3M (MMM) has attracted fresh attention after announcing two high profile partnerships: a long term supply agreement with Airbus for the A220 and a multi year materials collaboration with the Cadillac Formula 1 Team.

See our latest analysis for 3M.

Recent partnerships with Airbus and the Cadillac Formula 1 Team come as 3M’s share price has risen 10.72% over 90 days and 5.98% over 30 days, while its 1 year total shareholder return of 5.83% contrasts with a very large 3 year total shareholder return of 112.86%. This suggests momentum has strengthened lately compared with earlier softness this year.

If these moves have you thinking more broadly about materials and industrial trends, it could be a good moment to scan the market via our robotics and automation stocks screener 29 robotics and automation stocks

So with 3M trading at $159.96 against an analyst price target of $171.02 and an estimated 25.05% intrinsic discount, should you see current levels as a value opportunity, or assume the market is already pricing in future growth?

Most Popular Narrative: 6.4% Undervalued

The most followed narrative values 3M at $170.97 a share, a touch above the recent $159.96 close, and frames that gap around execution on margins and growth.

Significant operational efficiency gains, such as improved on-time delivery, increased equipment effectiveness, quality cost reductions, and supply chain/process consolidation, are driving structurally higher operating margins and earnings, benefits expected to compound as further optimization and automation are rolled out company-wide.

Curious what underpins that fair value for 3M? The narrative leans heavily on steadier revenue progress, a sizable lift in profitability, and a future earnings multiple that needs to compress. The exact mix of those assumptions might matter more than the headline discount itself.

Result: Fair Value of $170.97 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, there are still clear pressure points for 3M. Unresolved PFAS related litigation and ongoing macro sensitivity in automotive and electronics demand are both capable of undermining this margin led narrative.

Find out about the key risks to this 3M narrative.

Another View: 3M Through the P/E Lens

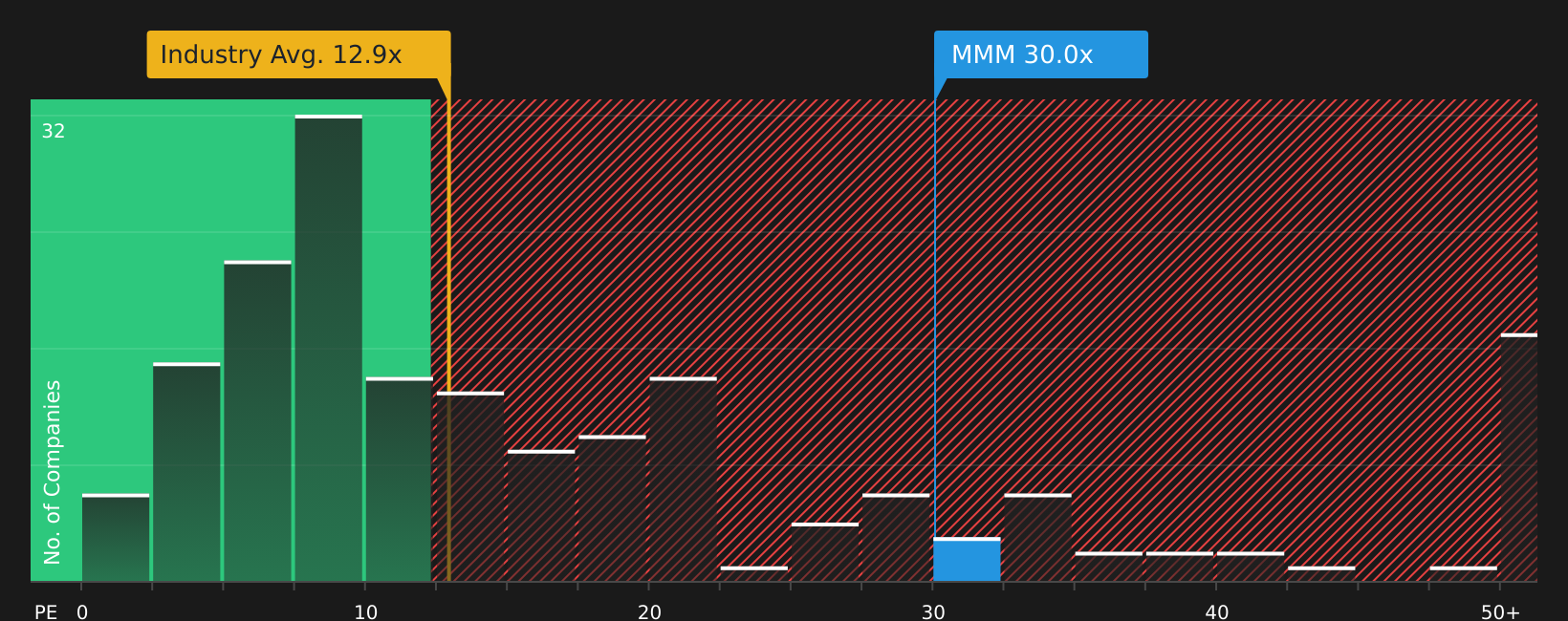

While the SWS model flags 3M as trading below an estimate of fair value, the P/E picture is less forgiving. At 29.9x earnings, 3M trades well above the global Industrials average of 13.4x and only slightly below its own fair ratio of 33.7x, which points to limited margin for error if earnings disappoint. Is that premium something you are comfortable paying for this story?

To pressure test that premium further, take a closer look at how the current P/E stacks up against the fair ratio and sector peers in the detailed valuation breakdown See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

If this mix of optimism and concern around 3M leaves you undecided, act while the data is fresh and weigh the trade off yourself with 2 key rewards and 3 important warning signs

Looking for more investment ideas beyond 3M?

Once you have a handle on 3M, do not stop there. Broaden your watchlist with fresh stock ideas that match your preferred balance between value, income, and resilience.

- Target potential bargains by scanning companies that combine quality fundamentals with attractive pricing using the 41 high quality undervalued stocks.

- Strengthen your income stream by reviewing stocks that offer robust yields and payout profiles through the 10 dividend fortresses.

- Prioritize capital preservation by focusing on companies that score well for resilience and stability via the 73 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com