- Unity Software recently moved to streamline its operations by winding down the ironSource Ads Network and selling its Supersonic game publishing unit, while concentrating resources on its Vector advertising network and Grow segment, which management reports are expanding quickly.

- This sharper focus on Vector as Unity’s core advertising engine highlights the company’s bid to become a more credible alternative in digital advertising, leveraging AI-driven capabilities across its gaming and interactive content platform.

- Next, we’ll examine how Unity’s renewed emphasis on the Vector ad network could reshape its existing investment narrative and future assumptions.

Uncover the next big thing with 24 elite penny stocks that balance risk and reward.

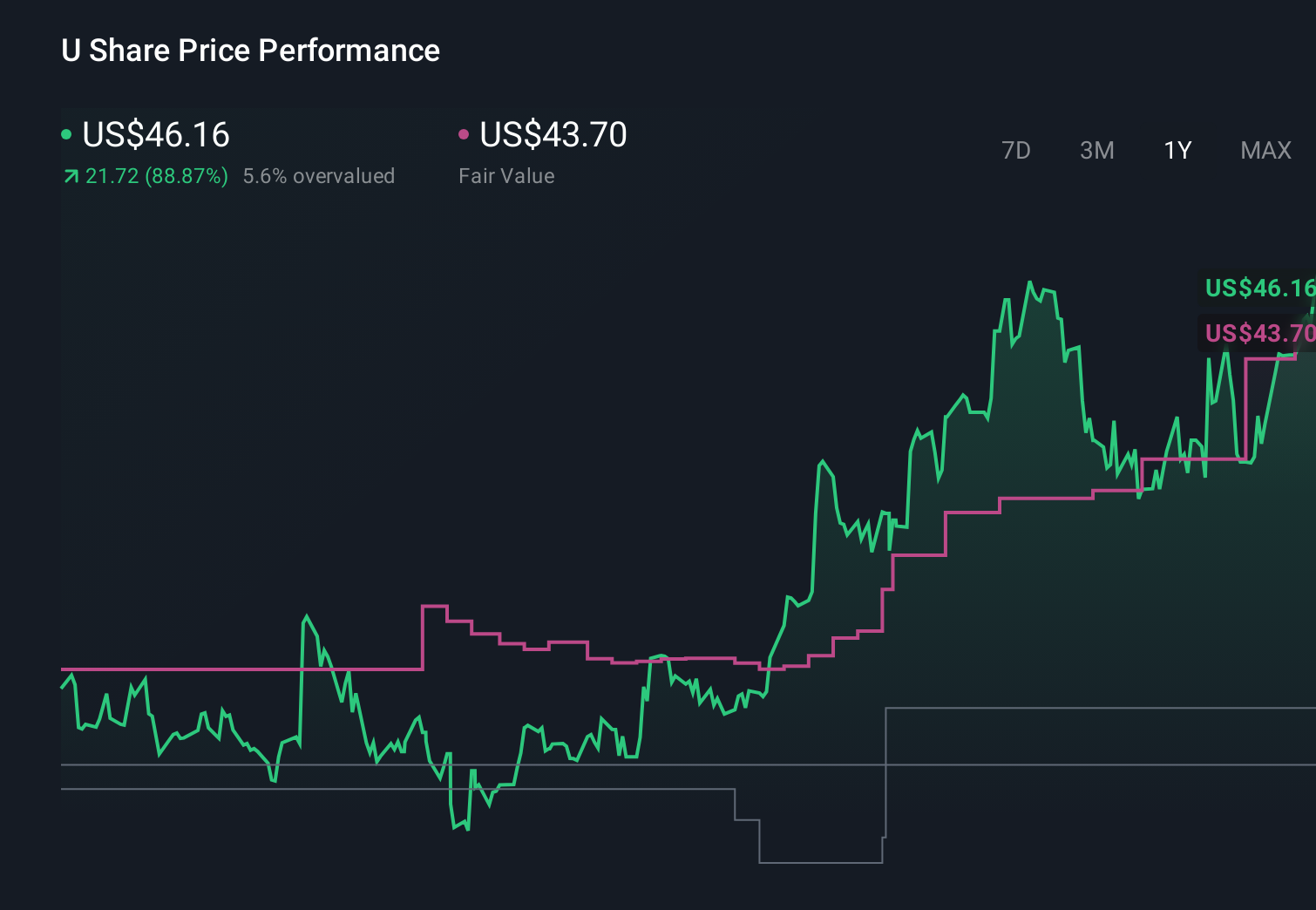

Unity Software Investment Narrative Recap

To own Unity today, you need to believe its engine, tools, and ad stack can translate a broad creator base into profitable, recurring software and advertising revenue. The recent shift toward the Vector ad network directly affects the key near term catalyst: stabilizing and growing the higher margin Grow segment without further worsening losses. The biggest risk remains execution, as Unity is still unprofitable and must prove it can simplify operations without sacrificing revenue scale.

The March decision to wind down the ironSource Ads Network and sell Supersonic is especially relevant here, because it clears the way for Vector and the Grow segment to carry more of the load. With Q1 2026 revenue at US$508.24 million but a net loss of US$347.61 million, any improvement in Unity’s ad efficiency and focus could matter for margins, even if the financial impact of these exits will take time to show up clearly.

Yet against this sharper focus on Vector, investors should also weigh the risk that rising competition and changing mediation trends in mobile advertising could...

Read the full narrative on Unity Software (it's free!)

Unity Software's narrative projects $2.9 billion revenue and $711.1 million earnings by 2029.

Uncover how Unity Software's forecasts yield a $34.39 fair value, a 26% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were already modeling Unity at about US$3.1 billion of revenue and US$334.6 million of earnings by 2029, which is far more bullish than the baseline view, and this latest Vector focused reshuffle might either reinforce that upside story or highlight how uncertain those assumptions really are.

Explore 7 other fair value estimates on Unity Software - why the stock might be worth as much as 98% more than the current price!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Unity Software research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Unity Software research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Unity Software's overall financial health at a glance.

Ready For A Different Approach?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- The latest GPUs need a type of rare earth metal called Dysprosium and there are only 29 companies in the world exploring or producing it. Find the list for free.

- The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Capitalize on the AI infrastructure supercycle with our selection of the 48 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com