- NOV recently saw a sharp one-day pullback after a period of strong outperformance, as investors reassessed the balance between growth opportunities and rising cost headwinds.

- The tension between robust energy infrastructure demand and concerns about margin pressure from tariffs, inflation and higher capital spending now sits at the center of NOV’s story.

- We’ll now examine how this margin pressure concern, despite supportive energy infrastructure demand, may influence NOV’s broader investment narrative.

AI is about to change healthcare. These 39 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

NOV Investment Narrative Recap

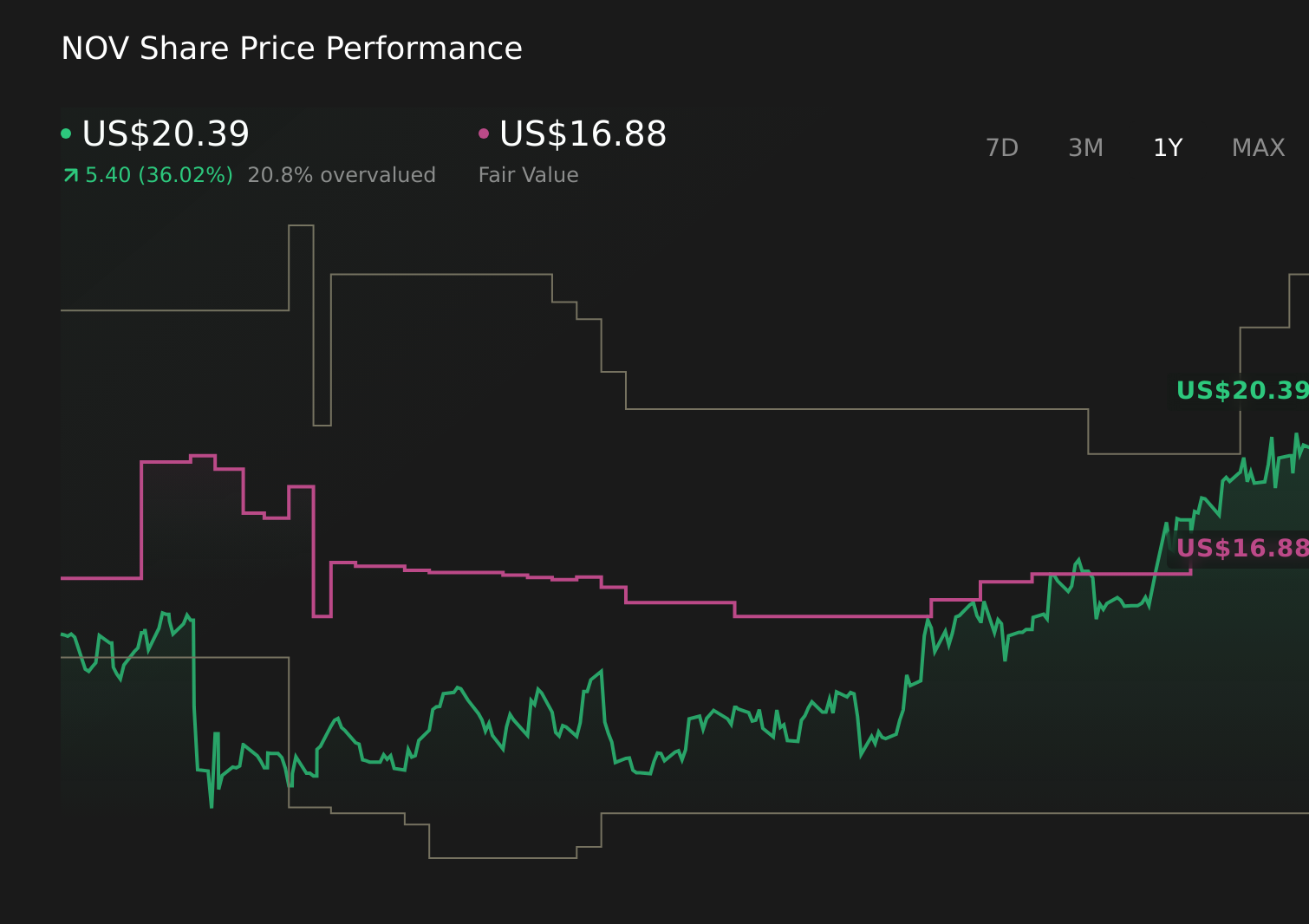

To own NOV today, you need to believe that its exposure to global energy infrastructure, including offshore and subsea, outweighs concerns about thin margins and volatile earnings. The recent pullback and softer Q1 results highlight that margin pressure from tariffs, inflation and higher capex is the key near term risk. In my view, the one day selloff does not fundamentally change the central catalyst, which remains how effectively NOV can convert its backlog and capacity investments into sustainably higher profitability.

The most relevant recent announcement here is NOV’s plan to roughly double subsea flexible pipe manufacturing capacity in Açu, Brazil, with a US$200 million investment over three years. This expansion ties directly into the margin debate: it supports the growth narrative around long cycle offshore demand, but it also raises near term capex and execution risk at a time when Q1 2026 revenue and net income already showed pressure on profitability.

Yet beneath this growth story, investors should also be aware of rising tariffs and cost inflation that could...

Read the full narrative on NOV (it's free!)

NOV's narrative projects $9.3 billion revenue and $492.5 million earnings by 2029.

Uncover how NOV's forecasts yield a $21.40 fair value, a 3% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were expecting earnings to climb toward about US$588 million by 2029, but compared with the tariff and cost inflation risks you have just seen, that is a far more optimistic story than the consensus and both views may need updating after this latest volatility.

Explore 4 other fair value estimates on NOV - why the stock might be worth as much as 40% more than the current price!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your NOV research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

- Our free NOV research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate NOV's overall financial health at a glance.

No Opportunity In NOV?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- Find 46 companies with promising cash flow potential yet trading below their fair value.

- The latest GPUs need a type of rare earth metal called Neodymium and there are only 27 companies in the world exploring or producing it. Find the list for free.

- This technology could replace computers: discover 30 stocks that are working to make quantum computing a reality.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com