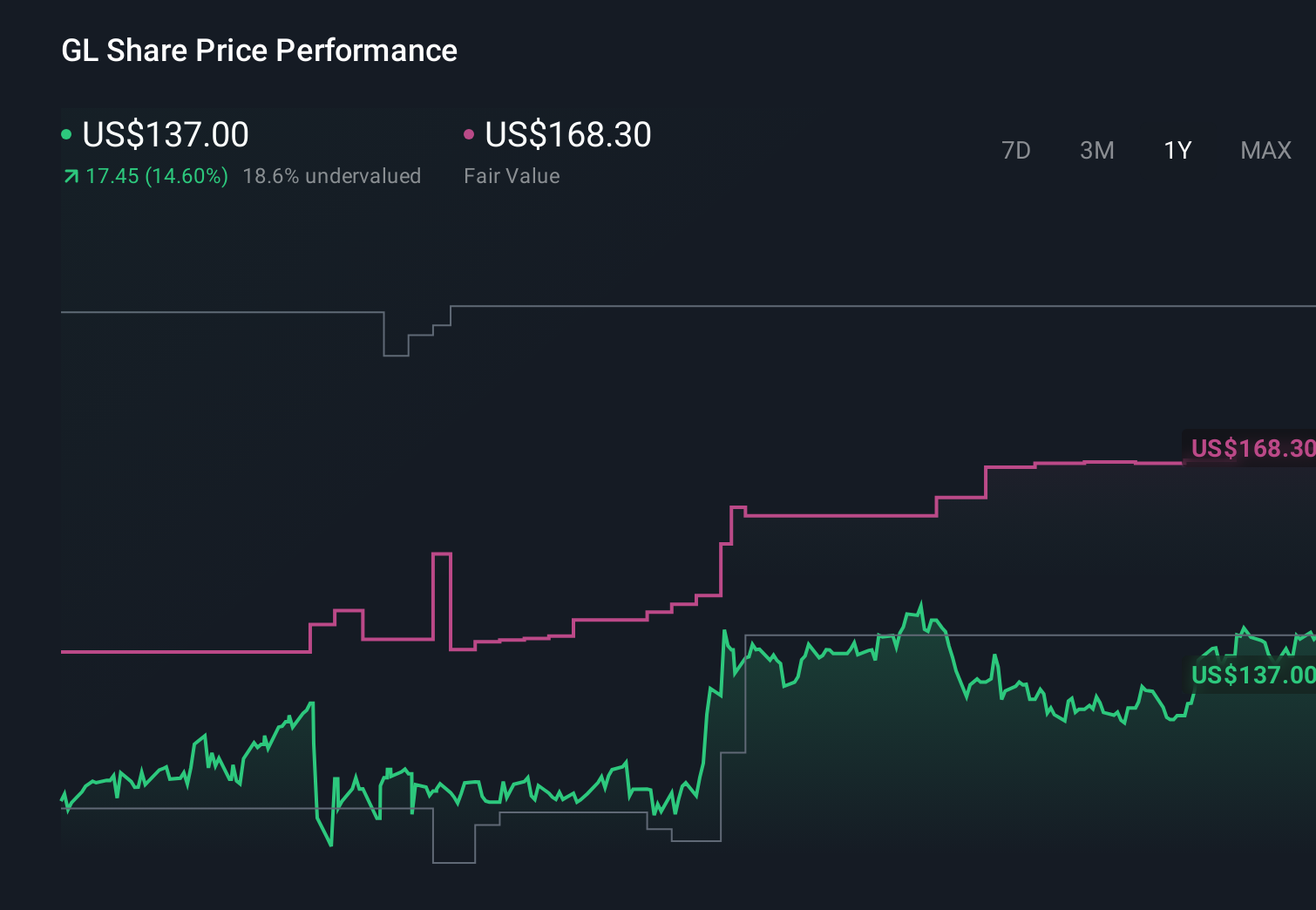

- In recent months, Globe Life reported quarterly results that matched revenue expectations but missed earnings and book value per share estimates, while executive Rebecca E. Zorn exercised options and sold 2,000 shares at around US$170 per share in June 2026.

- Despite the softer quarter, analysts continue to highlight Globe Life’s expected 6.3% sales growth for 2026 and favorable ranking as evidence of persistent business momentum.

- Next, we’ll examine how this analyst-backed sales growth outlook reshapes Globe Life’s investment narrative and its long-term earnings profile.

The future of work is here. Discover the 29 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

Globe Life Investment Narrative Recap

To own Globe Life, you need to believe that its agent-driven model and demand for life and supplemental health coverage can support steady sales, even as distribution and customer preferences evolve. The latest quarter’s miss on EPS and book value per share, alongside insider selling by Rebecca E. Zorn, does not appear to materially alter the near term focus on sales growth or the ongoing risk from regulatory and distribution shifts.

The most relevant recent announcement here is Globe Life’s reaffirmed 2026 earnings guidance and continued share repurchases, including 1.4 million shares bought back in Q1 2026 for US$238.61 million. This capital return stance, combined with analysts highlighting an expected 6.3% sales growth rate for 2026, frames the current debate around whether the stock’s post earnings strength is backed by durable fundamentals or vulnerable to the existing regulatory and distribution risks.

But beneath the solid sales outlook, one risk investors should be aware of is the ongoing regulatory and investigation overhang that could...

Read the full narrative on Globe Life (it's free!)

Globe Life's narrative projects $6.8 billion revenue and $1.3 billion earnings by 2028.

Uncover how Globe Life's forecasts yield a $172.10 fair value, a 4% downside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts paint a much more cautious picture, assuming revenue only reaches about US$7.2 billion and earnings US$1.3 billion by 2029, so it is worth comparing that pessimistic view with Globe Life’s current sales momentum and capital returns before deciding which narrative you find more convincing.

Explore 3 other fair value estimates on Globe Life - why the stock might be worth just $172.10!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Globe Life research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Globe Life research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Globe Life's overall financial health at a glance.

Ready For A Different Approach?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- Uncover the next big thing with 21 elite penny stocks that balance risk and reward.

- Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

- We've uncovered the 8 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com