- On 27 June 2026, Permian Resources Corporation (NYSE: PR) was added to multiple Russell growth benchmarks, including the Russell 1000 Growth, 2500 Growth, 3000 Growth, 3000E Growth, Midcap Growth, and Small Cap Comp Growth indices.

- This broad index inclusion can channel more benchmark-driven and institutional capital towards Permian Resources, potentially affecting liquidity, ownership mix, and how investors assess its growth profile.

- We’ll now examine how Permian Resources’ broad Russell growth index inclusion could influence its investment narrative and longer-term positioning.

We've uncovered the 8 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

Permian Resources Investment Narrative Recap

To own Permian Resources, you need to believe its Permian Basin drilling inventory, efficiency, and balance sheet can support resilient free cash flow despite commodity and regulatory uncertainty. The broad Russell growth index additions may reinforce its growth identity and improve liquidity, but they do not fundamentally change the near term dependence on supportive oil and gas prices or the risk that high ongoing capital spending could pressure future free cash flow.

Among recent developments, the February 2026 guidance for 2026 production of 400,000 to 430,000 Boe/d, with oil at 186,000 to 192,000 Bbls/d, is most relevant. Index inclusion will likely influence who owns the stock, while the production plan and required capital intensity remain central to the earnings and free cash flow story investors are evaluating.

But against this backdrop, the bigger issue investors should be watching is the risk that sustained high capex and well declines could...

Read the full narrative on Permian Resources (it's free!)

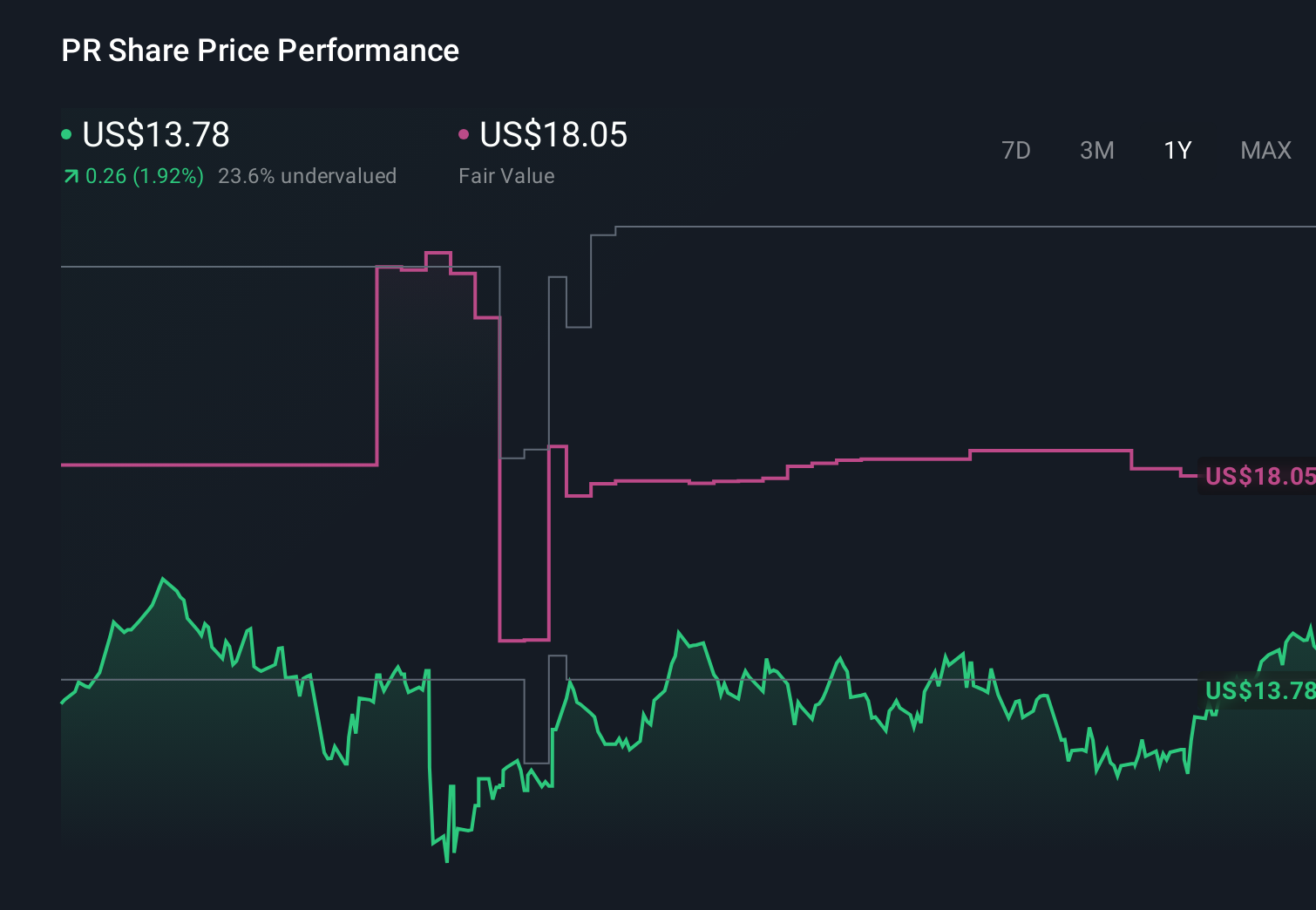

Permian Resources' narrative projects $6.3 billion revenue and $1.6 billion earnings by 2029.

Uncover how Permian Resources' forecasts yield a $25.72 fair value, a 37% upside to its current price.

Exploring Other Perspectives

Some of the lowest analysts were already cautious, assuming earnings of about US$1.4 billion by 2029, and they may see these Russell inclusions very differently from those focused on operational efficiencies and acquisition driven growth.

Explore 5 other fair value estimates on Permian Resources - why the stock might be worth over 3x more than the current price!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Permian Resources research is our analysis highlighting 3 key rewards and 4 important warning signs that could impact your investment decision.

- Our free Permian Resources research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Permian Resources' overall financial health at a glance.

Ready For A Different Approach?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- Capitalize on the AI infrastructure supercycle with our selection of the 51 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- The future of work is here. Discover the 29 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- AI is about to change healthcare. These 40 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com