- In early June 2026, Air Products and Chemicals marked the completion of a US$70 million expansion of its Missouri Manufacturing and Logistics Center in Maryland Heights, adding more than 70 hires to support rising demand in biogas, hydrogen recovery, aerospace nitrogen, and cleaner marine fuels.

- This expansion is Air Products Membrane Solutions' largest single-site investment to date, underlining how energy transition applications are becoming a central focus of the company’s industrial gas footprint.

- We’ll now examine how this major Missouri expansion, tied to rising biogas and hydrogen recovery demand, influences Air Products’ investment narrative.

The future of work is here. Discover the 34 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

Air Products and Chemicals Investment Narrative Recap

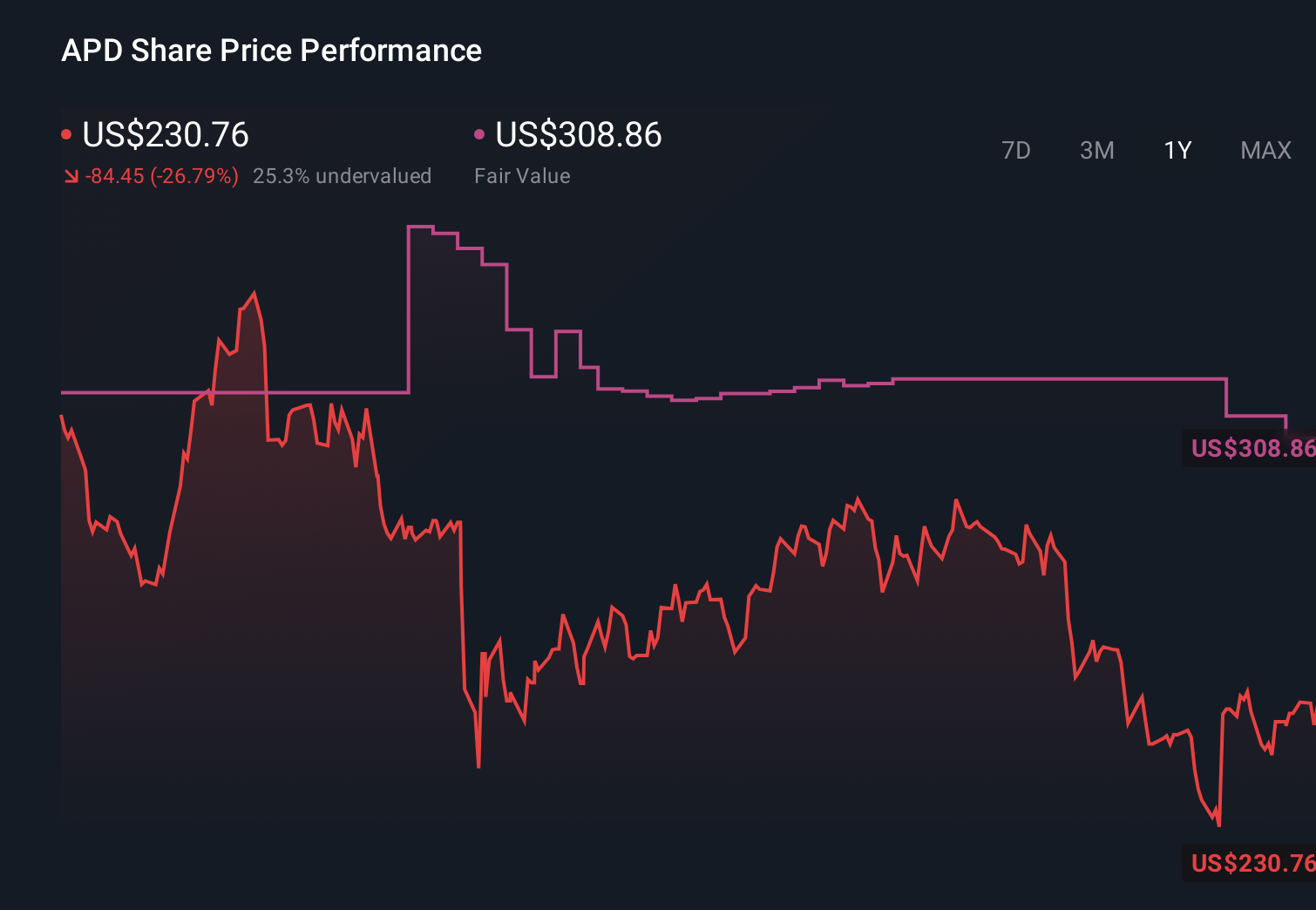

To own Air Products and Chemicals, you need to believe its large industrial gas and energy transition projects can translate into durable earnings and dividend growth despite heavy capital needs and project execution risk. The Missouri expansion supports that thesis at the margin by adding membrane capacity for biogas and hydrogen recovery, but it does not change that the key near term catalyst remains bringing major capital projects online efficiently, while the biggest risk is still delays or cost overruns that weigh on cash flow and returns.

The most relevant recent announcement alongside the Missouri news is Air Products’ April 2026 guidance raise, with the company pointing to pricing, productivity, and new asset contributions as drivers of expected earnings improvement this year. Together, stronger guidance and the new Missouri capacity frame a near term story that leans on operational execution and disciplined ramp up of new assets to justify the ongoing investment cycle and support the current dividend profile.

Yet while these developments look encouraging, investors should still watch how heavy capital spending could limit financial flexibility if...

Read the full narrative on Air Products and Chemicals (it's free!)

Air Products and Chemicals' narrative projects $15.4 billion revenue and $3.7 billion earnings by 2029. This requires 7.3% yearly revenue growth and a $1.6 billion earnings increase from $2.1 billion today.

Uncover how Air Products and Chemicals' forecasts yield a $327.86 fair value, a 19% upside to its current price.

Exploring Other Perspectives

Three members of the Simply Wall St Community value Air Products between US$214.95 and US$327.86 per share, showing a wide span of expectations. When you set those views against the company’s rising but capital intensive growth pipeline, it underlines how differently investors can weigh execution risk and why it helps to compare several independent assessments.

Explore 3 other fair value estimates on Air Products and Chemicals - why the stock might be worth as much as 19% more than the current price!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Air Products and Chemicals research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Air Products and Chemicals research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Air Products and Chemicals' overall financial health at a glance.

Want Some Alternatives?

Our top stock finds are flying under the radar-for now. Get in early:

- Uncover the next big thing with 25 elite penny stocks that balance risk and reward.

- Outshine the giants: these 14 early-stage AI stocks could fund your retirement.

- Capitalize on the AI infrastructure supercycle with our selection of the 48 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com