Centuri Holdings (CTRI) drew investor attention after announcing more than $360 million in new commercial awards, highlighting fresh contract wins with both existing and new customers across utility and data center markets.

See our latest analysis for Centuri Holdings.

Despite the contract wins, Centuri Holdings’ 7 day share price return declined 2.34%. However, its year to date share price return of 19.48% and 1 year total shareholder return of 44.09% suggest momentum has been building over a longer stretch.

If this infrastructure story has your attention, it could be a good moment to look at other grid focused opportunities and check out 34 power grid technology and infrastructure stocks

With Centuri Holdings posting solid reported revenue and net income growth alongside a roughly $3.0b market value and a recent close of $30.85, the key question is whether the current price still leaves room for opportunity or already reflects potential future growth.

Most Popular Narrative: 6.4% Overvalued

Centuri Holdings closed at $30.85, slightly above the most widely followed fair value estimate of $29.00 that anchors the current bullish narrative.

Record backlog of about $5.9b and an opportunity pipeline of roughly $13b, including more than 600 strategic bids, gives the company multi year visibility on awarded and potential work, which can support sustained revenue and better fixed cost absorption over time.

Want to understand why some investors think Centuri Holdings can grow into that price? The narrative leans heavily on sustained revenue expansion, rising margins and a tighter earnings multiple. The exact mix of growth, profitability and discounting behind that $29.00 fair value may surprise you.

Result: Fair Value of $29.00 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, Centuri Holdings still faces pressure from higher leverage and softer Non Union Electric margins, which could limit the extent of the current growth narrative.

Find out about the key risks to this Centuri Holdings narrative.

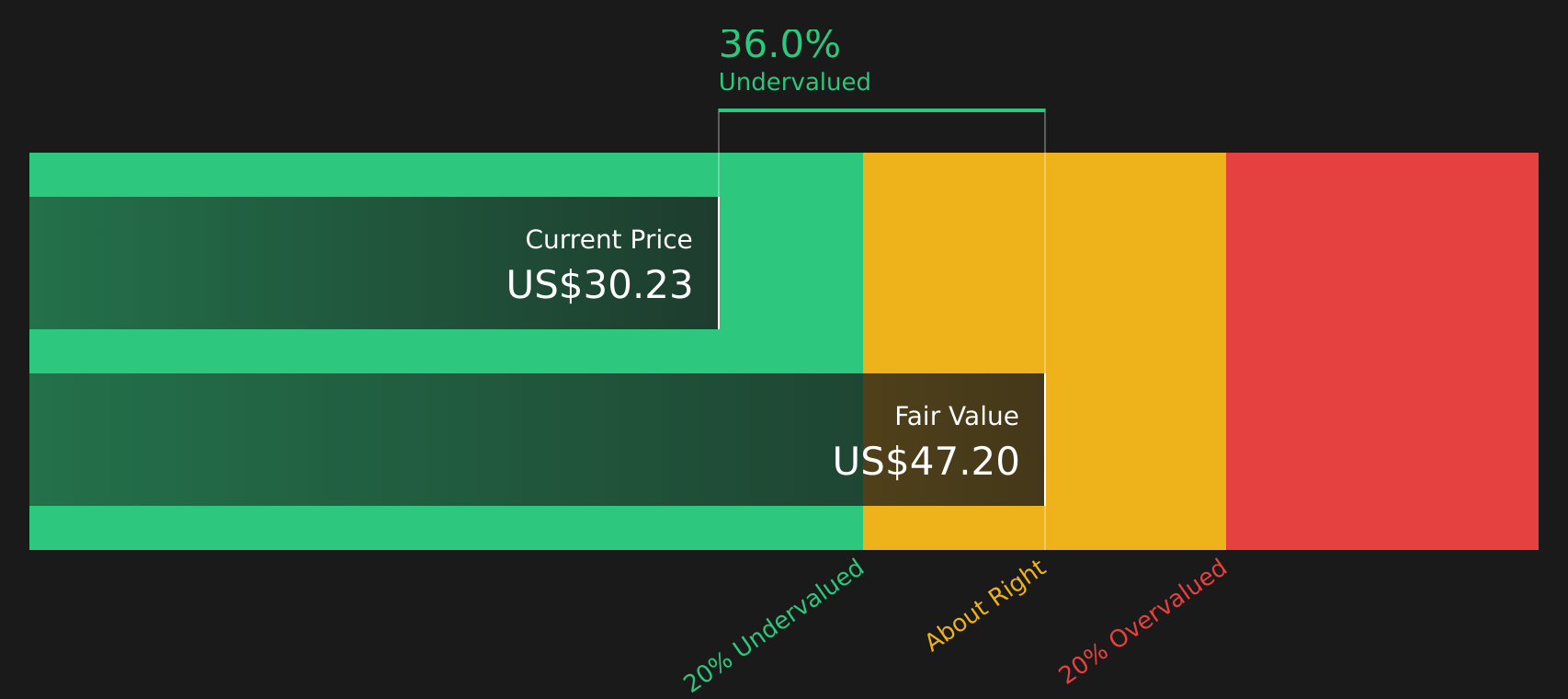

Another View: SWS DCF Fair Value for Centuri Holdings

The earlier narrative framed Centuri Holdings as 6.4% overvalued at $30.85 versus a $29.00 fair value. Our DCF model points in the opposite direction, suggesting fair value of $47.15 and implying the stock trades about 34.6% below that estimate. Which story feels more realistic to you?

Before leaning toward either conclusion, it is worth understanding how our DCF model turns future cash flow assumptions into that $47.15 figure and what would need to change for the gap to close, or widen, over time. Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Centuri Holdings for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 44 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

Are there mixed messages in the Centuri Holdings story so far? Use this as a starting point, review the underlying data yourself, and then weigh the 4 key rewards and 2 important warning signs.

Looking for more investment ideas beyond Centuri Holdings?

If Centuri Holdings has sharpened your focus on infrastructure, do not stop here. The best opportunities often show up where fewer people are already looking.

- Spot potential value candidates early by reviewing companies highlighted in the 44 high quality undervalued stocks built from Simply Wall St's data driven filters.

- Target income focused opportunities by scanning the 7 dividend fortresses that zero in on stocks with higher yields.

- Prioritise resilience by checking companies in the 66 resilient stocks with low risk scores so you are not the last to notice stronger balance sheets and steadier profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com