Virtu Financial (VIRT) is back in focus after its latest earnings report. Revenue grew by more than 30% year over year and net profit rose 84%, drawing fresh attention to the stock’s efficiency and valuation.

See our latest analysis for Virtu Financial.

Those results have arrived alongside strong momentum in Virtu Financial’s stock, with a 1 month share price return of 19.56% and a year to date share price return of 93.47%. The 3 year total shareholder return of 293.06% points to a longer track record of gains.

If this kind of move has you looking beyond Virtu Financial, it could be a good moment to see what else is setting up, starting with 20 top founder-led companies

So with Virtu Financial’s share price already sharply higher and revenue and profit moving strongly, is the stock still trading below its underlying value, or is the market already pricing in everything that could drive future growth?

Most Popular Narrative: 22% Overvalued

Against the latest close at $63.07, the most widely followed narrative for Virtu Financial pegs fair value at $51.71. This highlights a clear gap between price and modelled worth that hinges on how its earnings power evolves.

Virtu's investments in trading technology, cross asset platform integration, and digital asset capabilities (including crypto, stablecoins, and tokenized assets) position it to capture new wallet share, providing earnings growth and improved revenue diversification.

Want to see what is driving that value gap for Virtu Financial? The narrative leans heavily on shifting margins, changing revenue expectations, and a compressed future earnings multiple. Curious how those moving parts fit together into one payoff number? The full story is in the detailed forecast behind that fair value call.

Result: Fair Value of $51.71 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, there are still clear risks to the Virtu Financial story, including tougher competition from tech driven trading firms and potential regulatory shifts around digital assets and market structure.

Find out about the key risks to this Virtu Financial narrative.

Another View on Virtu Financial’s Valuation

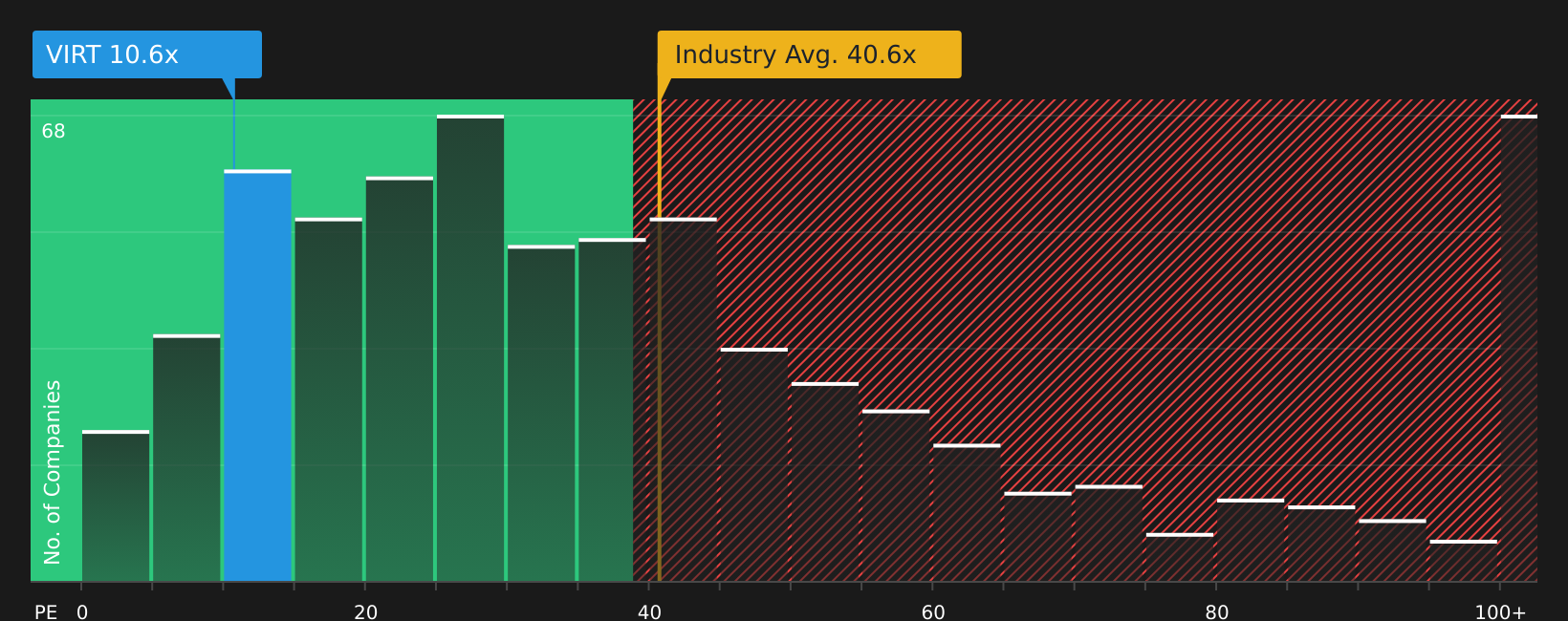

The analyst narrative argues Virtu Financial is about 22% overvalued at $63.07 based on a forward earnings model and a price target of $51.71. Yet on current numbers, VIRT trades on a P/E of 10.6x versus 27.4x for peers, 40.6x for the US Capital Markets industry, and a fair ratio of 15.5x. This points to a very different message about valuation risk and potential upside. Which lens do you put more weight on when the story you get depends on the model you use?

See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

After weighing both the earnings story and the valuation debate around Virtu Financial, are you leaning bullish or cautious, and how quickly will you test that view against the underlying numbers and assumptions? To see how the trade off between risks and rewards stacks up in one place, take a closer look at the 5 key rewards and 1 important warning sign

Looking For More Investment Ideas Beyond Virtu Financial?

If Virtu Financial has sharpened your focus, do not stop here, use Simply Wall Street’s powerful screener to uncover fresh stock ideas that fit your style.

- Target potential mispricings by scanning for companies that look attractively valued with healthy fundamentals using the 45 high quality undervalued stocks.

- Build a steadier income stream by zeroing in on companies with robust payouts through the 8 dividend fortresses.

- Limit unpleasant surprises by prioritizing resilience and balance sheet strength via the 66 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com