Moody's stock snapshot after recent performance shifts

Moody's (MCO) has drawn investor attention after recent share price moves. The stock is down 2% over the past week and about 2% over the past month, while the past 3 months show a 3% gain.

See our latest analysis for Moody's.

The recent pullback fits into a mixed picture, with the share price roughly flat over the past quarter but down year to date, while multi year total shareholder returns remain clearly positive.

If this kind of move has you scanning for other opportunities, it could be a good moment to widen your research using the 20 top founder-led companies

With Moody's stock down about 11% year to date but multi year returns still clearly positive, are you looking at a rare chance to buy quality at a discount, or are markets already pricing in its future growth?

Most Popular Narrative: 6.7% Undervalued

Moody's last closed at $441.82, while the most followed narrative, according to prajeesh, places fair value at $473.36, suggesting the market may be underappreciating the business.

Moody’s is not just a credit rating agency, it is one of the foundational infrastructure providers of the global financial system. Every year, governments, corporations, banks, and structured finance issuers collectively raise trillions of dollars in debt, and most of that debt requires a Moody’s rating to access institutional capital markets. This creates one of the strongest regulatory moats in modern capitalism. Alongside S&P Global, Moody’s effectively operates inside a global duopoly protected by decades of regulatory integration, reputation, and investor trust.

Want to understand why this narrative still sees upside at a premium price tag? The fair value hinges on sturdy margins, steady growth assumptions, and a powerful earnings multiple story that is not obvious from the chart alone.

Result: Fair Value of $473.36 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, the story can change if regulation reduces reliance on Moody's ratings or if a sharp, prolonged slump in global debt issuance pressures its high-margin model.

Find out about the key risks to this Moody's narrative.

Another view on what the price is saying

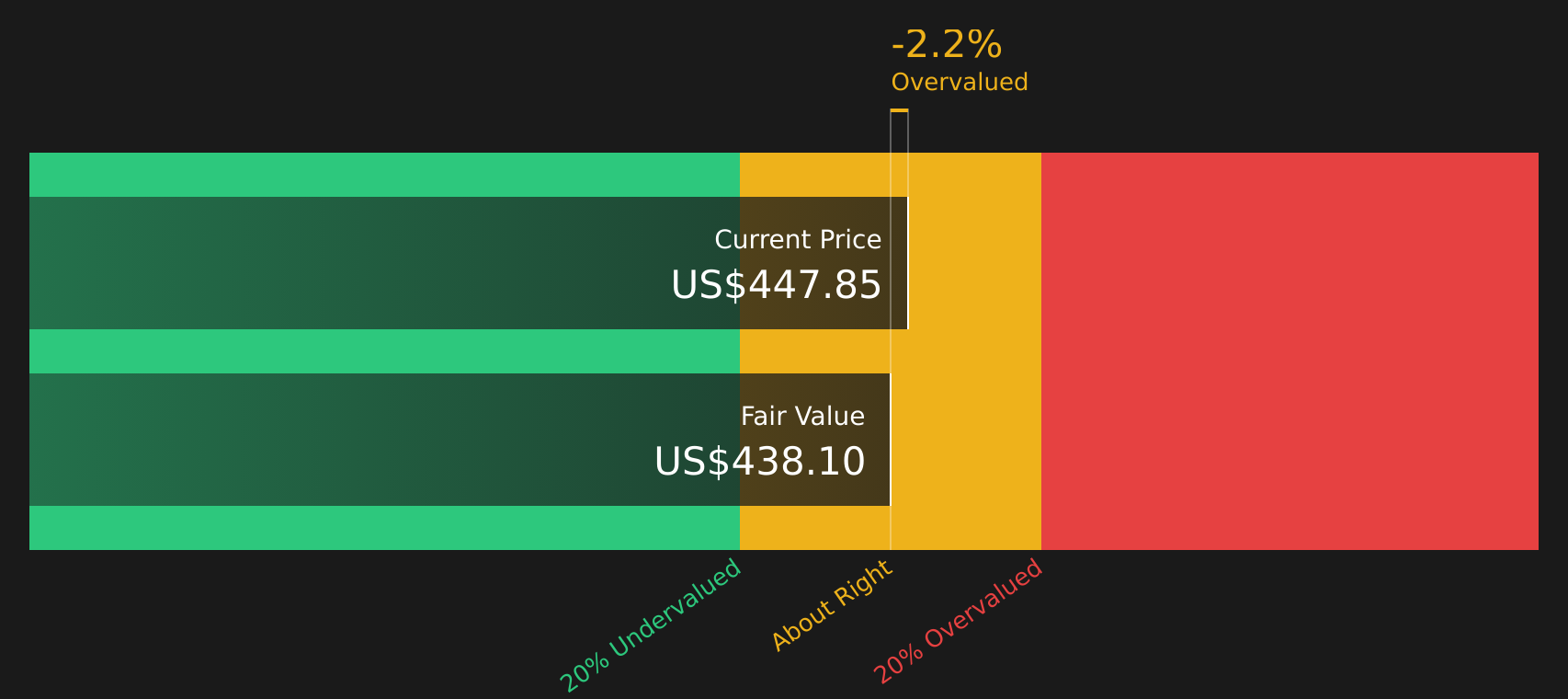

That user narrative sees Moody's as 6.7% undervalued at $473.36, but the SWS DCF model comes out slightly differently. On that view, the stock at $441.82 is trading just above an estimated future cash flow value of $440.71, which points to a price very close to fair rather than clearly cheap or expensive.

For a closer look at how this cash flow view is built and what would need to change for a bigger gap to open up, Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Moody's for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 47 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

Given the mix of cautious and optimistic signals so far, this is a good moment to look at the underlying data yourself and move quickly to shape your own view by weighing the 4 key rewards and 1 important warning sign.

Looking for more investment ideas?

If you stop with just one stock, you risk missing out on other strong setups, so use the Simply Wall St Screener to pressure test fresh ideas.

- Spot potential high return outliers early by scanning the 24 elite penny stocks with strong financials that already show stronger financial quality than many expect from this corner of the market.

- Hunt for quality at sensible prices by sorting through the 47 high quality undervalued stocks that pair solid fundamentals with valuations that may not fully reflect their strengths.

- Prioritise resilience by checking the 67 resilient stocks with low risk scores that score well on financial health so short term volatility is less likely to knock your plans off track.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com