- On 27 June 2026, Everus Construction Group, Inc. (NYSE: ECG) was added to several Russell Growth benchmarks, including the Russell 1000, 3000, 3000E, 2500, Midcap, and Small Cap Composite Growth Indexes.

- This broad index inclusion can expand Everus Construction Group’s presence in benchmark-driven portfolios, potentially increasing its shareholder base and influencing trading liquidity over time.

- Next, we’ll examine how Everus Construction Group’s addition to multiple Russell Growth indexes might influence its existing investment narrative.

Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

Everus Construction Group Investment Narrative Recap

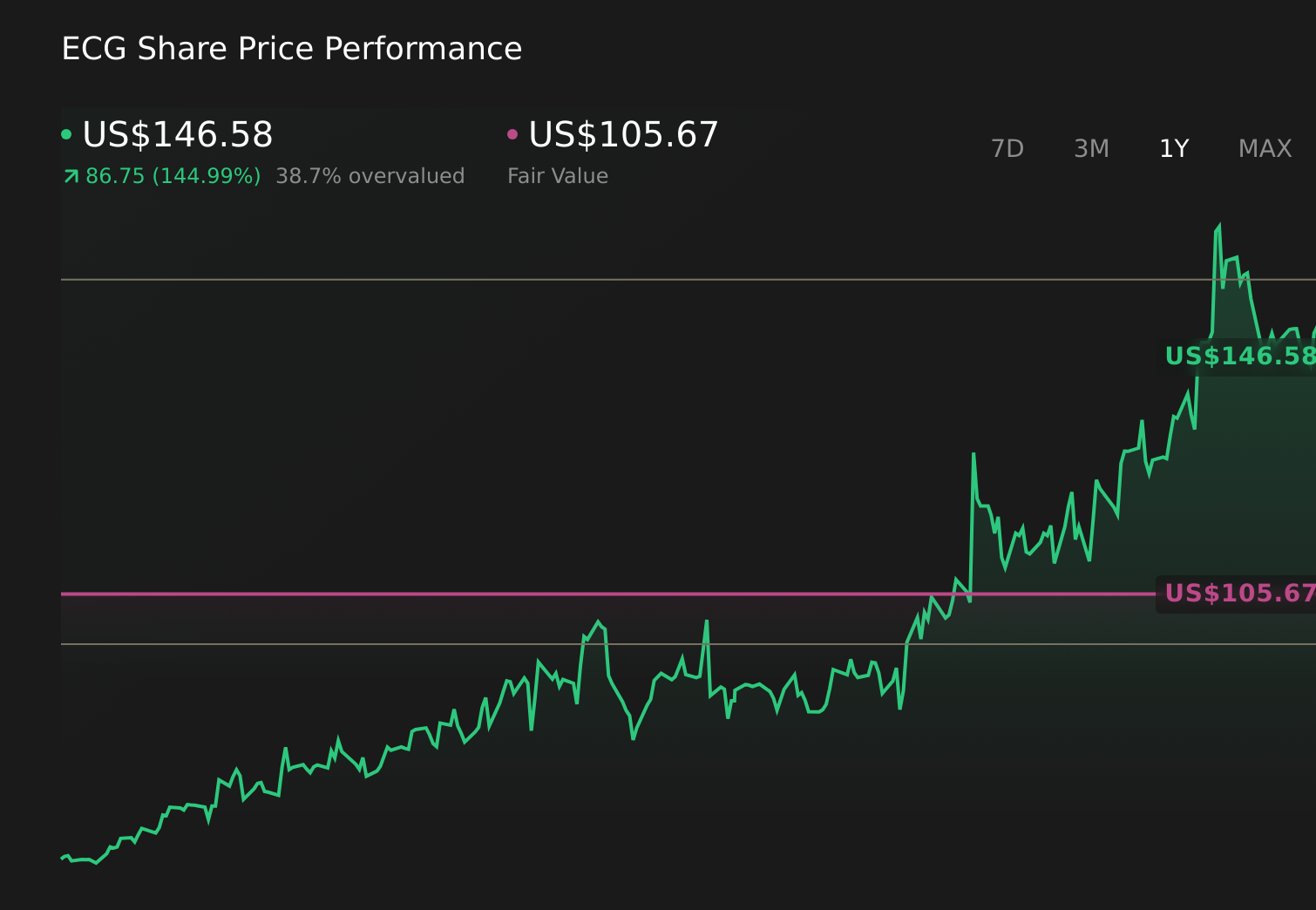

To own Everus Construction Group, you need to believe that demand for complex power and data center infrastructure can support disciplined growth, while the company manages execution risk and capital deployment. The Russell Growth index additions raise Everus’ profile and may influence liquidity, but they do not change the core near term catalyst, which is converting its large project pipeline into profitable work. The biggest current risk remains any slowdown or normalization in data center and high value project activity.

The most relevant recent announcement alongside the Russell inclusions is the May 2026 guidance raise, which lifted 2026 revenue expectations to US$4.3 billion to US$4.4 billion, helped by the SE&M acquisition. This frames the index news against an already upgraded operational outlook, where investors are focused on whether Everus can sustain above trend earnings growth and margins while stepping up M&A without eroding returns on invested capital.

Yet behind the strong guidance and index inclusion, there is a risk investors should be aware of if backlog momentum or data center demand were to...

Read the full narrative on Everus Construction Group (it's free!)

Everus Construction Group's narrative projects $4.3 billion revenue and $220.5 million earnings by 2028. This requires 7.2% yearly revenue growth and a $39.5 million earnings increase from $181.0 million today.

Uncover how Everus Construction Group's forecasts yield a $105.67 fair value, a 30% downside to its current price.

Exploring Other Perspectives

While consensus focuses on disciplined growth, the most optimistic analysts were already banking on revenue reaching about US$5.3 billion and earnings near US$296.9 million, so you should recognize that views differ widely and that fresh events like the Russell additions could push those bullish expectations or the backlog driven risk narrative in very different directions.

Explore 4 other fair value estimates on Everus Construction Group - why the stock might be worth less than half the current price!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Everus Construction Group research is our analysis highlighting 3 key rewards that could impact your investment decision.

- Our free Everus Construction Group research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Everus Construction Group's overall financial health at a glance.

No Opportunity In Everus Construction Group?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- The future of work is here. Discover the 29 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Outshine the giants: these 15 early-stage AI stocks could fund your retirement.

- The latest GPUs need a type of rare earth metal called Dysprosium and there are only 31 companies in the world exploring or producing it. Find the list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com