- NNN REIT, Inc. recently exercised its US$200 million incremental term loan option, expanding its senior unsecured term loan facility to US$500 million maturing in 2029, while also amending pricing grids on its term loan and revolving credit facility and entering a US$100 million forward starting swap to fix SOFR.

- The combination of lower SOFR-based margins and interest rate hedging may modestly trim borrowing costs and add visibility to future interest expenses, with proceeds earmarked for general corporate purposes.

- Next, we’ll assess how this incremental term loan and lower credit facility margins may influence NNN REIT’s existing investment narrative.

AI is about to change healthcare. These 40 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

NNN REIT Investment Narrative Recap

To own NNN REIT, you need to be comfortable with a slower growth, income-focused profile that leans on stable rent streams and disciplined balance sheet management. The expanded US$500,000,000 term loan, slightly lower SOFR-based margins and additional hedging appear supportive but do not materially alter the near term narrative, where the key catalyst remains execution on accretive acquisitions and the biggest risk is still tenant credit quality and broader retail pressure.

Against this backdrop, the reaffirmed 2026 earnings guidance of US$2.02 to US$2.08 per share (excluding certain items) is the most relevant recent data point, as it provides a reference for how management currently sees earnings holding up while interest costs, tenant health and acquisition conditions evolve alongside the new debt structure.

Yet investors should be aware that tenant bankruptcies and consolidations could still...

Read the full narrative on NNN REIT (it's free!)

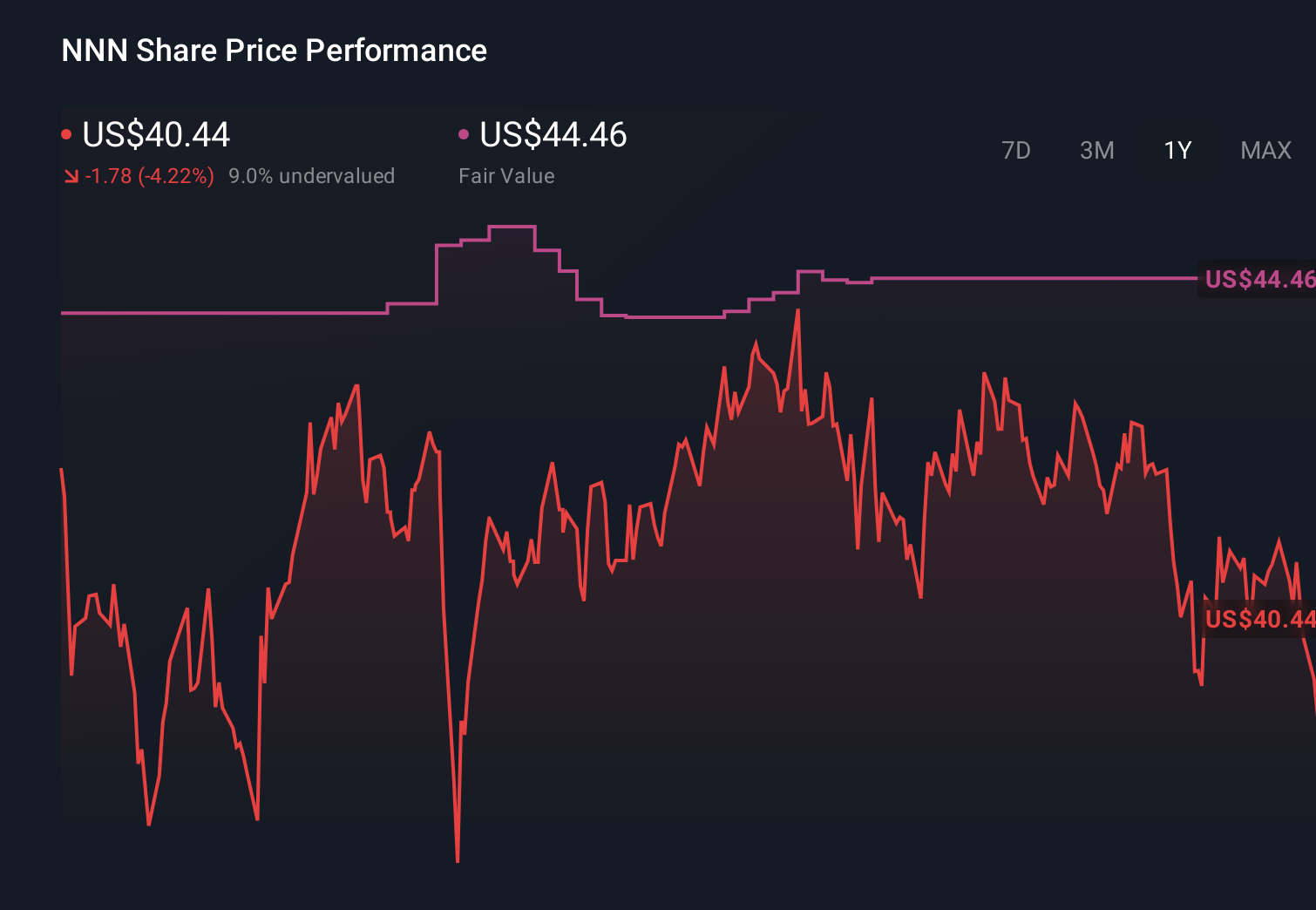

NNN REIT's narrative projects $1.1 billion revenue and $448.9 million earnings by 2029. This requires 4.7% yearly revenue growth and about a $62.4 million earnings increase from $386.5 million today.

Uncover how NNN REIT's forecasts yield a $46.23 fair value, a 3% downside to its current price.

Exploring Other Perspectives

Two Simply Wall St Community fair value estimates span roughly US$46 to US$84 per share, showing how far apart individual views can be. As you weigh those opinions, keep in mind how higher or more persistent interest costs could affect NNN REIT's ability to grow earnings and maintain its balance between income generation and financial flexibility.

Explore 2 other fair value estimates on NNN REIT - why the stock might be worth as much as 77% more than the current price!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your NNN REIT research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free NNN REIT research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate NNN REIT's overall financial health at a glance.

Contemplating Other Strategies?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- Capitalize on the AI infrastructure supercycle with our selection of the 52 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- Uncover the next big thing with 20 elite penny stocks that balance risk and reward.

- The future of work is here. Discover the 29 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com