Over the last 7 days, the United States market has experienced a 2.3% drop, yet it remains robust with a 21% increase over the past year and an earnings forecast predicting a 19% annual growth. In this dynamic environment, identifying lesser-known stocks with strong fundamentals and growth potential can offer unique opportunities for investors seeking to capitalize on these positive trends.

Top 10 Undiscovered Gems With Strong Fundamentals In The United States

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Imperial Petroleum | NA | 29.81% | 34.96% | ★★★★★★ |

| Brady | 2.00% | 6.15% | 10.01% | ★★★★★☆ |

| CF Bankshares | 63.11% | -6.95% | -10.61% | ★★★★★☆ |

| Waterdrop | 5.26% | 2.09% | 66.26% | ★★★★★☆ |

| Fortress Biotech | 19.46% | 0.53% | 26.21% | ★★★★★☆ |

| Alto Ingredients | 29.24% | -3.75% | -29.59% | ★★★★★☆ |

| TOYO | 57.03% | 225.22% | 49.41% | ★★★★☆☆ |

| Meridian | 86.20% | -9.29% | -18.08% | ★★★★☆☆ |

| Betterware de MéxicoP.I. de | 273.07% | 9.15% | -7.33% | ★★★☆☆☆ |

| GDEV | NA | 3.52% | 49.82% | ★★★☆☆☆ |

We're going to check out a few of the best picks from our screener tool.

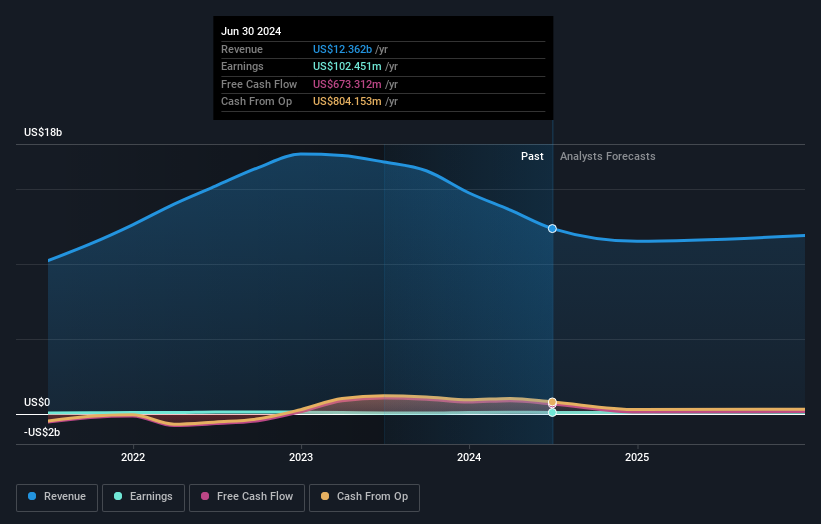

TOYO (TOYO)

Simply Wall St Value Rating: ★★★★☆☆

Overview: TOYO Co., Ltd. operates in the solar power supply chain, covering upstream wafer and silicon production to downstream photovoltaic module manufacturing in Asia and the United States, with a market cap of approximately $429.90 million.

Operations: TOYO generates revenue primarily from its Machinery & Industrial Equipment segment, which accounts for $518.61 million. The company's operations span the solar power supply chain, including wafer and silicon production, solar cell manufacturing, and photovoltaic module assembly in Asia and the United States.

TOYO has been making waves with its impressive earnings growth of 203.6% over the past year, significantly outpacing the Semiconductor industry's 22.6%. The company is trading at a notable discount, valued 83.3% below estimated fair value, while maintaining a satisfactory net debt to equity ratio of 18.1%. Recent strategic moves include a $357 million investment in a new U.S.-based solar cell facility expected to create around 400 jobs and generate operational synergies by co-locating with existing operations in Texas. Additionally, TOYO's recent agreements for $185.6 million worth of high-efficiency solar modules underscore its expanding footprint in the U.S. market.

- Click to explore a detailed breakdown of our findings in TOYO's health report.

Gain insights into TOYO's past trends and performance with our Past report.

Andersons (ANDE)

Simply Wall St Value Rating: ★★★★☆☆

Overview: The Andersons, Inc. is an agriculture and renewable fuels company with operations in the United States, Canada, Mexico, and internationally, and has a market cap of approximately $2.39 billion.

Operations: Andersons generates revenue primarily from its agribusiness and renewables segments, with $8.19 billion coming from agribusiness and $2.79 billion from renewables.

Andersons, a nimble player in the agricultural sector, is making strategic moves with its full ownership of ethanol plants and focus on carbon reduction initiatives. These efforts are poised to boost cash flow and profit margins as regulatory support for renewable fuels grows. The company's recent financial results show net income of US$33.19 million for Q1 2026, a significant leap from US$0.28 million the previous year, with earnings per share rising to US$0.98 from US$0.01. Despite high net debt to equity at 94.4%, Andersons has reduced its debt ratio over five years, demonstrating improved financial discipline amidst volatile commodity markets and expansion challenges.

Ategrity Specialty Insurance Company Holdings (ASIC)

Simply Wall St Value Rating: ★★★★★★

Overview: Ategrity Specialty Insurance Company Holdings operates through its subsidiaries to offer excess and surplus lines insurance and reinsurance products to small and medium-sized businesses in the United States, with a market cap of approximately $1.03 billion.

Operations: ASIC generates revenue primarily from its insurance business, which contributes $470.18 million. The company's market cap stands at approximately $1.03 billion.

Ategrity Specialty Insurance Company Holdings showcases impressive growth, with earnings surging 91.8% over the past year, outpacing the insurance industry's 36.5%. The company appears undervalued, trading at 44.9% below its estimated fair value, and remains debt-free, which enhances its financial stability. Recent results highlight a robust performance with Q1 revenue of US$128.96 million compared to US$83.12 million last year and net income jumping to US$25.47 million from US$8.46 million previously. Basic earnings per share rose to US$0.53 from US$0.2, reflecting strong operational efficiency and profitability potential in this niche market segment.

Summing It All Up

- Unlock more gems! Our US Undiscovered Gems With Strong Fundamentals screener has unearthed 14 more companies for you to explore.Click here to unveil our expertly curated list of 17 US Undiscovered Gems With Strong Fundamentals.

- Already own these companies? Link your portfolio to Simply Wall St and get alerts on any new warning signs to your stocks.

- Simply Wall St is your key to unlocking global market trends, a free user-friendly app for forward-thinking investors.

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com