Over the last 7 days, the United States market has experienced a 3.3% decline, yet it remains up by 22% over the past year with earnings anticipated to grow by 17% annually in the coming years. In this context, growth companies with substantial insider ownership can be particularly appealing as they often indicate strong confidence from those closest to the business's operations and potential.

Top 10 Growth Companies With High Insider Ownership In The United States

| Name | Insider Ownership | Earnings Growth |

| Uxin (UXIN) | 34.3% | 74.1% |

| Upstart Holdings (UPST) | 14.1% | 58.9% |

| SharonAI Holdings (SHAZ) | 32.5% | 105.4% |

| Karman Holdings (KRMN) | 15.6% | 52.6% |

| FirstSun Capital Bancorp (FSUN) | 21% | 54.2% |

| Duos Technologies Group (DUOT) | 11.2% | 158.4% |

| Corcept Therapeutics (CORT) | 10.9% | 48.9% |

| Astera Labs (ALAB) | 10.1% | 29.3% |

| AppLovin (APP) | 27.5% | 21.7% |

| Abeona Therapeutics (ABEO) | 16.7% | 32.9% |

Here's a peek at a few of the choices from the screener.

Aebi Schmidt Holding (AEBI)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Aebi Schmidt Holding AG manufactures specialty vehicles across North America, Europe, and internationally, with a market cap of $925.42 million.

Operations: The company's revenue is primarily derived from North America, contributing $1.17 billion, and Europe and the rest of the world, generating $567.85 million.

