Alaska Air Group (ALK) recently granted Chief Financial Officer Shane R. Tackett 4,100 restricted stock units, a routine equity award that ties a portion of his compensation directly to the company’s share performance.

See our latest analysis for Alaska Air Group.

Alaska Air Group’s recent equity grant to the CFO comes as the stock trades at $51.09, with a 30-day share price return of 19.68% and a 90-day share price return of 36.86%, while the 1-year total shareholder return is broadly flat at 0.08%. This suggests momentum has picked up recently after a weaker longer term record.

If this kind of renewed momentum has you thinking about where else capital could work harder, it may be worth scanning 20 top founder-led companies

With Alaska Air Group stock trading at $51.09, sitting below an average analyst price target of $59.75 and an intrinsic discount estimate of about 81%, you have to ask whether there is genuine value on offer here or whether the market is already factoring in future growth.

Most Popular Narrative: 11.1% Undervalued

With Alaska Air Group trading at $51.09 against a narrative fair value of $57.50, the current setup leans toward upside in the most widely followed storyline.

The expansion and optimization of the Seattle international gateway, including new long-haul routes and a growing fleet of Boeing 787s, positions Alaska Air Group to benefit from sustained urban growth and increasing travel demand in West Coast cities, which is anticipated to drive higher passenger volumes and top-line revenue growth.

Curious what revenue trajectory, margin rebuild and earnings power need to look like to justify that fair value? The narrative leans on bolder growth and profitability assumptions than the recent past. The valuation math rests on those forward estimates rather than today’s earnings picture.

Result: Fair Value of $57.50 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, Alaska Air Group still faces some clear swing factors, including higher unit costs from labor and fleet spending, as well as execution risk around the Hawaiian Airlines integration.

Find out about the key risks to this Alaska Air Group narrative.

Another View on Alaska Air Group’s Valuation

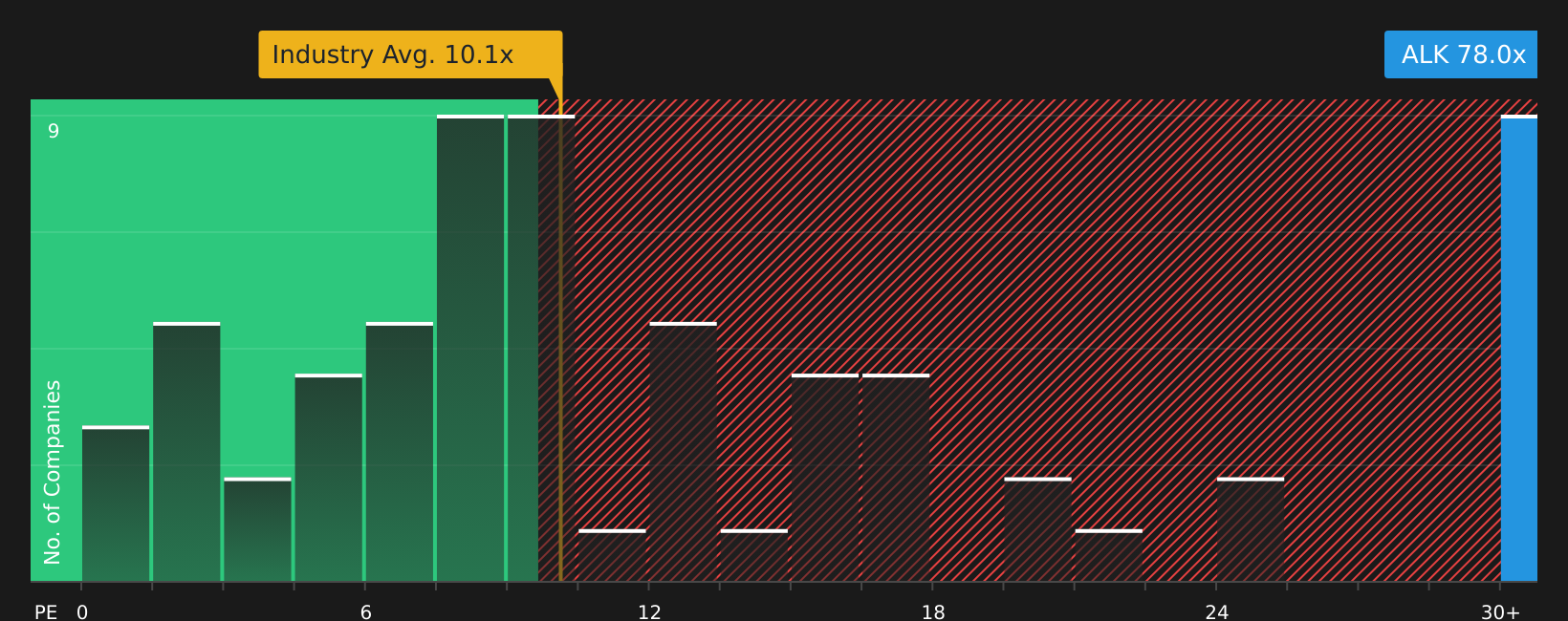

While the narrative fair value of $57.50 suggests Alaska Air Group is undervalued, the current P/E of 78x tells a very different story when set against peer averages of 21x and a fair ratio of 108.8x. Is this a mispriced opportunity, or simply higher valuation risk in plain sight?

See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

With mixed signals around Alaska Air Group’s valuation and outlook, it makes sense to check the underlying data yourself and decide where you stand. To see how the current upside case compares with the key concerns and potential positives, take a closer look at the 2 key rewards and 3 important warning signs.

Looking for more investment ideas beyond Alaska Air Group?

If the Alaska Air Group story has sharpened your focus, do not stop here. Broaden your watchlist with fresh opportunities that match your investing style.

- Target income potential by scanning 7 dividend fortresses that may appeal if you want yields backed by solid fundamentals.

- Hunt for mispriced quality by reviewing 44 high quality undervalued stocks that could offer better entry points than headline stocks.

- Prioritize resilience by checking 74 resilient stocks with low risk scores so you are not the one regretting missed opportunities when volatility picks up.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com