- In recent days, Napco Security Technologies reported a strong institutional shareholding profile, with institutions now owning more than the company’s total shares outstanding and increasing their stakes quarter-over-quarter.

- The company also delivered improved financial health, with quarterly revenue growing year-over-year and net profit more than doubling, pointing to stronger efficiency and resilience in its operations.

- We’ll now examine how rising institutional ownership, alongside improving profitability metrics, may influence Napco Security Technologies’ broader investment narrative.

Capitalize on the AI infrastructure supercycle with our selection of the 49 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

Napco Security Technologies Investment Narrative Recap

To own Napco Security Technologies, you need to believe its mix of security hardware and higher margin recurring services can offset pressure on equipment profitability. The latest data on rising institutional ownership and improved profitability metrics supports that view in the near term, but does not materially change the key short term catalyst, which remains stabilizing hardware margins, or the biggest risk around concentration in a few recurring revenue platforms.

The most relevant recent announcement here is Napco’s quarterly report showing year over year revenue growth and more than doubled net profit. That improvement in financial health slightly strengthens the case that recurring services and operational efficiency can cushion hardware volatility, but it does not remove concerns about dependence on products like StarLink Fire radios or the potential impact of further margin pressure if demand softens.

Yet behind this improving profitability profile, there is a risk investors should be aware of around...

Read the full narrative on Napco Security Technologies (it's free!)

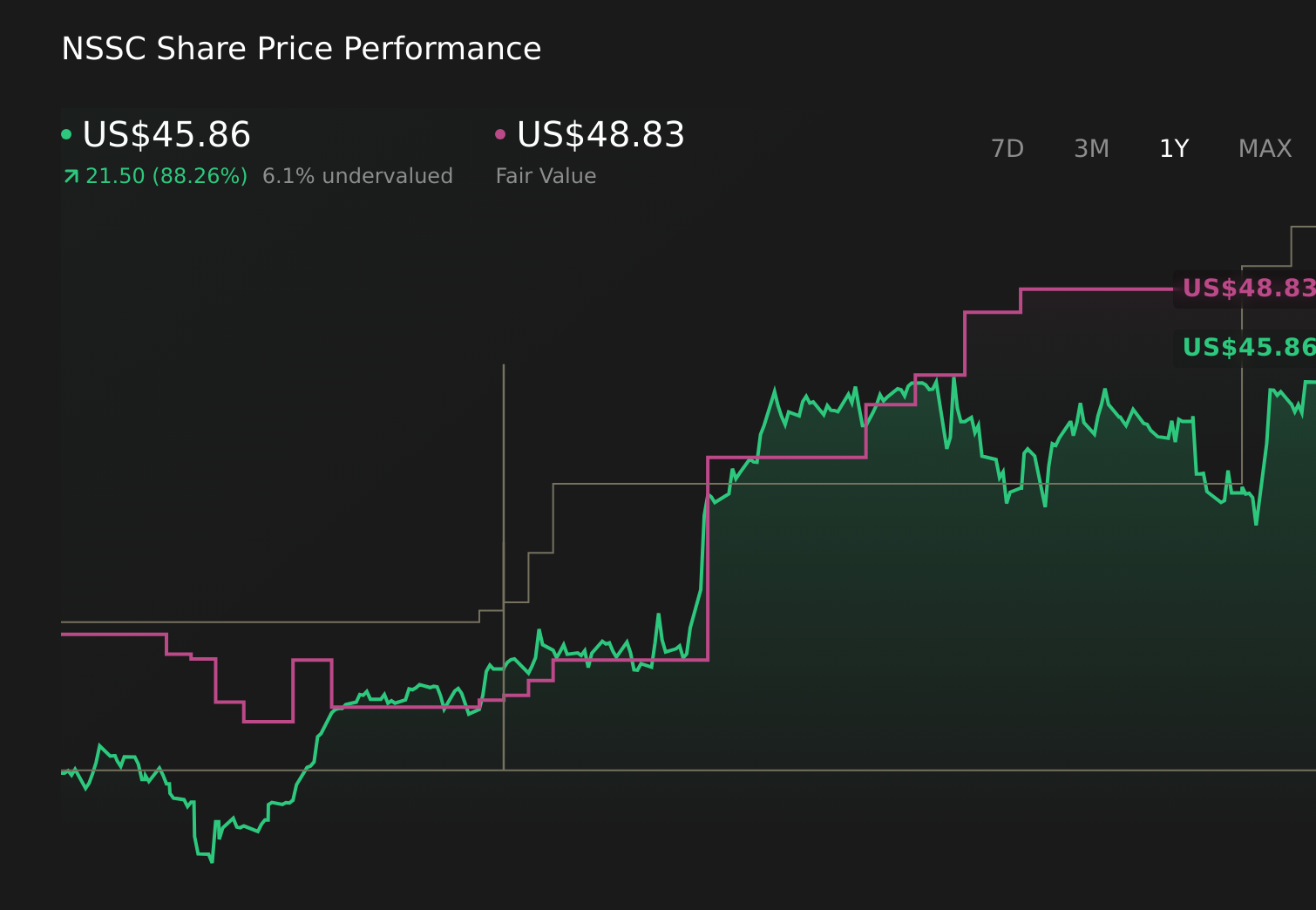

Napco Security Technologies' narrative projects $253.7 million revenue and $96.3 million earnings by 2029. This implies 8.8% yearly revenue growth and about a $59.4 million earnings increase from $36.9 million today.

Uncover how Napco Security Technologies' forecasts yield a $50.33 fair value, a 35% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were assuming earnings could reach about US$101.7 million by 2029, yet the latest mix of strong institutional buying and ongoing reliance on a narrow set of recurring products highlights how differently you might assess Napco’s future and why it is worth comparing several viewpoints before deciding what this new information means for you.

Explore 3 other fair value estimates on Napco Security Technologies - why the stock might be worth as much as 35% more than the current price!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Napco Security Technologies research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Napco Security Technologies research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Napco Security Technologies' overall financial health at a glance.

Looking For Alternative Opportunities?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- The future of work is here. Discover the 31 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 14 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- We've uncovered the 8 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com