- In late June 2026, BioAge Labs began dosing participants in QUELL-CV, a Phase 2 proof-of-concept trial of its oral NLRP3 inhibitor BGE-102 for cardiovascular risk reduction, following earlier Phase 1 data showing strong hsCRP reductions and good tolerability.

- This step advances BioAge’s pipeline from early safety testing toward assessing real-world cardiovascular outcomes, sharpening investor focus on its inflammation-targeted approach to heart disease.

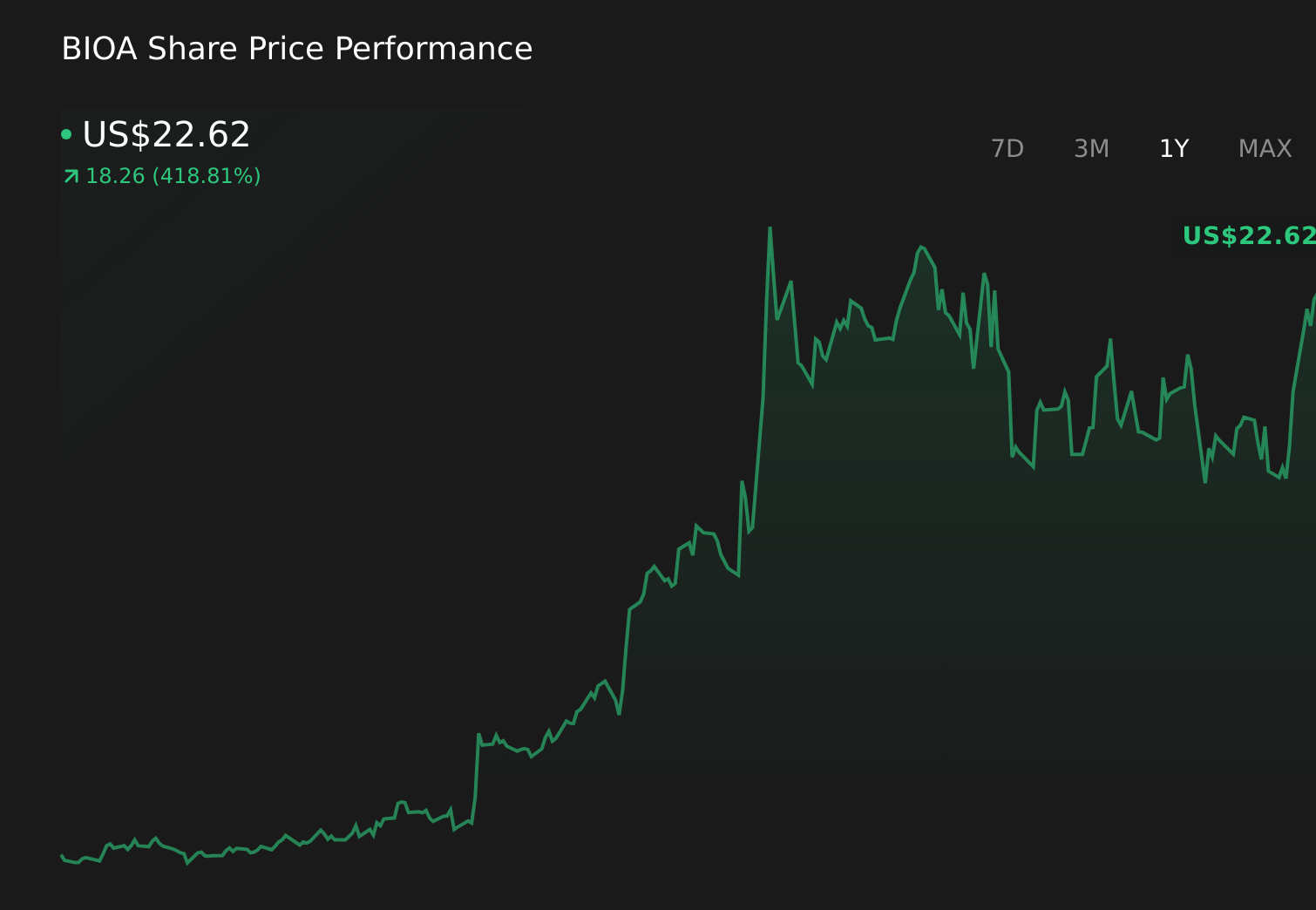

- Next, we’ll explore how initiating the QUELL-CV Phase 2 study for BGE-102 shapes BioAge Labs’ investment narrative and risk profile.

We've uncovered the 8 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

What Is BioAge Labs' Investment Narrative?

To own BioAge Labs today, you really have to believe that an inflammation-focused NLRP3 inhibitor can become a meaningful tool in managing cardiovascular risk, and that the company can survive a long stretch of losses while it tests that thesis. The start of QUELL-CV and BioAge’s inclusion in multiple Russell growth and microcap indices pull more investor attention to that single bet and may support trading liquidity, but they do not change the basic near-term catalysts: clean Phase 2 hsCRP data in H2 2026 and progress on the ophthalmology program. On the risk side, a widening net loss of about US$89.93 million, slow forecast revenue growth and ongoing equity issuance remain front and center, even with the share price up sharply.

However, one funding-related issue may matter more than recent index additions, and investors should know why. Our expertly prepared valuation report on BioAge Labs implies its share price may be too high.Exploring Other Perspectives

Explore 2 other fair value estimates on BioAge Labs - why the stock might be worth over 8x more than the current price!

Reach Your Own Conclusion

Disagree with this assessment? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your BioAge Labs research is our analysis highlighting 3 important warning signs that could impact your investment decision.

- Our free BioAge Labs research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate BioAge Labs' overall financial health at a glance.

Searching For A Fresh Perspective?

Our top stock finds are flying under the radar-for now. Get in early:

- Find 41 companies with promising cash flow potential yet trading below their fair value.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 15 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- Capitalize on the AI infrastructure supercycle with our selection of the 53 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com