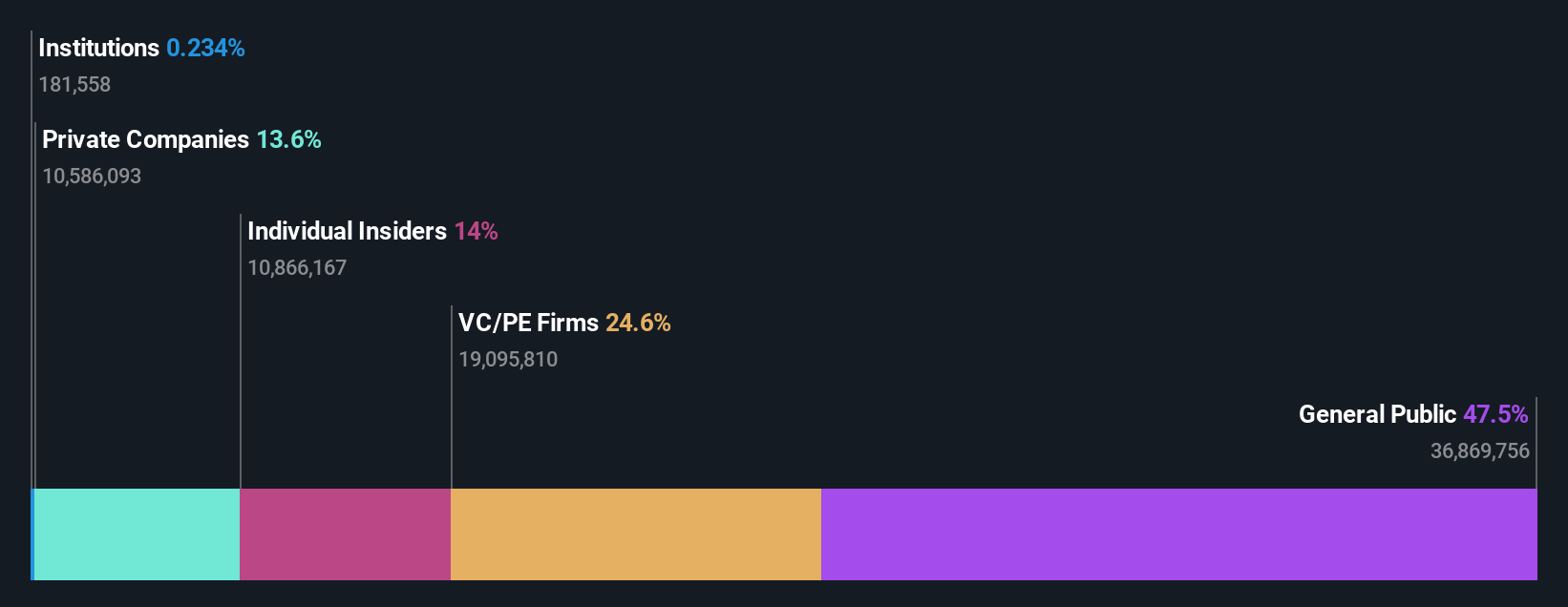

Insider Ownership: 14.3%

Earnings Growth Forecast: 97.3% p.a.

Aebi Schmidt Holding has demonstrated strong growth potential with a 61% revenue increase last year and forecasts predicting earnings growth of 97.32% annually, outpacing the US market. Insider confidence is evident, with significant insider buying and no substantial selling in the past three months. Recent leadership changes include Barend Fruithof as Chair of the Board, while strategic amendments to company bylaws aim to enhance governance flexibility. Despite these positives, profit margins have decreased compared to last year.

- Click here to discover the nuances of Aebi Schmidt Holding with our detailed analytical future growth report.

- Our valuation report unveils the possibility Aebi Schmidt Holding's shares may be trading at a premium.

EquipmentShare.com (EQPT)

Simply Wall St Growth Rating: ★★★★★☆

Overview: EquipmentShare.com Inc. offers integrated construction solutions through equipment rental, sales, and technology services, with a market cap of $5.04 billion.

Operations: The company's revenue is derived from equipment sales amounting to $1.58 billion and equipment rental and service operations totaling $2.93 billion.

