- O-I Glass recently presented at the Wells Fargo 16th Annual Industrials & Materials Conference in Chicago, where its CEO and CFO reaffirmed 2026 adjusted EBITDA guidance of US$1.13–US$1.23 billion and EPS of US$1.00–US$1.50.

- Management also highlighted that the Fit To Win cost-saving program is running ahead of schedule, with US$50.00 million of gross benefits expected in 2026 despite softer demand and higher energy costs.

- We’ll now examine how reaffirmed guidance supported by ahead-of-schedule Fit To Win savings may influence O-I Glass’s existing investment narrative.

Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 27 best rare earth metal stocks of the very few that mine this essential strategic resource.

O-I Glass Investment Narrative Recap

To own O-I Glass, you need to believe that cost efficiency and resilient glass packaging demand can eventually offset recent losses and industry headwinds. The reaffirmed 2026 adjusted EBITDA and EPS guidance suggests that, in the near term, the key catalyst remains execution on Fit To Win savings, while the biggest risk is that softer volumes and higher energy costs keep eroding profitability. This conference update does not appear to materially change that risk‑reward balance.

Among recent developments, ongoing share repurchases under the US$100.0 million authorization stand out alongside the reiterated 2026 guidance. Buying back over 5.0 million shares since 2024 modestly amplifies any future earnings recovery per share, which ties directly into the catalyst of improving margins from Fit To Win. However, with the business still loss making, the effectiveness of these capital returns ultimately hinges on whether cost savings translate into durable, positive earnings.

But investors should also be aware that if energy inflation persists and volume softness deepens, O-I Glass’s reliance on cost cuts could...

Read the full narrative on O-I Glass (it's free!)

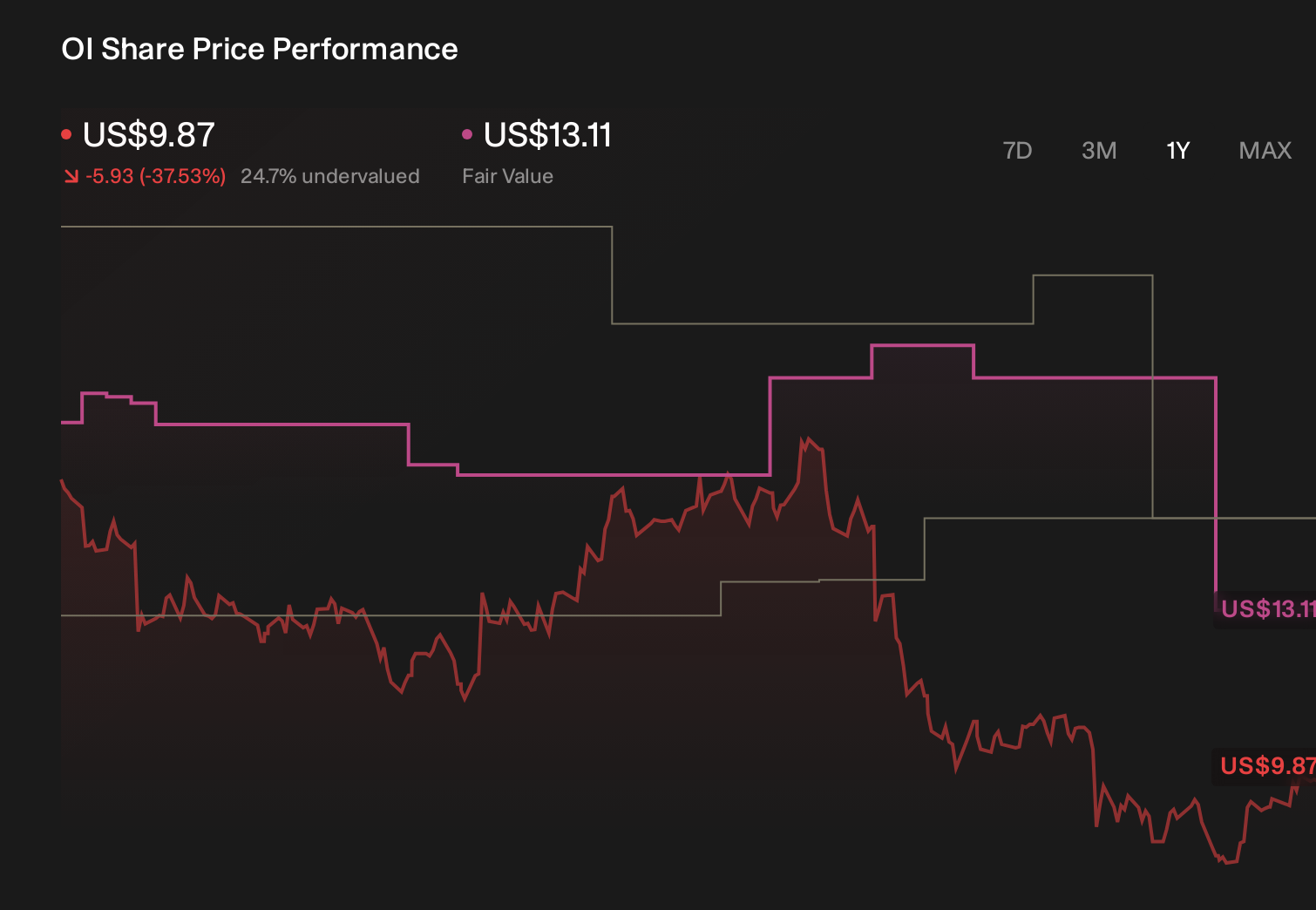

O-I Glass' narrative projects $6.8 billion revenue and $565.5 million earnings by 2029.

Uncover how O-I Glass' forecasts yield a $13.11 fair value, a 58% upside to its current price.

Exploring Other Perspectives

Before this update, the most optimistic analysts expected revenue near US$6.9 billion and earnings of about US$502 million by 2029, which is far more upbeat than the consensus view that focuses on modest growth and fragile margins. You may find that the bullish case, which leans heavily on Fit To Win and premiumization to overcome risks like energy costs and substitution, feels too optimistic or just right depending on your own assumptions, and this latest guidance reaffirmation could shift those narratives in either direction.

Explore 3 other fair value estimates on O-I Glass - why the stock might be worth just $13.11!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your O-I Glass research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free O-I Glass research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate O-I Glass' overall financial health at a glance.

Looking For Alternative Opportunities?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- Outshine the giants: these 14 early-stage AI stocks could fund your retirement.

- This technology could replace computers: discover 30 stocks that are working to make quantum computing a reality.

- We've uncovered the 9 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com