- FB Financial Corporation has announced it will release its second-quarter 2026 results on July 13 after market close, followed by an earnings call on July 14, and has authorized a new US$175,000,000 share repurchase program running through June 30, 2027.

- This combination of an upcoming earnings update and a sizeable buyback authorization highlights management’s confidence and has drawn fresh attention from analysts.

- We’ll now explore how the newly authorized US$175,000,000 share repurchase program may influence FB Financial’s existing investment narrative.

The future of work is here. Discover the 29 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

FB Financial Investment Narrative Recap

To own FB Financial you need to be comfortable with a regional bank story built on loan growth, disciplined funding costs and the planned Southern States combination, while accepting exposure to credit quality and policy uncertainty. The new US$175,000,000 buyback and upcoming Q2 2026 update do not change the core near term swing factor, which remains how well FB Financial balances growth with credit and deposit cost pressures, nor the key risk around its Commercial and Industrial portfolio and integration execution.

The fresh share repurchase authorization is the clearest recent announcement to watch alongside the earnings call, as it interacts directly with the existing catalyst of “strong capital levels and potential for strategic deployment.” Together with prior repurchases and regular dividends, it frames how much financial flexibility FB Financial still has to support organic loan growth and the Southern States combination, especially if credit costs or funding competition were to stay challenging.

Yet behind the headline of a larger buyback, investors should be aware of how integration risk around Southern States could...

Read the full narrative on FB Financial (it's free!)

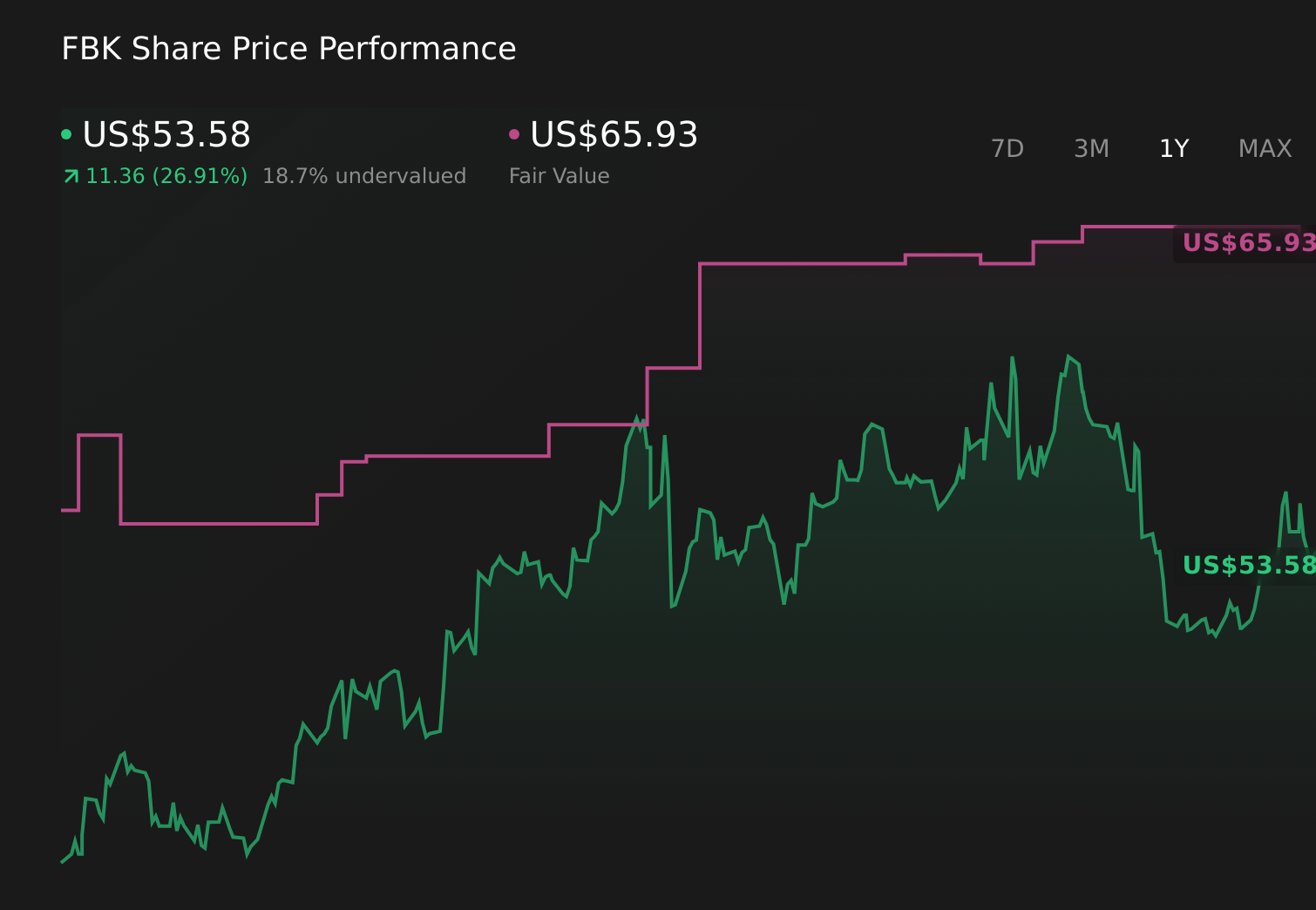

FB Financial's narrative projects $1.0 billion revenue and $415.1 million earnings by 2029.

Uncover how FB Financial's forecasts yield a $64.43 fair value, a 16% upside to its current price.

Exploring Other Perspectives

Two Simply Wall St Community fair value estimates for FB Financial span roughly US$64 to just over US$101, showing how far apart individual views can be. Against that backdrop, the coming earnings update and the bank’s ongoing credit and integration risks give you several very different scenarios to consider for FB Financial’s future performance.

Explore 2 other fair value estimates on FB Financial - why the stock might be worth as much as 84% more than the current price!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your FB Financial research is our analysis highlighting 2 key rewards that could impact your investment decision.

- Our free FB Financial research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate FB Financial's overall financial health at a glance.

Ready For A Different Approach?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 15 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- Capitalize on the AI infrastructure supercycle with our selection of the 51 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- Uncover the next big thing with 22 elite penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com