- In early June 2026, VinFast Auto reported preliminary May deliveries of 19,503 EVs in Vietnam, bringing year‑to‑date domestic deliveries to 97,961 vehicles and reinforcing its position in the local automotive market.

- At the same time, VinFast deepened its technology roadmap by partnering with NVIDIA and Autobrains on a level 4 autonomous driving platform tailored to Southeast Asia’s complex traffic conditions.

- Next, we’ll examine how VinFast’s rapid domestic EV delivery momentum could reshape its investment narrative around scale, margins, and technology.

Find 44 companies with promising cash flow potential yet trading below their fair value.

VinFast Auto Investment Narrative Recap

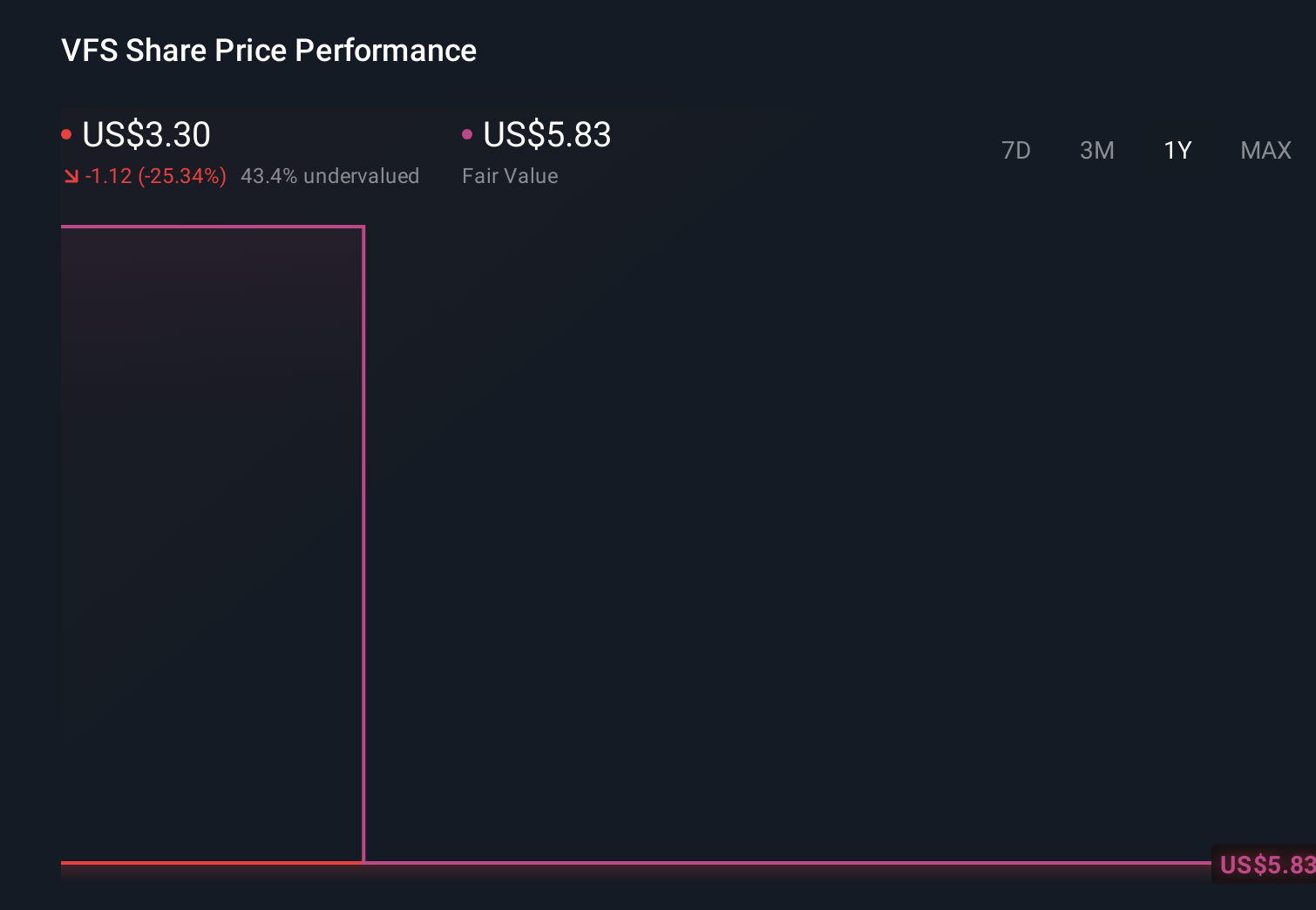

To own VinFast Auto, you need to believe that rapidly scaling EV volumes in Vietnam can eventually support better unit economics and fund its broader regional ambitions. The latest jump to nearly 100,000 domestic deliveries in five months supports the scale story, but Q1 2026 results with a wider net loss keep liquidity and ongoing cash burn as the key near term overhang. This delivery update does not materially change that central risk.

The new Level 4 autonomous driving collaboration with NVIDIA and Autobrains sits squarely in the technology catalyst bucket, giving VinFast access to a validated hardware and software stack for complex Southeast Asian driving conditions. For investors, it links the current delivery momentum with a longer term thesis that software and higher value features could eventually help margins, even as the company continues to absorb heavy upfront R&D and ecosystem investment.

Yet against this progress, the pressure from high cash burn and limited cash runway is information investors should be aware of...

Read the full narrative on VinFast Auto (it's free!)

VinFast Auto’s narrative projects ₫239006.9 billion in revenue and ₫6230.1 billion in earnings by 2029.

Uncover how VinFast Auto's forecasts yield a $6.30 fair value, a 100% upside to its current price.

Exploring Other Perspectives

Before this latest delivery surge, the most optimistic analysts were already assuming revenue could reach about ₫189,419.4 billion by 2028, which is far more upbeat than consensus and leans heavily on faster EV adoption and cheaper batteries to improve margins, while others worry that Vietnam concentration and ongoing losses could still cap the upside if these assumptions prove too ambitious.

Explore 5 other fair value estimates on VinFast Auto - why the stock might be worth less than half the current price!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your VinFast Auto research is our analysis highlighting 1 key reward and 3 important warning signs that could impact your investment decision.

- Our free VinFast Auto research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate VinFast Auto's overall financial health at a glance.

Contemplating Other Strategies?

Our top stock finds are flying under the radar-for now. Get in early:

- AI is about to change healthcare. These 40 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Invest in the nuclear renaissance through our list of 88 elite nuclear energy infrastructure plays powering the global AI revolution.

- The latest GPUs need a type of rare earth metal called Neodymium and there are only 30 companies in the world exploring or producing it. Find the list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com