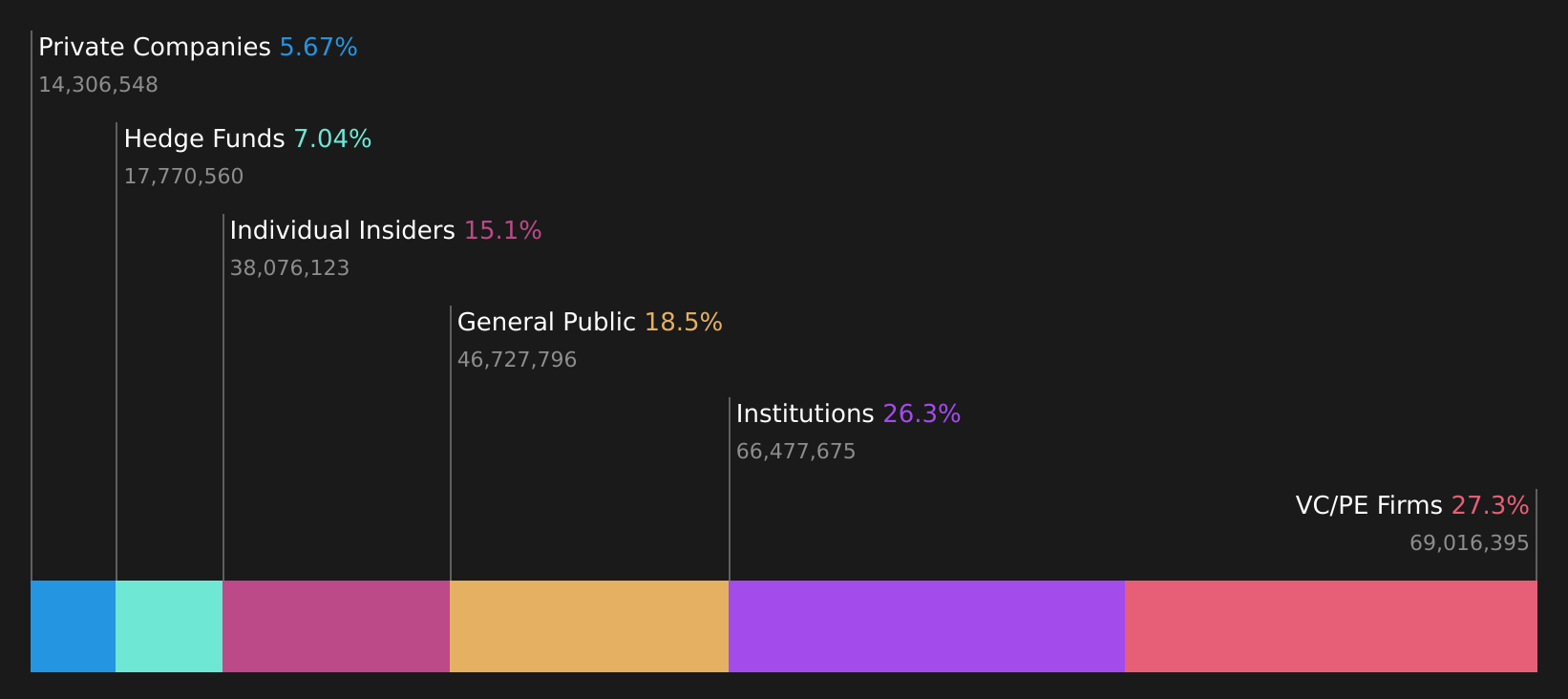

Insider Ownership: 15.1%

Earnings Growth Forecast: 46.3% p.a.

EquipmentShare.com has shown substantial insider buying with no significant selling in the past three months, indicating strong internal confidence. The company recently became profitable and forecasts suggest earnings growth of 46.3% per year, surpassing the US market average. Despite interest payments not being well covered by earnings, EquipmentShare raised its revenue guidance for 2026 to between US$5.15 billion and US$5.58 billion, reflecting optimism about future performance amidst slower revenue growth forecasts of 18.1% annually compared to peers.

- Get an in-depth perspective on EquipmentShare.com's performance by reading our analyst estimates report here.

- Insights from our recent valuation report point to the potential overvaluation of EquipmentShare.com shares in the market.

Estée Lauder Companies (EL)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: The Estée Lauder Companies Inc. manufactures, markets, and sells skin care, makeup, fragrance, and hair care products globally with a market cap of approximately $30.62 billion.

Operations: The company's revenue segments are comprised of $7.19 billion from skin care, $4.25 billion from makeup, $2.72 billion from fragrance, and $566 million from hair care products.

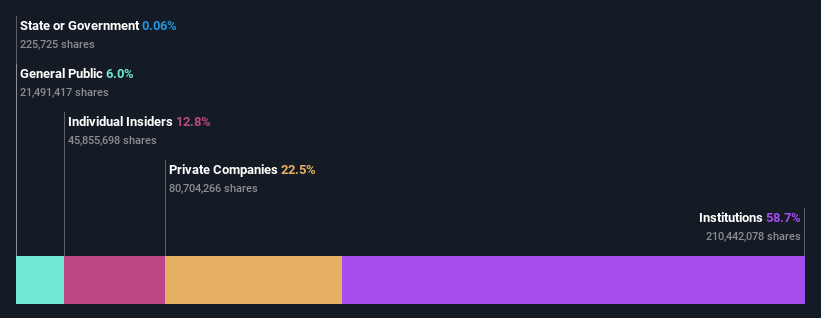

Insider Ownership: 11.3%

Earnings Growth Forecast: 50.5% p.a.

Estée Lauder Companies, with significant insider ownership, is forecast to achieve profitability within three years, surpassing market averages. Despite slower revenue growth projections of 3.8% annually compared to the US market's 11.9%, its return on equity is expected to be robust at 35.6%. Recent termination of merger talks with Puig led to an 11.5% share price increase as investors favored Estée Lauder's independent brand strength and family control stability amidst legal settlements and revised earnings guidance.

- Navigate through the intricacies of Estée Lauder Companies with our comprehensive analyst estimates report here.

- The analysis detailed in our Estée Lauder Companies valuation report hints at an deflated share price compared to its estimated value.

Turning Ideas Into Actions

- Navigate through the entire inventory of 175 Fast Growing US Companies With High Insider Ownership here.

- Curious About Other Options? We've found 9 US stocks that are forecast to pay a dividend yeild of over 6% next year. See the full list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com