Navigator Holdings (NVGS) has drawn fresh attention after recent share price moves, with the stock down about 6% over the past month but up roughly 17% in the past 3 months.

See our latest analysis for Navigator Holdings.

Set against a 1 year total shareholder return of 50.56% and a 3 year total shareholder return of 76.29%, Navigator Holdings’ recent 7 day share price pullback of 5.61% suggests shorter term momentum is cooling after a stronger run.

If you are reassessing opportunities as energy related stocks move, it can be a good time to scan for other ideas using the 20 top founder-led companies

With Navigator Holdings now valued at about US$1.34b and trading at US$21.71 against an analyst price target of US$25.25, investors may ask whether there is still a buying opportunity or whether the current price already reflects its prospects.

Most Popular Narrative: 14% Undervalued

Compared with Navigator Holdings' last close at $21.71, the most followed narrative points to a fair value of $25.25, framing current pricing as a discount based on detailed earnings and revenue assumptions.

The continued structural shift toward cleaner fuels (like LPG and ammonia), together with industrial growth and higher living standards in emerging markets, is driving rising demand for liquefied gas and petrochemical transport; Navigator is already seeing restored trade volumes post-Q2 disruption, supporting higher utilization and revenue growth.

Curious what justifies a higher value for Navigator Holdings even as consensus points to lower future revenue and earnings and a richer future P/E multiple than the sector, all discounted back at a specific required return and tied to shrinking share count assumptions.

Result: Fair Value of $25.25 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, for Navigator Holdings this narrative still hinges on volatile charter rates and geopolitical disruptions that could quickly pressure utilization, margins, and the implied higher future P/E.

Find out about the key risks to this Navigator Holdings narrative.

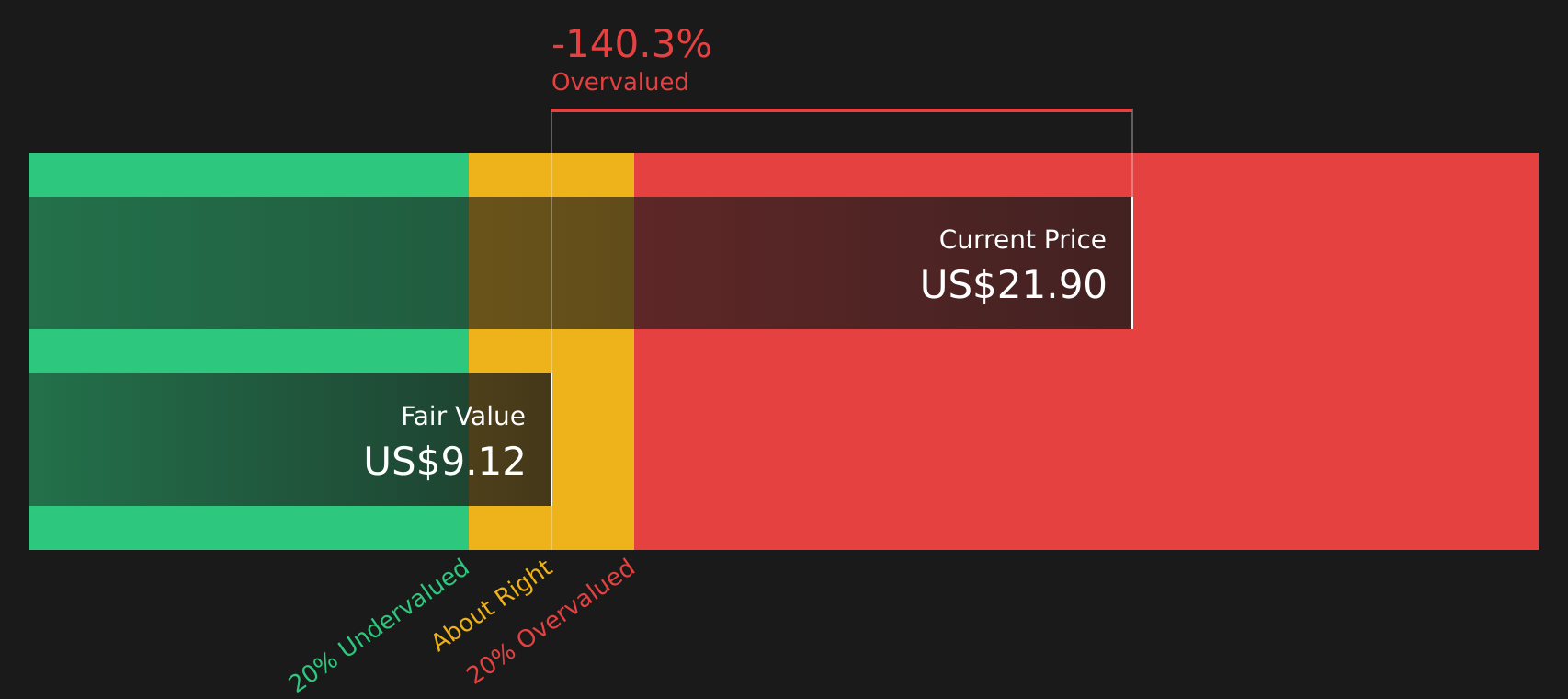

Another View: SWS DCF Model Flags Overvaluation

While analyst narratives frame Navigator Holdings as about 14% undervalued at $25.25 fair value, the Simply Wall St DCF model points in the opposite direction, with an estimated future cash flow value of $9.12 per share, well below the current $21.71 price. This raises the question of which lens you trust more.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Navigator Holdings for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 45 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

Given the mixed signals around Navigator Holdings, it can help to move quickly, review the numbers yourself, and weigh both the potential and the concerns by checking the 2 key rewards and 4 important warning signs.

Looking for more investment ideas beyond Navigator Holdings?

If Navigator Holdings has sharpened your focus, do not stop here. Broadening your watchlist with other stocks can surface opportunities you would not want to miss.

- Spot potential bargains early by scanning screener containing 19 high quality undiscovered gems that combine quality fundamentals with limited market attention.

- Prioritize resilience by reviewing 65 resilient stocks with low risk scores designed to highlight companies with calmer risk profiles.

- Target dependable balance sheets by checking the solid balance sheet and fundamentals stocks screener (48 results) and focus on businesses with stronger financial footing.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com