Event: Stericycle Deal and New COO Put Healthcare and Sustainability in Focus

Waste Management (WM) has moved deeper into healthcare waste and sustainability by acquiring Stericycle and naming Tara Hemmer as chief operating officer. This combination sharpens attention on the stock’s evolving business mix and margin profile.

See our latest analysis for Waste Management.

WM’s recent news sits against a mixed share performance, with the stock falling 7.39% on a 90 day share price return and a 1 year total shareholder return down 5.72%. However, 3 and 5 year total shareholder returns of 39.23% and 73.12% point to momentum built over a longer holding period.

If this shift toward healthcare and infrastructure has your attention, it could be a good moment to scan other essential service plays through the 34 power grid technology and infrastructure stocks

With Waste Management trading at US$219.45, modest implied discounts to both analyst targets and some intrinsic estimates suggest a potential value gap. Investors may now be asking whether this recent pullback is an opportunity or whether the market is already pricing in future growth.

Most Popular Narrative: 13.3% Undervalued

Against a last close of $219.45, the most followed narrative points to a fair value of $253.12, framing WM as modestly undervalued on long term assumptions.

The company's strategic investments in sustainability, particularly in the areas of recycling and renewable energy, are showing strong, high-return growth, which could drive future revenue increases. The integration and optimization of WM Healthcare Solutions are on track to deliver significant synergies, anticipated to reach $250 million annually by 2027, positively impacting earnings.

Curious what sits behind that valuation gap? The narrative leans on steady top line growth, firmer margins, and a richer earnings multiple than the sector. The real intrigue is how those three levers combine in the model.

Result: Fair Value of $253.12 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this hinges on execution. Higher leverage after the Stericycle deal and potential shifts in tax credits and regulation are both capable of upsetting the current valuation story.

Find out about the key risks to this Waste Management narrative.

Another Angle: Earnings Multiple Sends a Caution Signal

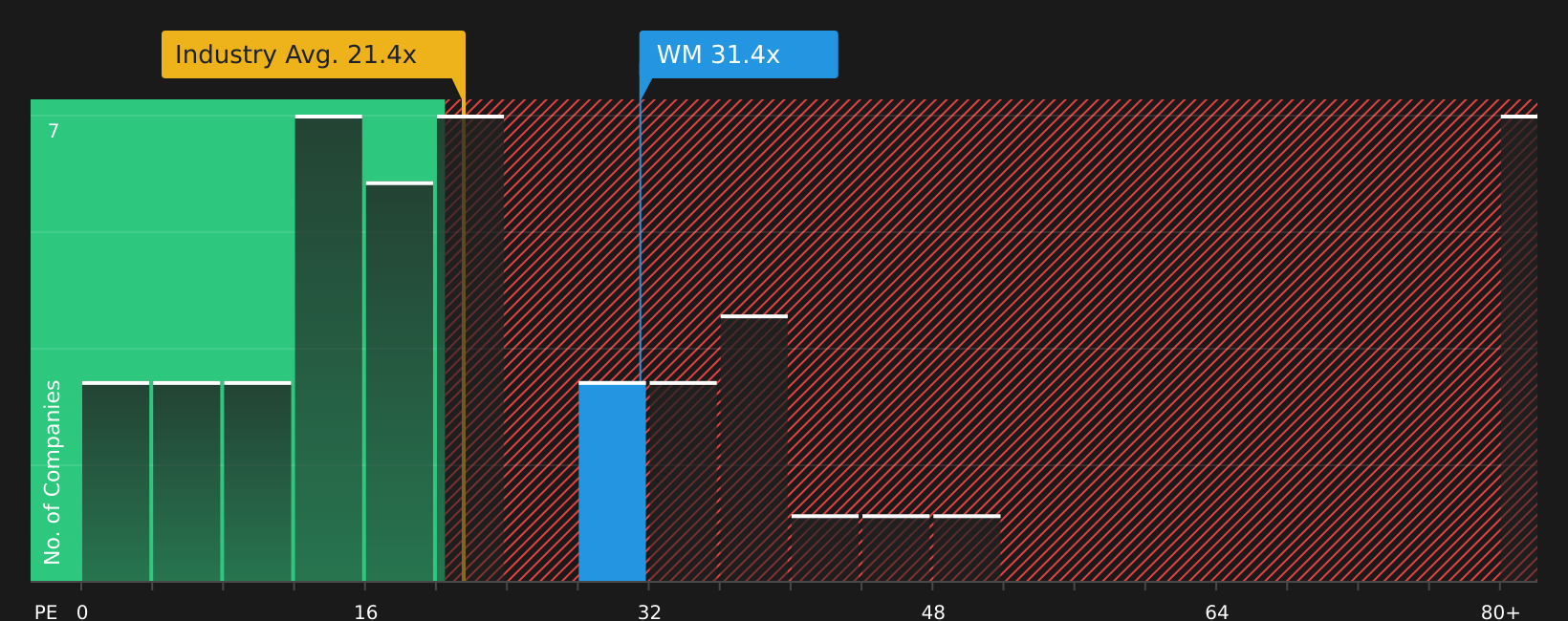

That 13.3% DCF style undervaluation sits next to a very different message from the P/E ratio. WM trades on 31.5x earnings versus a fair ratio of 25.9x, above the US Commercial Services average of 21.2x yet slightly below the peer average of 32.9x. This raises the question of whether the downside risk is being underplayed.

See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

With the mix of risks and rewards around WM, it makes sense to move quickly, check the underlying data, and stress test your own view using the 4 key rewards and 1 important warning sign.

Looking for more investment ideas?

If WM has sharpened your focus, do not stop here. Broaden your watchlist with other stocks that match different goals and risk levels.

- Target potential mispricings by checking companies that screen well on quality and value through the 44 high quality undervalued stocks.

- Strengthen your income stream by scanning for companies with higher yields and resilient payouts in the 8 dividend fortresses.

- Dial down risk by filtering for companies with healthier finances and steadier metrics using the solid balance sheet and fundamentals stocks screener (48 results).

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com