- In its latest reported quarter, Green Plains Inc. posted a 25.89% year-over-year revenue decline and a very large year-over-year drop in net profit, while still ranking 6th out of 29 peers for financial health in the Renewable Energy industry.

- This combination of weaker quarterly performance and relatively strong balance sheet positioning creates a mixed picture that may influence how investors weigh Green Plains' transition plans and risk profile.

- Now we’ll consider how this steep quarterly revenue and profit deterioration interacts with Green Plains’ existing investment narrative and expectations.

Capitalize on the AI infrastructure supercycle with our selection of the 49 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

Green Plains Investment Narrative Recap

To own Green Plains, you have to believe in its shift from a traditional ethanol producer to a more diversified low carbon fuels and coproducts platform, supported by policy incentives and carbon credits. The latest quarter’s 25.89% revenue drop and sharp net profit decline highlight how exposed that story still is to weaker volumes and margins. For now, the setback does not appear to fundamentally alter the key near term catalyst of policy driven earnings from 45Z credits, but it does sharpen execution risk.

The most relevant recent development is Green Plains’ Q1 2026 report, which paired lower sales of US$445.8 million with a swing to net income of US$32.94 million from a loss a year earlier. In the context of the weak revenue headline, this raises important questions about how much of the profitability is tied to mix, efficiency, or one off factors and how repeatable those earnings are as the company pursues carbon, protein and low carbon fuel opportunities.

However, investors should be aware that the biggest policy related risk around carbon credits and incentives could...

Read the full narrative on Green Plains (it's free!)

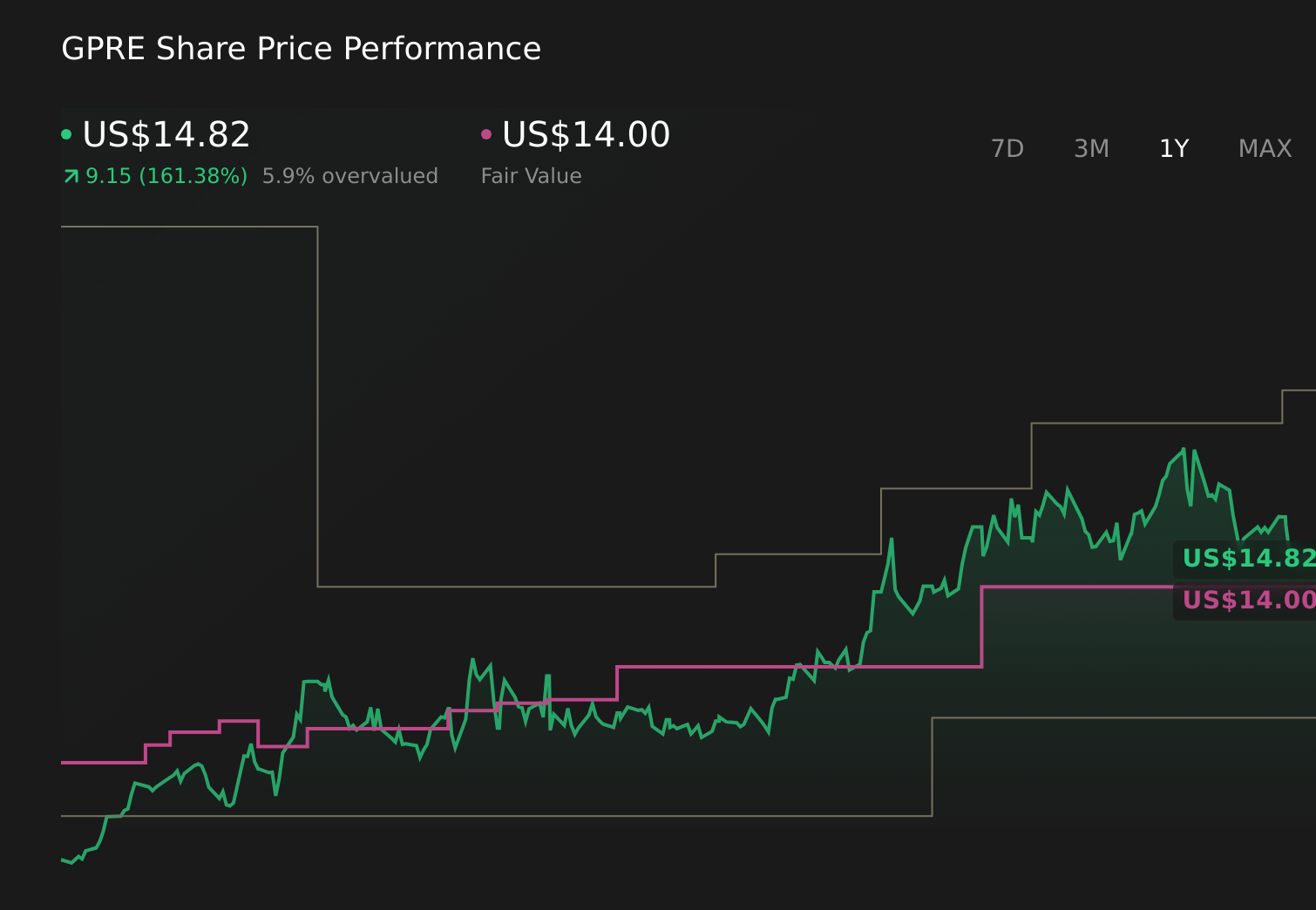

Green Plains' narrative projects $3.4 billion revenue and $116.3 million earnings by 2028. This requires 12.4% yearly revenue growth and a $268.2 million earnings increase from -$151.9 million today.

Uncover how Green Plains' forecasts yield a $14.00 fair value, a 4% downside to its current price.

Exploring Other Perspectives

Before this weak quarter, the most pessimistic analysts were already cautious, expecting revenue of about US$3.7 billion and earnings near US$176 million by 2029, yet still warning that heavy capital spending and volatile commodity markets could limit returns; compared with the baseline narrative that leans on policy support and efficiency gains, this more skeptical view underlines how sharply opinions differ and why you may want to compare several scenarios as new results emerge.

Explore 3 other fair value estimates on Green Plains - why the stock might be worth just $14.00!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Green Plains research is our analysis highlighting 4 key rewards that could impact your investment decision.

- Our free Green Plains research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Green Plains' overall financial health at a glance.

Contemplating Other Strategies?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- We've uncovered the 8 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- The future of work is here. Discover the 31 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Rare earth metals are the new gold rush. Find out which 31 stocks are leading the charge.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com