Hims & Hers Health (HIMS) is back in focus after securing a $400 million financing arrangement with JPMorgan Chase Bank. This move improves liquidity while regulatory scrutiny of its peptide ambitions intensifies.

See our latest analysis for Hims & Hers Health.

At a share price of $37.57, Hims & Hers Health has seen strong short term momentum, with a 1 month share price return of 35.34% and 90 day share price return of 96.29%, while the 1 year total shareholder return declined 20.84% but the 3 year total shareholder return is more than 3x.

If this mix of fast growth themes and regulatory questions interests you, it can be useful to see what else is moving in healthcare technology, starting with 39 healthcare AI stocks

With Hims & Hers Health trading at $37.57, above the average analyst price target and alongside rapid revenue and net income growth but ongoing losses and regulatory questions, is there still a buying opportunity here, or is the market already pricing in future growth?

Most Popular Narrative: 78.3% Undervalued

Compared to the last close of $37.57, the most followed narrative on Hims & Hers Health points to a fair value of $173.02, framing the current price as a steep discount based on long term expansion assumptions.

Over the long term (10yrs), Hims & Hers has an unusually large addressable market ahead of it. The company’s growth is driven by three reinforcing dimensions:

• Expanding market size, as digital healthcare adoption continues to grow globally

• Category expansion, including new offerings such as hormonal health, longevity, and sleep

• International scaling, with multiple geographies already in the pipeline (e.g. Brazil, Australia)

• Growth inside of the current categories

This narrative, set out by Deep_Insights, focuses on rapid revenue expansion, rising margins and a premium future earnings multiple to support that higher fair value.

Want to see how those revenue assumptions, margin targets and future earnings multiple all connect back to a $173.02 fair value for Hims & Hers Health? The full narrative details the growth path, category mix and profitability profile that underpin this valuation, so you can review how those numbers compare.

Result: Fair Value of $173.02 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, Hims & Hers Health still faces meaningful risks, including regulatory pushback on peptide and weight loss offerings and the challenge of turning revenue growth into consistent profits.

Find out about the key risks to this Hims & Hers Health narrative.

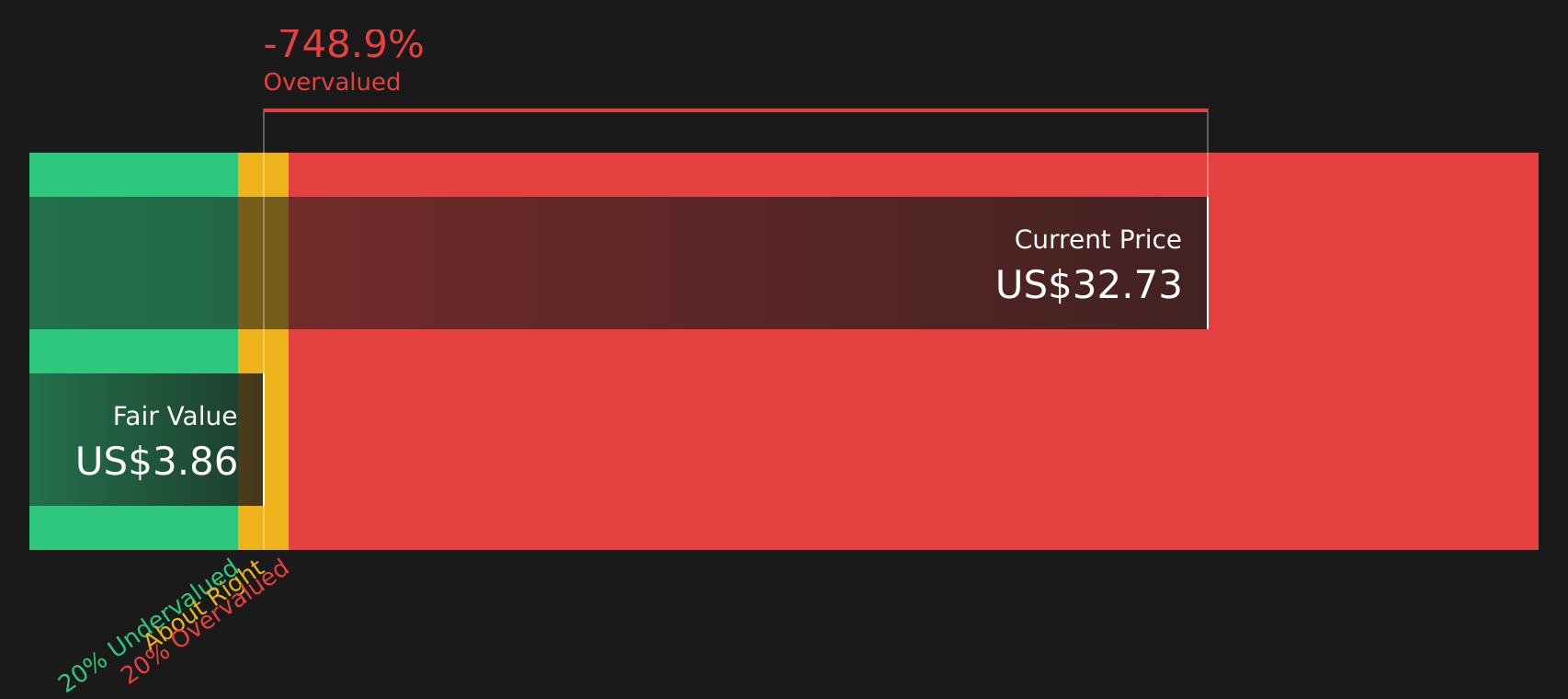

Another View: SWS DCF Model Points To Overvaluation

While the most popular Hims & Hers Health narrative sees the stock as materially undervalued at a fair value of $173.02, the SWS DCF model tells a very different story. On that view, the current price of $37.57 sits well above an estimated future cash flow value of $3.86, implying the shares look expensive on this framework.

For investors, this kind of gap between a narrative driven valuation and a cash flow based model raises a simple question: which set of assumptions feels closer to how Hims & Hers Health will actually convert growth into long term cash generation?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Hims & Hers Health for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 41 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

Given the split views on Hims & Hers Health and its mix of risks and rewards, it makes sense to review the numbers for yourself and decide where you stand, including the 1 key reward and 1 important warning sign.

Looking for more investment ideas beyond Hims & Hers Health?

If Hims & Hers Health has sharpened your interest in growth and risk trade offs, do not stop here, widen your watchlist with focused stock ideas.

- Target potential mispricings by scanning companies that pair quality fundamentals with attractive prices using the 41 high quality undervalued stocks.

- Strengthen income potential by reviewing stocks with robust yields and resilience profiles via the 8 dividend fortresses.

- Prioritize capital protection by searching for companies screened for sturdier balance sheets and lower risk signals through the 73 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com