- Earlier in 2026, Cabot Corporation released its 2026 Sustainability Report, revealing it met 14 of 15 2025 sustainability goals, with 11 achieved ahead of schedule and highlighting sharp reductions in nonhazardous landfill waste.

- The report also outlined early progress toward Cabot’s 2030 Sustainability Goals, including work on product carbon footprints and beneficial reuse of materials, signaling how environmental performance is being embedded into the company’s operations.

- We’ll now examine how Cabot’s ahead-of-schedule sustainability achievements, particularly its steep landfill waste reduction, could influence its broader investment narrative.

Find 43 companies with promising cash flow potential yet trading below their fair value.

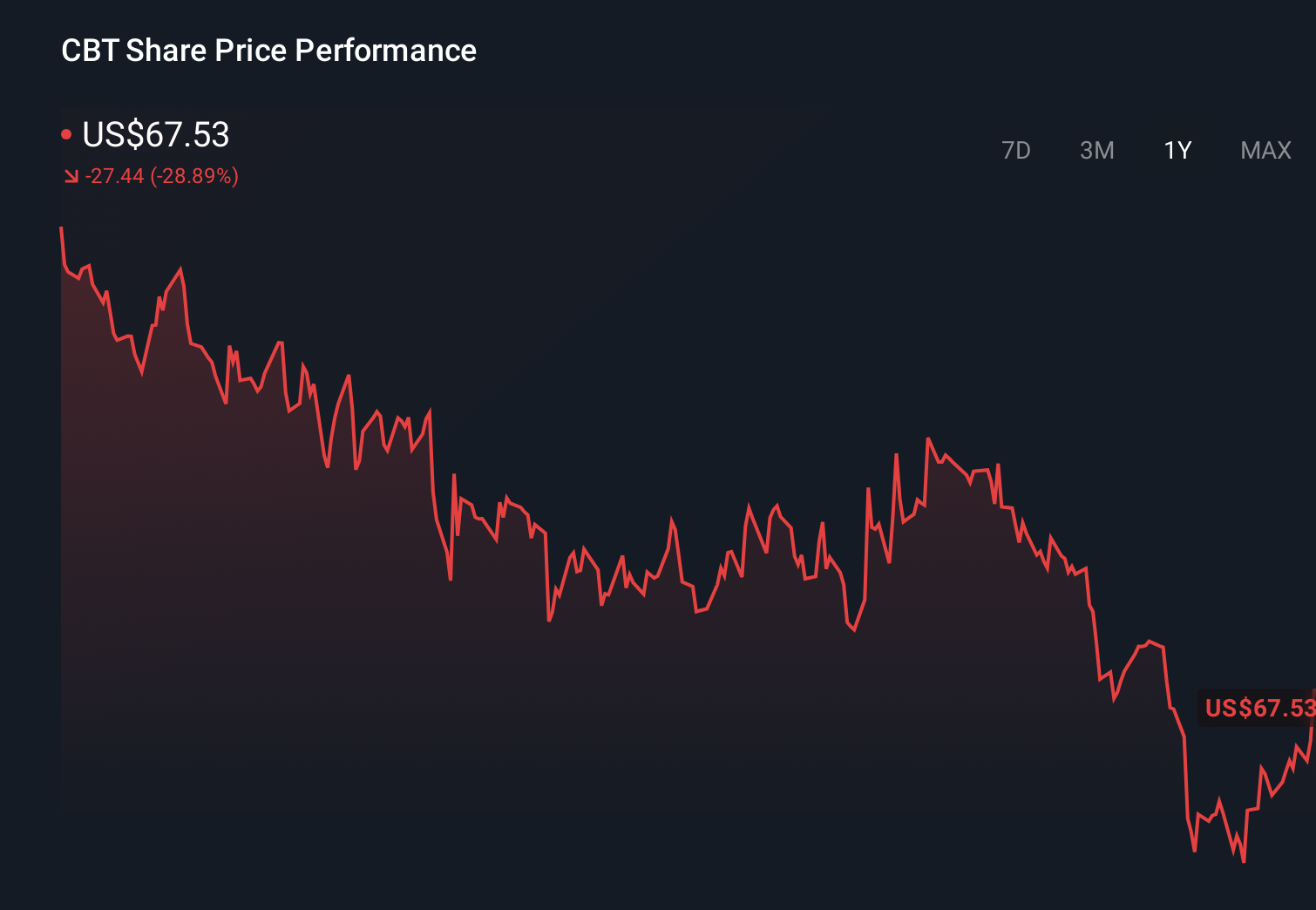

Cabot Investment Narrative Recap

To own Cabot, you need to believe its specialty materials portfolio in batteries, tires and infrastructure can keep converting long duration demand into solid cash generation, even as earnings have recently softened. The 2026 Sustainability Report, with 14 of 15 goals met and sharp landfill waste reductions, supports Cabot’s positioning with customers and regulators, but does not meaningfully change the near term focus on Battery Materials growth as a key catalyst or margin pressure in Reinforcement Materials as a central risk.

The most relevant recent announcement alongside the sustainability update is Cabot’s new US$1.3 billion unsecured revolving credit facility maturing in 2031. Together, the strengthened liquidity and credible progress on 2030 sustainability goals may give Cabot additional flexibility to keep funding battery materials projects and network optimization efforts, even as it works through near term earnings pressure and capacity rationalizations that could reshape its cost base.

However, while Cabot’s sustainability execution looks encouraging, investors should also be aware that...

Read the full narrative on Cabot (it's free!)

Cabot's narrative projects $4.0 billion revenue and $479.7 million earnings by 2029. This requires 3.4% yearly revenue growth and about a $198.7 million earnings increase from $281.0 million today.

Uncover how Cabot's forecasts yield a $85.67 fair value, a 8% downside to its current price.

Exploring Other Perspectives

Before this sustainability news, the most optimistic analysts were assuming Cabot could lift earnings to about US$499 million by 2029 on higher margins, which is far more upbeat than consensus and could be challenged if Reinforcement Materials pricing pressure, already visible in recent EBIT declines, proves harder to offset than those bullish models assume.

Explore 4 other fair value estimates on Cabot - why the stock might be worth 16% less than the current price!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Cabot research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Cabot research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Cabot's overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- Explore 30 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- Uncover the next big thing with 22 elite penny stocks that balance risk and reward.

- Capitalize on the AI infrastructure supercycle with our selection of the 50 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com