Otter Tail (OTTR) is back in focus after the company and two subsidiaries agreed to a $30 million settlement with the End-User Class in the ongoing PVC Pipe Antitrust Litigation.

See our latest analysis for Otter Tail.

Beyond the legal headlines, Otter Tail’s share price has been firm, with a 7 day share price return of 3.58% and an 11.27% year to date share price return at a last close of $90.63. The 5 year total shareholder return of 111.79% suggests momentum has built over a longer horizon.

If this legal update has you thinking more broadly about utilities and infrastructure, it could be a good moment to see what else is moving through 35 power grid technology and infrastructure stocks

So with Otter Tail trading around its analyst price target and screens suggesting it is above some intrinsic value estimates, are you looking at an underappreciated utility stock or one where the market is already pricing in future growth?

Most Popular Narrative: 10% Overvalued

Otter Tail is trading at $90.63, slightly above the narrative fair value of $90.50, which prices in a detailed view of future earnings and margins.

The analysts have a consensus price target of $90.5 for Otter Tail based on their expectations of its future earnings growth, profit margins and other risk factors.

In order for you to agree with the analysts, you would need to believe that by 2029, revenues will be $1.4 billion, earnings will come to $206.7 million, and it would be trading on a PE ratio of 22.7x, assuming you use a discount rate of 7.1%.

The fair value hinges on slower revenue growth, slimmer margins, and a richer earnings multiple than today. Want to see how those moving parts fit together?

Result: Fair Value of $90.50 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, Otter Tail could challenge that overvalued label if its $1.4b utility capital plan delivers the projected 9% earnings growth, or if large new load contracts materialize.

Find out about the key risks to this Otter Tail narrative.

Another View: What Otter Tail’s P/E Ratio Is Saying

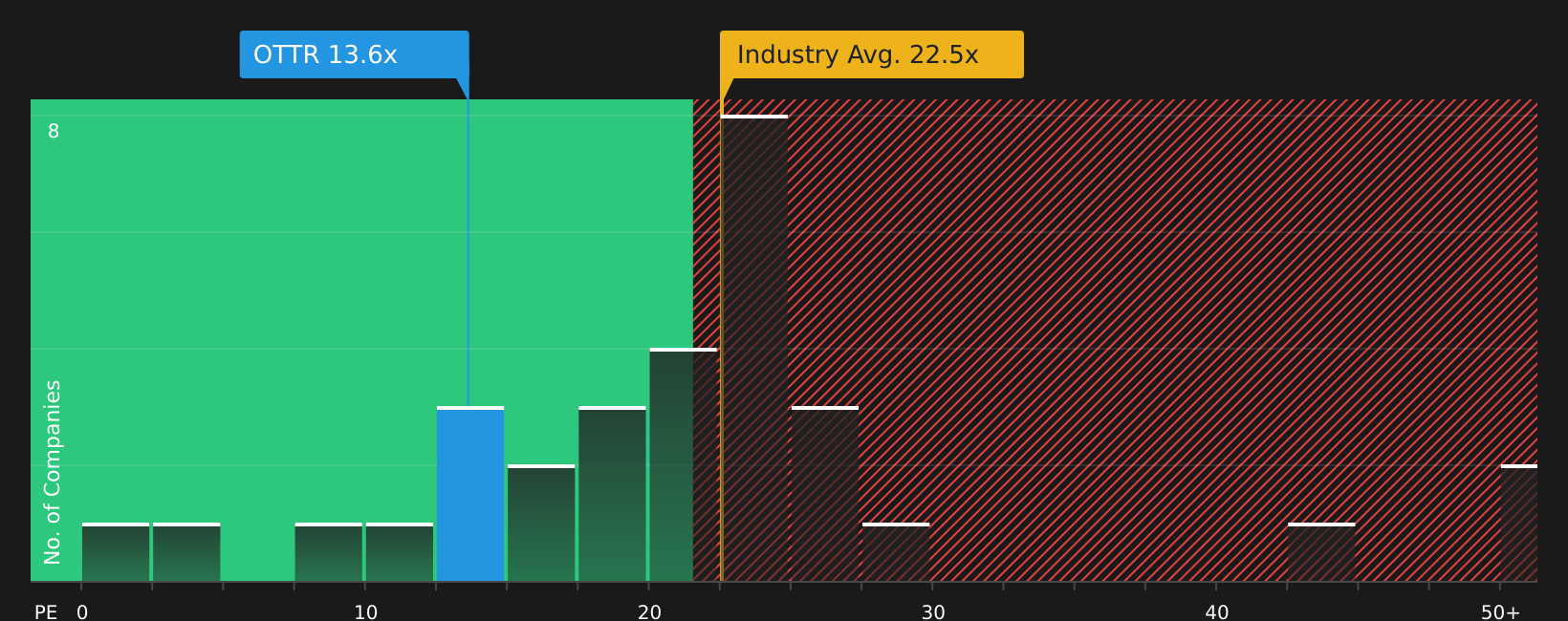

The first narrative flagged Otter Tail as roughly 10% overvalued on future earnings assumptions, but the current P/E ratio of 13.6x tells a different story. That is lower than the US Electric Utilities industry at 22.2x and below the 27.1x peer average.

At the same time, Otter Tail trades slightly above its fair ratio of 13.2x. This suggests the market is already pricing in a bit more optimism than that statistical benchmark implies. For investors weighing valuation risk, the question is whether the business can keep justifying that premium.

See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

With mixed signals on valuation and sentiment around Otter Tail, this is the moment to look closely at the numbers and form your own judgment, starting with the 1 key reward and 3 important warning signs.

Looking for more investment ideas beyond Otter Tail?

If Otter Tail has sharpened your focus on valuation and quality, do not stop here, the next strong idea in your portfolio could be just one screen away.

- Target potential bargains with resilient earnings by scanning 44 high quality undervalued stocks that align with disciplined price and quality checks.

- Strengthen your income stream by reviewing 8 dividend fortresses that combine higher yields with a focus on durability.

- Prioritize capital protection first by assessing 71 resilient stocks with low risk scores designed for steadier business and financial profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com