- Earlier this month, Hilton Grand Vacations Inc. completed a US$300,000,000 securitization of timeshare loans via Hilton Grand Vacations Trust 2026-2, issuing four tranches of notes with a weighted average coupon of 5.16% and an advance rate of 98% to refinance debt and support general corporate needs.

- This latest securitization underscores HGV’s continued use of asset-backed financing to support its timeshare business model and balance-sheet flexibility.

- Next, we’ll explore how this sizeable securitization, alongside recent strong revenue and profit growth, reshapes Hilton Grand Vacations’ investment narrative.

This technology could replace computers: discover 31 stocks that are working to make quantum computing a reality.

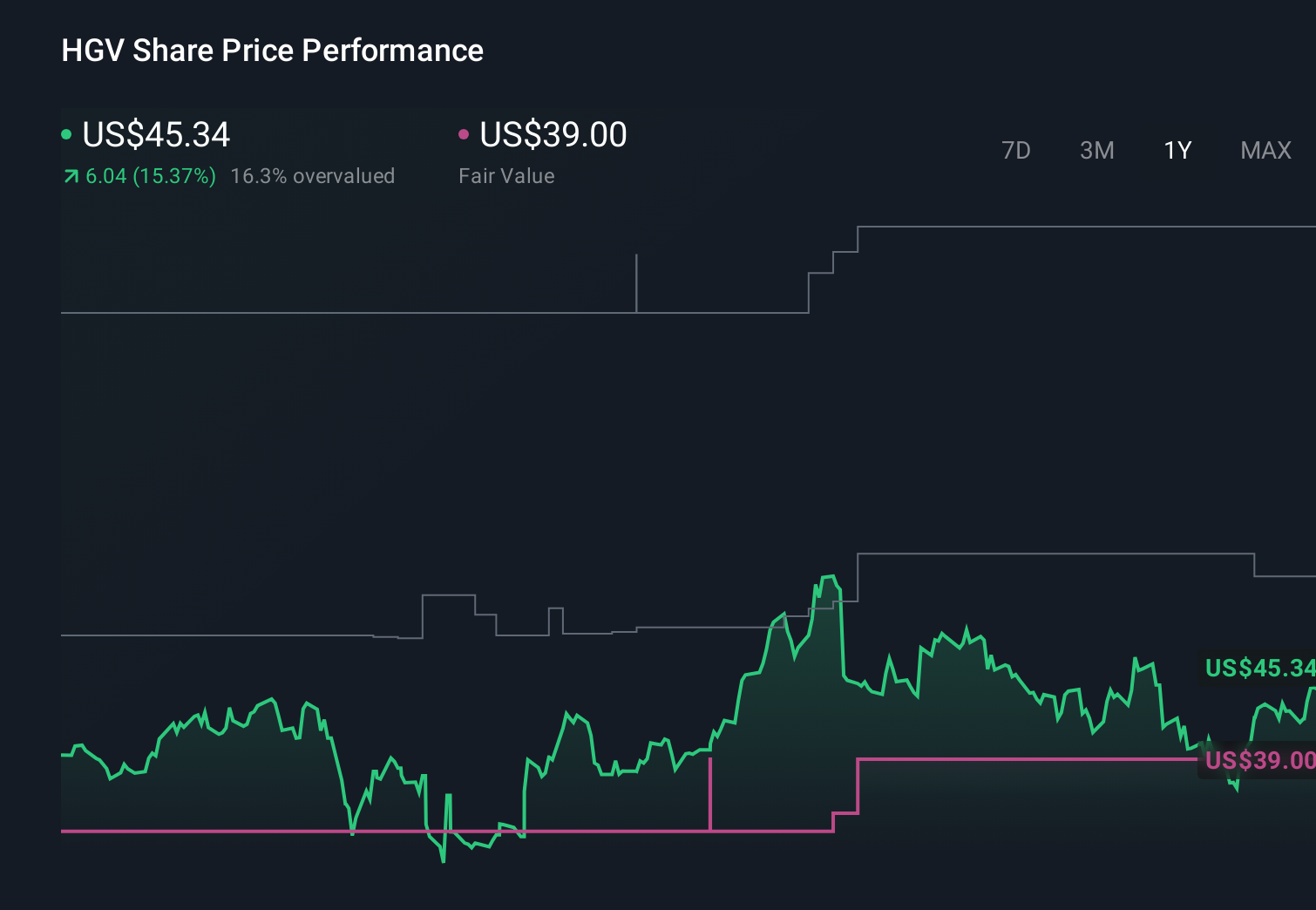

Hilton Grand Vacations Investment Narrative Recap

To own Hilton Grand Vacations, you need to believe its timeshare model, member programs, and acquisition integrations can translate into durable cash flows despite credit and demand risks. The new US$300,000,000 securitization improves near term funding flexibility, but does not materially change the key near term catalyst, which is continued revenue and earnings execution, or the main risk around elevated bad debt and timeshare loan defaults.

The most connected recent development is HGV’s upsized US$1,000,000,000 revolving warehouse facility, closed in May 2026. Together with the June securitization, it highlights how the company is leaning on receivables based financing to support inventory, integrations, and broader corporate needs at scale, which can influence how effectively it converts contract sales momentum and acquisition benefits into actual earnings and cash flow for shareholders.

Yet investors should be aware that if delinquency or default rates on HGV’s US$4,000,000,000 receivables portfolio were to worsen...

Read the full narrative on Hilton Grand Vacations (it's free!)

Hilton Grand Vacations' narrative projects $6.2 billion revenue and $472.1 million earnings by 2029.

Uncover how Hilton Grand Vacations' forecasts yield a $56.00 fair value, a 6% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were already assuming revenue could reach about US$6.2 billion and earnings US$549 million by 2029, so this latest securitization may either support that bullish capital access story or prompt a rethink of how funding, credit risk, and growth ambitions truly fit together.

Explore 4 other fair value estimates on Hilton Grand Vacations - why the stock might be worth just $56.00!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Hilton Grand Vacations research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Hilton Grand Vacations research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Hilton Grand Vacations' overall financial health at a glance.

Curious About Other Options?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- AI is about to change healthcare. These 40 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Capitalize on the AI infrastructure supercycle with our selection of the 49 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- Outshine the giants: these 14 early-stage AI stocks could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com