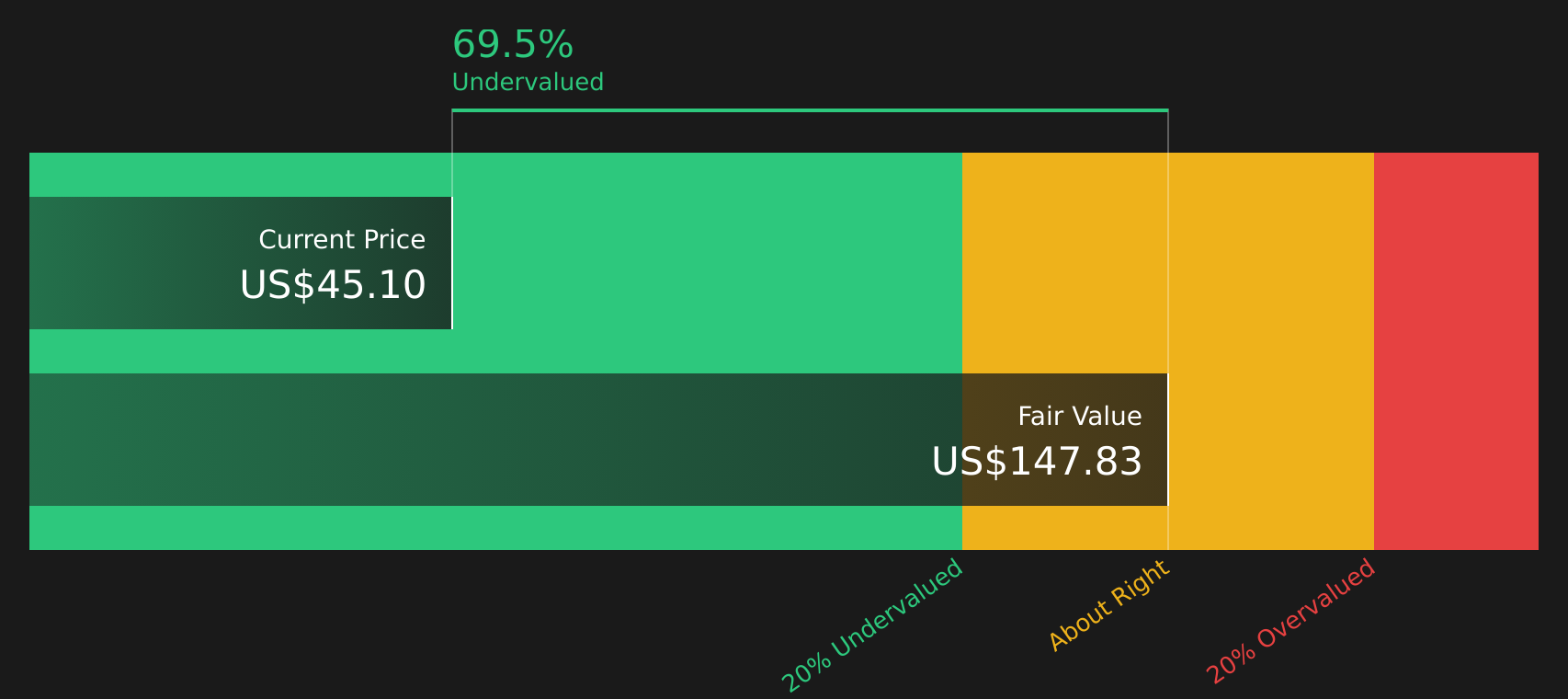

Another Take: Cash Flows Point the Other Way

While analysts see Iridium Communications as 56.3% overvalued with a fair value of $30.38, the SWS DCF model points in the opposite direction, suggesting the stock is trading at a 67.8% discount to its future cash flow value of $147.34. Which signal do you treat as more important, sentiment or cash flows?

To see how that cash flow view is built and where assumptions could be too cautious or too optimistic, take a closer look at the SWS DCF model output for Iridium Communications, including the full calculation path and key inputs: Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Iridium Communications for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 47 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

After weighing upbeat signals against clear concerns, do not sit on the fence; review the full picture and judge the trade off for yourself with the 2 key rewards and 1 important warning sign

Looking for more investment ideas?

If you stop with just one stock, you risk missing other opportunities that fit your goals, so put a few minutes into broadening your watchlist with focused screens.

- Spot potential mispricings by scanning 47 high quality undervalued stocks that combine solid fundamentals with room for a stronger future story.

- Strengthen your defense by reviewing 63 resilient stocks with low risk scores that carry lower overall risk scores while still offering meaningful business exposure.

- Get ahead of the crowd by checking the screener containing 21 high quality undiscovered gems before they land on every investor’s radar.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com